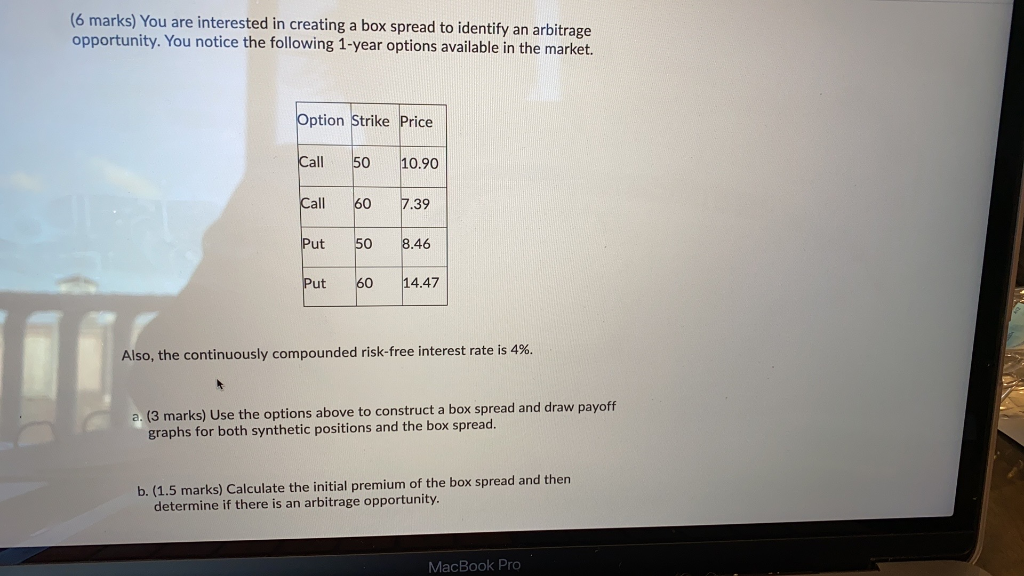

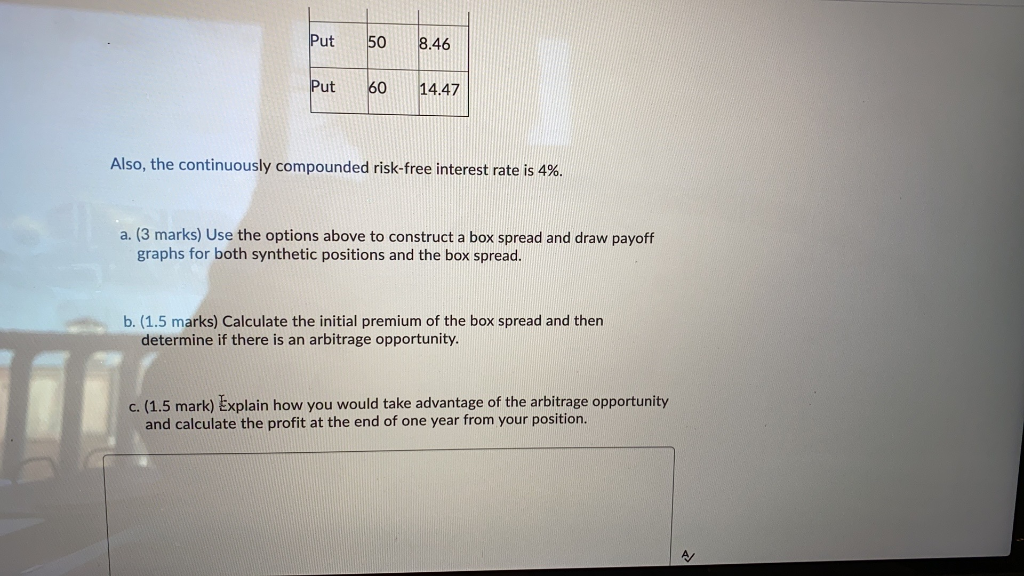

Question: (6 marks) You are interested in creating a box spread to identify an arbitrage opportunity. You notice the following 1-year options available in the market.

(6 marks) You are interested in creating a box spread to identify an arbitrage opportunity. You notice the following 1-year options available in the market. Option Strike Price Call 50 10.90 Call 60 7.39 Put 508.46 Put 60 14.47 Also, the continuously compounded risk-free interest rate is 4%. a. (3 marks) Use the options above to construct a box spread and draw payoff graphs for both synthetic positions and the box spread. b. (1.5 marks) Calculate the initial premium of the box spread and then determine if there is an arbitrage opportunity. MacBook Pro Put 50 8.46 Put 60 14.47 Also, the continuously compounded risk-free interest rate is 4%. a. (3 marks) Use the options above to construct a box spread and draw payoff graphs for both synthetic positions and the box spread. b. (1.5 marks) Calculate the initial premium of the box spread and then determine if there is an arbitrage opportunity. c. (1.5 mark) Explain how you would take advantage of the arbitrage opportunity and calculate the profit at the end of one year from your position

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts