Question: * 5:4 split after closing on 12/31/05 **6:1 split after close on 12/31/05 Q1 calculate the percentage return in a value weighted series for the

* 5:4 split after closing on 12/31/05

**6:1 split after close on 12/31/05

Q1 calculate the percentage return in a value weighted series for the december 31, 2005 to december 31, 2016

a. -0.1159

b. -0.1555

c. 0.1302

d. 0.1487

e. none of the above

Q2 find the percentage change in the value of the index from 1/4 to 1/5. round intermidiate step and your final answer to four decimal. (answer in decimal format)

Q3 a prive weighted index currently consist of stocks A,B, and C suppose that stock C is replaced with a higher priced stock (stock D for example) what will be the intermidiate effect of the change on the index's value?

a. value will increase

b. value will decrease

c. value will remain the same

d. cannot be determined

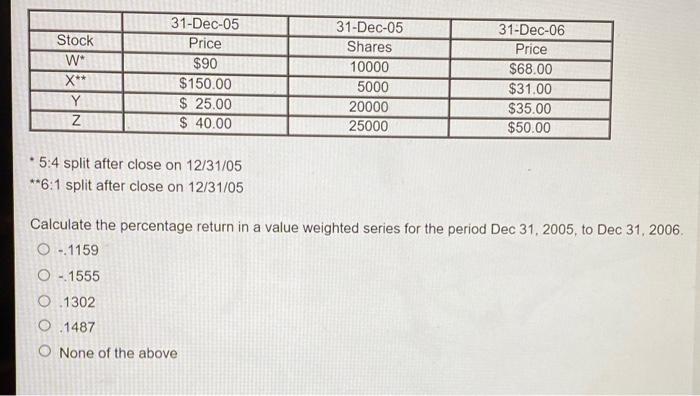

Stock W* X** Y z 31-Dec-05 Price $90 $150.00 $ 25.00 $ 40.00 31-Dec-05 Shares 10000 5000 20000 25000 31-Dec-06 Price $68.00 $31.00 $35.00 $50.00 5:4 split after close on 12/31/05 **6:1 split after close on 12/31/05 Calculate the percentage return in a value weighted series for the period Dec 31, 2005, to Dec 31, 2006. 0 - 1159 O - 1555 O 1302 O.1487 None of the above

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock