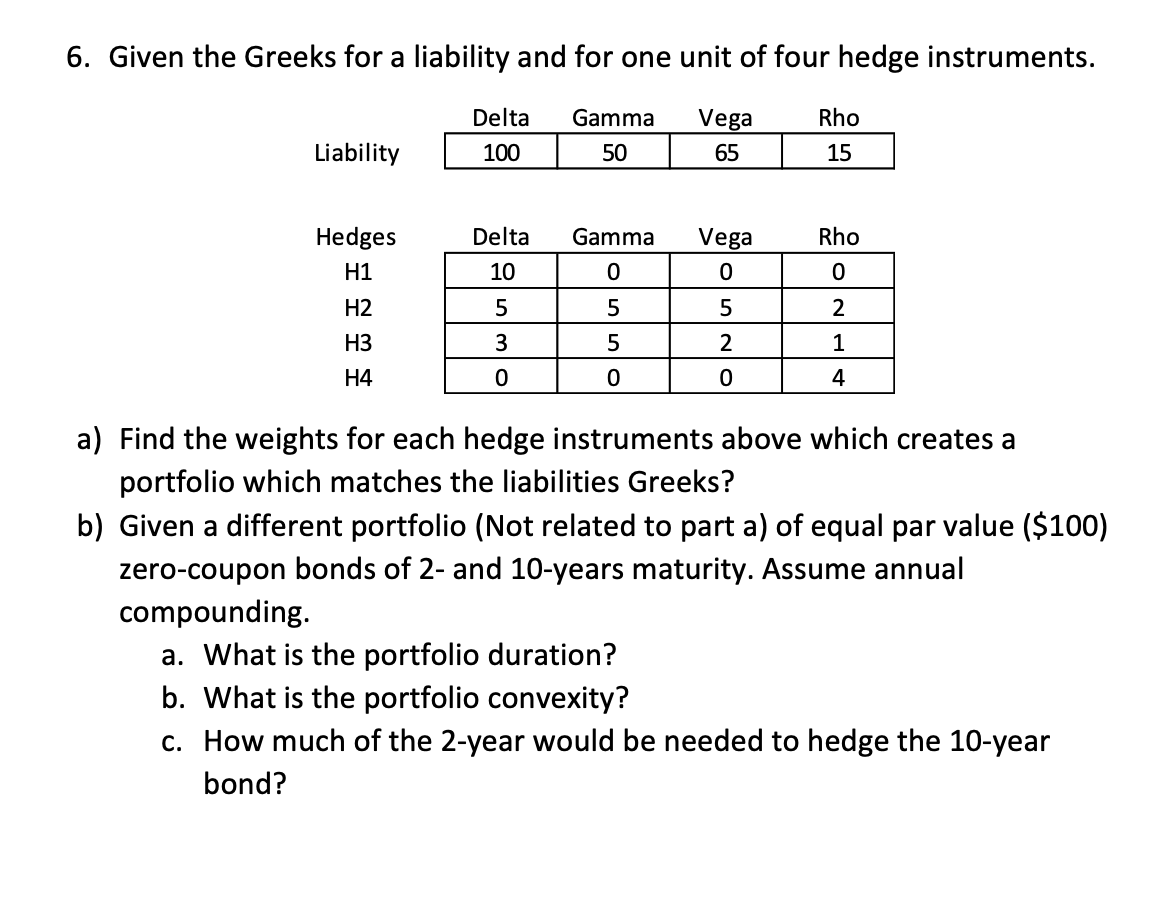

Question: 6. Given the Greeks for a liability and for one unit of four hedge instruments. Liability a) Find the weights for each hedge instruments above

6. Given the Greeks for a liability and for one unit of four hedge instruments. Liability a) Find the weights for each hedge instruments above which creates a portfolio which matches the liabilities Greeks? b) Given a different portfolio (Not related to part a) of equal par value (\$100) zero-coupon bonds of 2- and 10-years maturity. Assume annual compounding. a. What is the portfolio duration? b. What is the portfolio convexity? c. How much of the 2-year would be needed to hedge the 10-year bond

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock