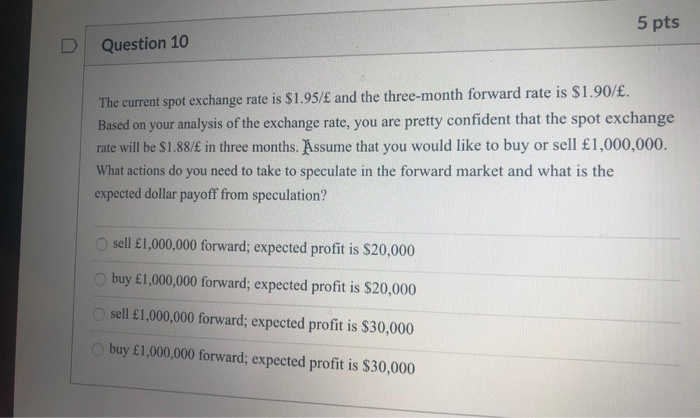

Question: 5 pts D Question 10 The current spot exchange rate is $1.9S/E and the three-month forward rate is $1.90/. Based on your analysis of the

5 pts D Question 10 The current spot exchange rate is $1.9S/E and the three-month forward rate is $1.90/. Based on your analysis of the exchange rate, you are pretty confident that the spot exchange rate will be $1.88/f in three months. Assume that you would like to buy or sell 1,000,000. What actions do you need to take to speculate in the forward market and what is the expected dollar payoff from speculation? sell 1,000,000 forward; expected profit is $20,000 buy 1,000,000 forward; expected profit is $20,000 sell 1,000,000 forward; expected profit is $30,000 buy 1,000,000 forward; expected profit is $30,000

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock