Question: 6. (8 pts) Write a formula for the covariance between asset i and asset j in a single-factor risk model where the single factor is

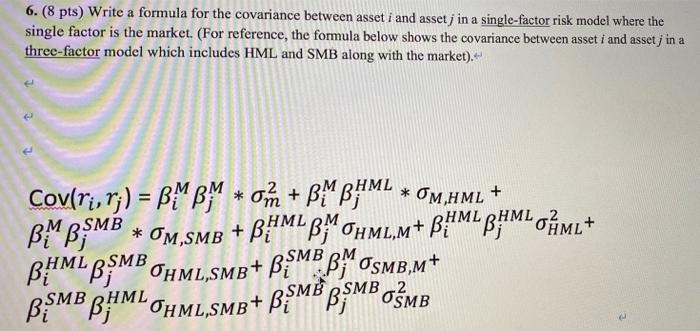

6. (8 pts) Write a formula for the covariance between asset i and asset j in a single-factor risk model where the single factor is the market. (For reference, the formula below shows the covariance between asset i and asset in a three-factor model which includes HML and SMB along with the market). * Cov(ri, r;) = BM BM * 0m+ BM BHML * OMHML + BMB.MB * OM,SMB + BML BM OH ML,m+ BML BML O ML+ BHMLB.MB OHML,SMB+BSMBBM OSMB,m+ BMBBHMLOHML,SMB+ BSMBBMBOMB RSMB

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock