Question: 6. Suppose that your first assignment as a financial analyst in the Giant Investment Company is to evaluate the performance of the Mini Fund

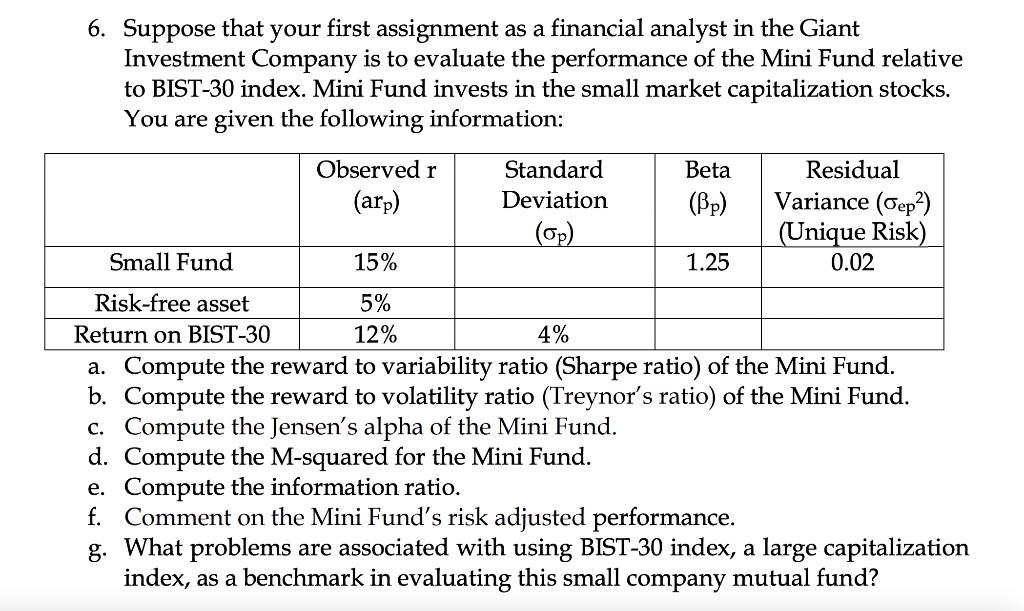

6. Suppose that your first assignment as a financial analyst in the Giant Investment Company is to evaluate the performance of the Mini Fund relative to BIST-30 index. Mini Fund invests in the small market capitalization stocks. You are given the following information: Observed r (arp) Standard Deviation (op) Beta (pp) c. Compute the Jensen's alpha of the Mini Fund. d. Compute the M-squared for the Mini Fund. Small Fund 15% Risk-free asset 5% Return on BIST-30 12% 4% a. Compute the reward to variability ratio (Sharpe ratio) of the Mini Fund. b. Compute the reward to volatility ratio (Treynor's ratio) of the Mini Fund. Residual Variance (Gep) (Unique Risk) 0.02 1.25 e. Compute the information ratio. f. Comment on the Mini Fund's risk adjusted performance. g. What problems are associated with using BIST-30 index, a large capitalization index, as a benchmark in evaluating this small company mutual fund?

Step by Step Solution

3.37 Rating (144 Votes )

There are 3 Steps involved in it

Here are the steps on how to solve this question a Compute the reward to variability ratio Sharpe ratio of the Mini Fund The Sharpe ratio is a measure of the excess return of an investment over the ri... View full answer

Get step-by-step solutions from verified subject matter experts