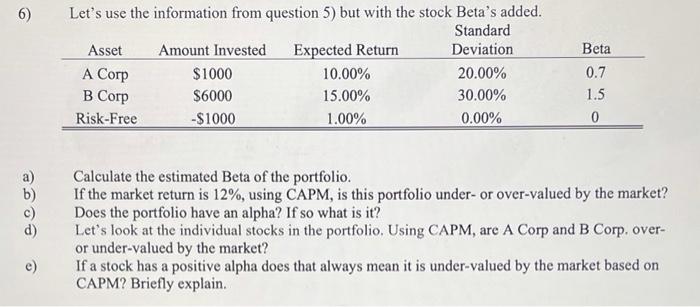

Question: 6) Let's use the information from question 5) but with the stock Beta's added. Standard Asset Amount Invested Expected Return Deviation A Corp $1000 10.00%

6) Let's use the information from question 5) but with the stock Beta's added. Standard Asset Amount Invested Expected Return Deviation A Corp $1000 10.00% 20.00% B Corp $6000 15.00% 30.00% Risk-Free -$1000 1.00% 0.00% Beta 0.7 1.5 0 a) b) c) d) Calculate the estimated Beta of the portfolio. If the market return is 12%, using CAPM, is this portfolio under-or over-valued by the market? Does the portfolio have an alpha? If so what is it? Let's look at the individual stocks in the portfolio. Using CAPM, are A Corp and B Corp. over- or under-valued by the market? If a stock has a positive alpha does that always mean it is under-valued by the market based on CAPM? Briefly explain. e) 6) Let's use the information from question 5) but with the stock Beta's added. Standard Asset Amount Invested Expected Return Deviation A Corp $1000 10.00% 20.00% B Corp $6000 15.00% 30.00% Risk-Free -$1000 1.00% 0.00% Beta 0.7 1.5 0 a) b) c) d) Calculate the estimated Beta of the portfolio. If the market return is 12%, using CAPM, is this portfolio under-or over-valued by the market? Does the portfolio have an alpha? If so what is it? Let's look at the individual stocks in the portfolio. Using CAPM, are A Corp and B Corp. over- or under-valued by the market? If a stock has a positive alpha does that always mean it is under-valued by the market based on CAPM? Briefly explain. e)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts