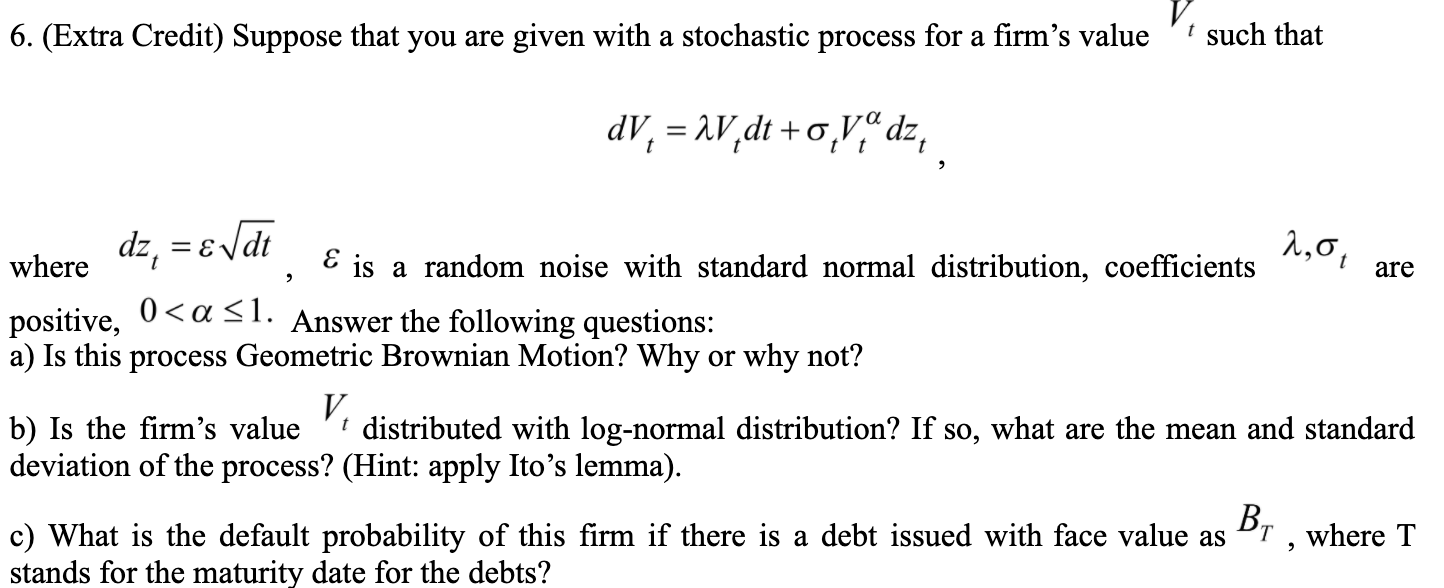

Question: 6. (Extra Credit) Suppose that you are given with a stochastic process for a firm's value t such that dV, = 2V dt+o, Vadz dz,

6. (Extra Credit) Suppose that you are given with a stochastic process for a firm's value t such that dV, = 2V dt+o, Vadz dz, = &vdt are 2,0, where E is a random noise with standard normal distribution, coefficients positive, 0 6. (Extra Credit) Suppose that you are given with a stochastic process for a firm's value t such that dV, = 2V dt+o, Vadz dz, = &vdt are 2,0, where E is a random noise with standard normal distribution, coefficients positive, 0

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock