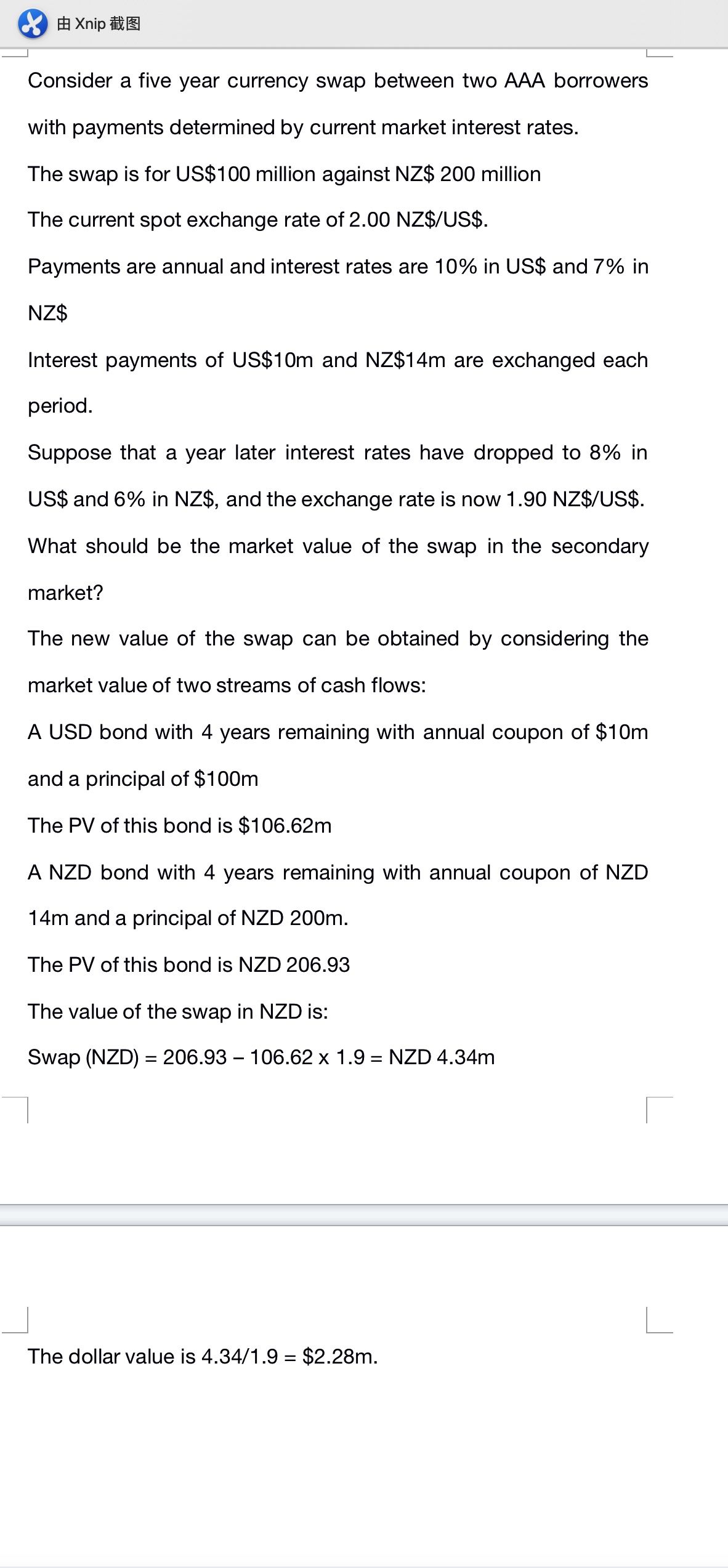

Question: 6 EH Xnip E. _l Consider a five year currency swap between two AAA borrowers l_ with payments determined by current market interest rates. The

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock