Question: 6 1.1 points 03:49:51 eBook References Problem 5-55 Activity-Based Costing (LO 5-1, 5-2, 5-4, 5-5) Manchester Technology, Inc., manufactures several different types of printed

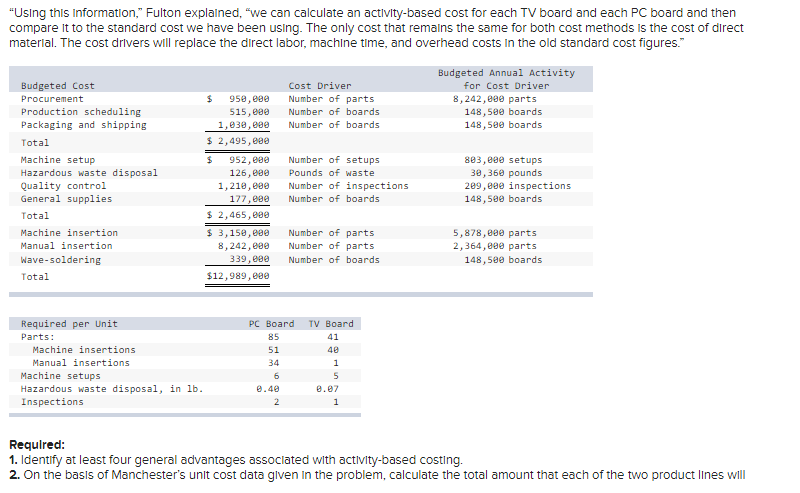

6 1.1 points 03:49:51 eBook References Problem 5-55 Activity-Based Costing (LO 5-1, 5-2, 5-4, 5-5) Manchester Technology, Inc., manufactures several different types of printed circuit boards; however, two of the boards account for the majority of the company's sales. The first of these boards, a television circuit board, has been a standard in the Industry for several years. The market for this type of board is competitive and price-sensitive. Manchester plans to sell 80,000 of the TV boards in 20x1 at a price of $460 per unit. The second high-volume product, a personal computer circuit board, is a recent addition to Manchester's product line. Because the PC board Incorporates the latest technology, It can be sold at a premium price. The 20x1 plans include the sale of 55,000 PC boards at $775 per unit. Manchester's management group is meeting to discuss how to spend the sales and promotion dollars for 20x1. The sales manager believes that the market share for the TV board could be expanded by concentrating Manchester's promotional efforts in this area. In response to this suggestion, the production manager said, "Why don't you go after a bigger market for the PC board? The cost sheets that I get show that the contribution from a PC board is significantly larger than the contribution from a TV board. I know we get a premium price for the PC board. Selling it should help overall profitability." The cost-accounting system shows that the following costs apply to the PC and TV boards. Direct material Direct labor Machine time PC Board $244 3.0 hr. 1.0 hr. TV Board $154 2.0 hr. 0.5 hr. Variable manufacturing overhead is applied on the basis of direct-labor hours. For 20x1, variable overhead is budgeted at $2,465,000, and direct-labor hours are estimated at 357,500. The hourly rates for machine time and direct labor are $28 and $36, respectively. The company applies a material-handling charge at 10 percent of material cost. This material-handling charge is not included in variable manufacturing overhead. Total 20x1 expenditures for direct material are budgeted at $25,740,000. Andrew Fulton, Manchester's controller, believes that before the management group proceeds with the discussion about allocating sales and promotional dollars to Individual products, it might be worthwhile to look at these products on the basis of the activities Involved in their production. Fulton has prepared the following schedule to help the management group understand this concept.

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts