2. read and analyze the case, Jones Electrical Distribution. 1 How well is fones lectrical Distrikution...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

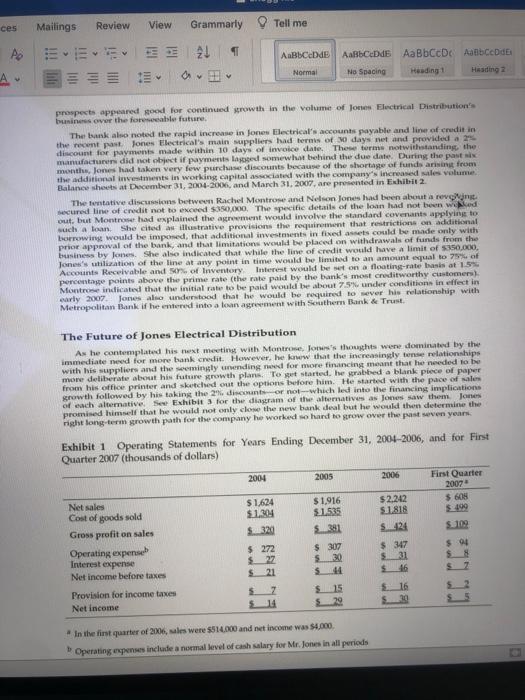

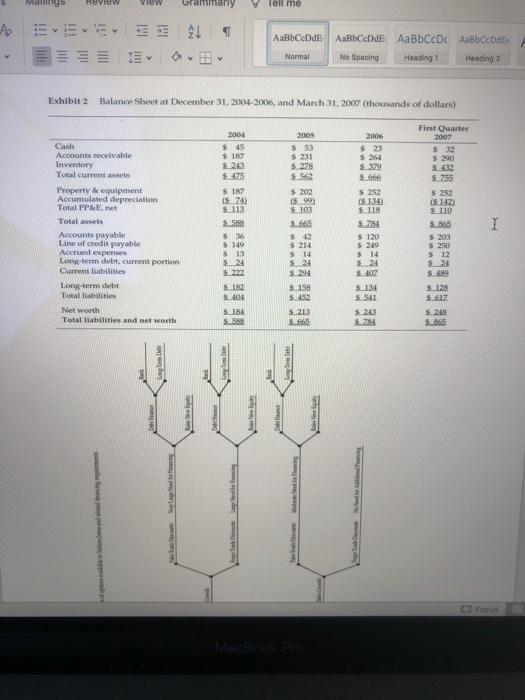

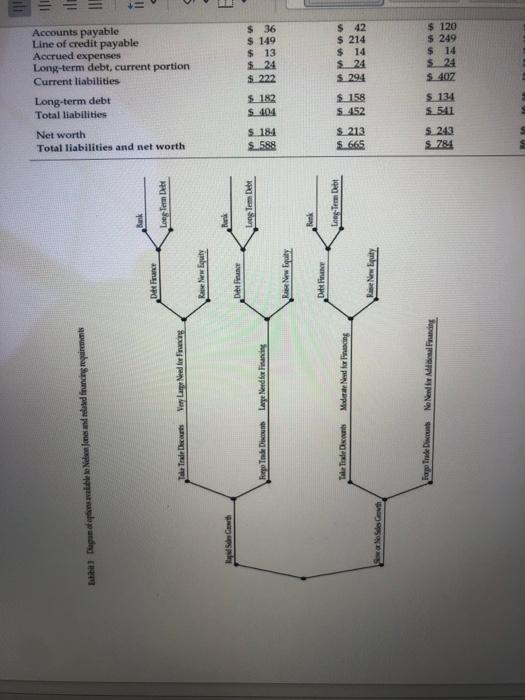

2. read and analyze the case, Jones Electrical Distribution. 1 How well is "fones lectrical Distrikution" perturtning? What mast Jones do well to muccend 2 Why does a business that has profit of 5000 per year need a bank loan! 1 What drove the increse in lones'A accounts rvoeivable and inventory balances in 2005 ad 20067 4 Nelon lones's esitimalestat a SO0 line of credit is sufficient for 2007 accurate? 3. When will Jons be able to repay the line of credis? 6 What could Jones do u teduce the stze of the line of credit he needa 7. What are the implicanu or Jones's litestyle of accepting the new, larger line of credit? In order to answer these questions, you should be utilizing some or all of the following tools: analyze income statements & cash flow, utilize financial ratios to understand the business situation, understand the relationship between sustainable growth rate & profitability, address the desire to expand with capital requirements & profitability. Jones Electrical Distribution After several years of rapid growth, in the spring of 2007 Jones Electrical Distribution anticipated a further substantial increase in nales. Despite good profits, the company had experienced a shortage of cash and had found it necessary to increase its borrowing fron Metropolitan Bank-a local on branch bank-to S250,000 in 2006, The maximum loan that Metropolitan would make to any one borrower was $250.000, and Jones had been able to stay within the limit only by relving very heavily on trade credit from the manufacturers from whom Jones purchaed the electrical products it sold to its customens. Nelson Jones, sole owner and president of the company, was therefore looking elsewhere for a new banking relationship that would allow him to negotiate a larger loan. Jim Lyons, a homebuilder who was a friend of Jones, introduced Jones to Rachel Montrone, Lyons's relationship officer at the local branch of Southern Bank & Trust-a large, regional bank Southem had a 7-year relationship with Lyos, including a current loan balance of over S3 milion Jones and Montrose tentatively dincussed the possibility that Southem might extend a line of credit to Jans up to a maximum amount of $350,000. Jones thought that a loan of thin size would more than meet his needs for at least the next year, and he was eager for the flexibility that a line of credit of this size would provide. Alter discunsion, Montrose had arranged for the eredit department of Southern Bank & Trust to investigate Nelson Jones and his company Backgre and of Jones Electrical Distribution Jones Electrical Distribution was founded in 1990 as a partnership between Nebson Jonos and his college roominate, Dave Verden. In 2003, Jones arnd Verden had a disagreement on how aggressivety they should grow the business, and Jones ultimately bought Verden out for $250,000 They agrend that Jones would pay Verden the $250,000 in installments of S2.000 per month plus interest of per year chegg file eferences Mailings Review View Grammarly Tell me Ka v 。而。前。 正 AaBbCeDdE AaBbCeDdE AaBbCcD AaBbCcDdE Normal No Spacing Heading 1 Heading 3 The business sold electrical components and tools to general contractors and electricians. The products, which included items such as controllers, breakers, signal devices and fuses, were purchased from nearly 100 different suppliers. Jones's customers used the products in the construction and repair of commercial and residential buildings, To a degree, Jones's sales followed the seasonality of its customens' businesses which had their highest activity during the spring and summer when weather was most conducive for construction work. The market in which Jones competed was large, fragmented, and highly competitive. Jones faced significant competition from national distributors, home centers, and other small supply houses. In spite of the competition, Jones had built up sales volume by successfully competing on price and employing an aggressive direct sales force who often visited customers at their job sites. In order to compete on price, Jones maintained tight control over operating expenses, including paying his salesforce primarily on commission and keeping overhead to a minimum. In addition, as part of his expense management effort, Jones had historically paid his suppliers within 10 days of the invoice date in order to take full advantage of the 2% discounts they offered for quick payments. Jones had also proved adept at demand forecasting and inventory management, allowing him to satisfy his customers' demand with a modest amount of inventory relative to his larger competitors. Jones's focus and dedication to his business allowed him to build it into a profitable operation. Jones Electrical Distribution had grown to $2.24 million in sales and $30,000 of net income in 2006. Operating statements for years 2004-2006 and for the three months ending March 31, 2007, are given in Exhibit 1. Financing the Business Through Southern Bank & Trust To solve his financing need, Jones wanted to develop a relationship with a larger bank that would not run into issues with maximum loans to a single borrower as he had experienced with Metropolitan Bank. He wanted to build a relationship with a bank that could grow with him including to more locations if he decided to add additional sites in the future. As part of its customary due diligence of Jones Electrical Distribution, the Southem Bank & Trust's credit department asked Jones's friend Jim Lyons for a reference on Jones. Lyons's reference included the followine.commente "Nalson isahusinessman of the hiohost.intaaritand sharn Mailings Review View Grammarly Tell me AaBbCeDdE AaBbCeDdE AaBbCcD AasbccodE = 。|のv田▼ Normal No Spacing Heading 1 Heading 2 Financing the Business Through Southern Bank & Trust To solve his financing need, Jones wanted to develop a relationship with a larger bank that would not run into issues with maximum loans to a single borrower as he had experienced with Metropolitan Bank He wanted to build a relationship with a bank that could grow with him, including to more locations if he decided to add additional sites in the future. As part of its customary due diligence of Jones Electrical Distribution, the Southem Bank & Trust's credit department asked Jones's friend Jim Lyons for a reference on Jones. Lyons's reference included the following comments: "Nelson is a businessman of the highest integrity ansharp acumen who is a very hands-on manager of his operation. He has excellent knowledgeruf the products he sells and provides customers with excellent service. He also lives a modest lifestyle." The bank also toured Jones Electrical Distribution's warehouse and office and interviewed the area sales managers for three of the manufacturers from whom Jones bought the products he sold. The managers were unanimous in their favorable opinion of Jones. One of them said: "Nelson has been one of our best performing wholesalers. He really knows how to build relationships and close a sale. He has also been great with his expense management. The guy does not spend a dime unless he absolutely has to. We look forward to building a bigger relationship with him in the future." In addition to the electrical distribution business, which was Jones's only source of income, Jones held jointly with his wife an equity in their home. The house had cost $199,000 to build in 1999 and was mortgaged for $117,000. He also held a $250,000 life insurance policy, payable to his wife. Otherwise, they had no sizeable personal investments. Southern Bank & Trust gave particular attention to the debt position and current ratio of the business. It noted the ready market for the company's products at all times and the fact that sales prospects were favorable. The bank's investigator reported: "Sales are expected to reach $2.7 million by the end of 2007." On the other hand, it was recognized that a general economic downtum might slow down the rate of increase in sales. Projections beyond 2007 were difficult to make, but the pronpects appeared good for continued growih in the volume of Jores Electrical Distribution's business over the foreseeable future The bank alno noted the rapid increase in Jones Electrical's accounts payable and line of credit in Lihe necnt past Jone Electrical'a.main.suoliers had termms of 30 davs net and.ovided .2% OFocu Mailings Review View Grammarly Tell me ces 讯、而、。 AaBbCeDdE AalbCeDdE AaBbCcD AalbCcDdE A Normal No Spacing Heading 1 Haading 2 prospects appeared good for continued growth in the volume of Jones Electrical Distribution's buniness over the foreseeable future. The bank also noted the rapid increase in Jones Electrical's accounts payable and line of credit in the recent past Jones Electrical's main suppliers had terms of 30 days net and provided a 2% discount for payments made within 10 day of invoice date. These terms notwithstanding, the manufacturen did not object if payments laged somewhat behind thr due date. During the past six months, Jones had taken very few purchase discounts because of the shortage of funds arising from the additional investments in working capital associated with the company's increased sales volume. Balance sheets at December 31, 2004-2006, and March 31, 2007, are presented in Exhibit 2. The tentative discussions between Rachel Montrose and Nelson Jones had been about a revevjng. ecured line of credit not to exceed $350,000. The specific details of the loan had not been wked out. but Montrose had explained the agreement would involve the standard covenants applying to such a loan. She cited as illustrative provisions the requirement that restrictions on additional borrowing would be imposed, that additional investments in fixed assets could be made only with prior approval of the bank, and that limitations would be placed on withdrawals of funds from the business by Jones. She also indicated that while the line of credit would have a limit of 5350,000, Jones's utilization of the line at any point in time would be limited to an amount equal to 75% of Accounts Receivable and S of Inventory percentage points above the prime rate (the rate paid by the bank's most creditvworthy customers). Montrose indicated that the initial rate to be paid would be about 7.5% under conditions in effect in early 2007. Jones also understood that he would be required to sever his relationship with Metropolitan Bank if he entered into a loan agreement with Southern Bank & Trust. Interest would be set on a floating-rate basis at 15% The Future of Jones Electrical Distribution As he contemplated his next meeting with Montrose, Jos's thoughts were dominated by the immediate need for more bank credit. However, he knww that the increasingly tense relationships with his suppliers and the seemingty unending need for more financing meant that he needed to be more deliberate about his future growth plans. To get started. he grabbed a blank piece of paper from his oftice printer and sketched out the options before him. He started with the pace of sales growth followed by his taking the 2% discoantsor not-which led into the financing implications of each altermative. See Exhibit 3 for the diagram of thhe altermatives as Jones saw them Jones promised himself that he would not only close the new bank deal but he would then determine the right long-term growth path for the company he worked so hard to grow over the past seven years Exhibit 1 Operating Statements for Years Ending December 31, 2004-2006, and for First Quarter 2007 (thousands of dollars) 2004 2005 2006 First Quarter 2007 $ 608 £499 Net sales Cost of goods sold $1,624 $1.304 $1,916 $1.535 $2.242 S1818 Gross profit on sales 320 381 S424 S.109 Operating expense Interest expense Net income before taxes $ 347 S31 $94 $ 272 $ 27 S21 $ 307 $30 S44 Provision for income taxes Net income S14 *In the first quarter of 2006, sales were $514.000 and net income was $4,000. Operating expenses include a nomal level of cash salary for Mr. Jones in I periods Mallings Review Tell me 24 T AaBbCeDdE AaBbCeDdE AaBbCcDr AabbCcDdE v田。 Normal No Spacing Heading 1 Heading 2 Exhibit 2 Balance Sheet at December 31, 2004-2006, and March 31, 2007 (thousands of dollars) First Quarter 2007 2004 2005 2006 Cash Accounts receivable Inventory Total current assets $45 $ 187 5.243 $.475 S 53 $231 $.228 5.562 $23 S 264 S.329 5.666 S 32 S 290 S432 5.755 Property & equlpment S 187 係74) S.113 S 252 (S 134) $ 118 $ 202 Accumulated depreciation Total PP&E. net $252 G.142) $110 $103 Total assets 5.588 S.784 S865 Accounts payable Line of credik payable Accrued expenses Long-term debt, current portion Current liabilities $36 $149 $13 5 42 $ 214 $ 14 S24 5.294 $ 120 $249 $ 14 524 $203 5250 S 12 524 5.222 Long-term debt Total liabilities S.182 S 125 5.134 S.541 S.452 5.612 Net worth .213 5.243 5.245 Total liabilities and net worth 5.588 S865 介介 Focus MocBook Pio wwbu Accounts payable Line of credit payable Accrued expenses Long-term debt, current portion S 294 Current liabilities Long-term debt Total liabilities $ 158 S.452 Net worth Total liabilities and net worth $ 213 S 665 Eahbit Dagunof epns avalble te Neln Jomes and nelated financing equiremmts Diee Firunce Long Tem Deb Teke Trade Decourts Very Lane Need fer Firncing Rase New Eiquity Bank Det Finance Long Tem Debt Forgo Tade Discount Lage Need er Financing Raise New Equity Diet Finance Moderae Ned kar Finaing Rase New Equty Fago Trade Dicounb Ne Nenl for Addioal Financing SSS. 2. read and analyze the case, Jones Electrical Distribution. 1 How well is "fones lectrical Distrikution" perturtning? What mast Jones do well to muccend 2 Why does a business that has profit of 5000 per year need a bank loan! 1 What drove the increse in lones'A accounts rvoeivable and inventory balances in 2005 ad 20067 4 Nelon lones's esitimalestat a SO0 line of credit is sufficient for 2007 accurate? 3. When will Jons be able to repay the line of credis? 6 What could Jones do u teduce the stze of the line of credit he needa 7. What are the implicanu or Jones's litestyle of accepting the new, larger line of credit? In order to answer these questions, you should be utilizing some or all of the following tools: analyze income statements & cash flow, utilize financial ratios to understand the business situation, understand the relationship between sustainable growth rate & profitability, address the desire to expand with capital requirements & profitability. Jones Electrical Distribution After several years of rapid growth, in the spring of 2007 Jones Electrical Distribution anticipated a further substantial increase in nales. Despite good profits, the company had experienced a shortage of cash and had found it necessary to increase its borrowing fron Metropolitan Bank-a local on branch bank-to S250,000 in 2006, The maximum loan that Metropolitan would make to any one borrower was $250.000, and Jones had been able to stay within the limit only by relving very heavily on trade credit from the manufacturers from whom Jones purchaed the electrical products it sold to its customens. Nelson Jones, sole owner and president of the company, was therefore looking elsewhere for a new banking relationship that would allow him to negotiate a larger loan. Jim Lyons, a homebuilder who was a friend of Jones, introduced Jones to Rachel Montrone, Lyons's relationship officer at the local branch of Southern Bank & Trust-a large, regional bank Southem had a 7-year relationship with Lyos, including a current loan balance of over S3 milion Jones and Montrose tentatively dincussed the possibility that Southem might extend a line of credit to Jans up to a maximum amount of $350,000. Jones thought that a loan of thin size would more than meet his needs for at least the next year, and he was eager for the flexibility that a line of credit of this size would provide. Alter discunsion, Montrose had arranged for the eredit department of Southern Bank & Trust to investigate Nelson Jones and his company Backgre and of Jones Electrical Distribution Jones Electrical Distribution was founded in 1990 as a partnership between Nebson Jonos and his college roominate, Dave Verden. In 2003, Jones arnd Verden had a disagreement on how aggressivety they should grow the business, and Jones ultimately bought Verden out for $250,000 They agrend that Jones would pay Verden the $250,000 in installments of S2.000 per month plus interest of per year chegg file eferences Mailings Review View Grammarly Tell me Ka v 。而。前。 正 AaBbCeDdE AaBbCeDdE AaBbCcD AaBbCcDdE Normal No Spacing Heading 1 Heading 3 The business sold electrical components and tools to general contractors and electricians. The products, which included items such as controllers, breakers, signal devices and fuses, were purchased from nearly 100 different suppliers. Jones's customers used the products in the construction and repair of commercial and residential buildings, To a degree, Jones's sales followed the seasonality of its customens' businesses which had their highest activity during the spring and summer when weather was most conducive for construction work. The market in which Jones competed was large, fragmented, and highly competitive. Jones faced significant competition from national distributors, home centers, and other small supply houses. In spite of the competition, Jones had built up sales volume by successfully competing on price and employing an aggressive direct sales force who often visited customers at their job sites. In order to compete on price, Jones maintained tight control over operating expenses, including paying his salesforce primarily on commission and keeping overhead to a minimum. In addition, as part of his expense management effort, Jones had historically paid his suppliers within 10 days of the invoice date in order to take full advantage of the 2% discounts they offered for quick payments. Jones had also proved adept at demand forecasting and inventory management, allowing him to satisfy his customers' demand with a modest amount of inventory relative to his larger competitors. Jones's focus and dedication to his business allowed him to build it into a profitable operation. Jones Electrical Distribution had grown to $2.24 million in sales and $30,000 of net income in 2006. Operating statements for years 2004-2006 and for the three months ending March 31, 2007, are given in Exhibit 1. Financing the Business Through Southern Bank & Trust To solve his financing need, Jones wanted to develop a relationship with a larger bank that would not run into issues with maximum loans to a single borrower as he had experienced with Metropolitan Bank. He wanted to build a relationship with a bank that could grow with him including to more locations if he decided to add additional sites in the future. As part of its customary due diligence of Jones Electrical Distribution, the Southem Bank & Trust's credit department asked Jones's friend Jim Lyons for a reference on Jones. Lyons's reference included the followine.commente "Nalson isahusinessman of the hiohost.intaaritand sharn Mailings Review View Grammarly Tell me AaBbCeDdE AaBbCeDdE AaBbCcD AasbccodE = 。|のv田▼ Normal No Spacing Heading 1 Heading 2 Financing the Business Through Southern Bank & Trust To solve his financing need, Jones wanted to develop a relationship with a larger bank that would not run into issues with maximum loans to a single borrower as he had experienced with Metropolitan Bank He wanted to build a relationship with a bank that could grow with him, including to more locations if he decided to add additional sites in the future. As part of its customary due diligence of Jones Electrical Distribution, the Southem Bank & Trust's credit department asked Jones's friend Jim Lyons for a reference on Jones. Lyons's reference included the following comments: "Nelson is a businessman of the highest integrity ansharp acumen who is a very hands-on manager of his operation. He has excellent knowledgeruf the products he sells and provides customers with excellent service. He also lives a modest lifestyle." The bank also toured Jones Electrical Distribution's warehouse and office and interviewed the area sales managers for three of the manufacturers from whom Jones bought the products he sold. The managers were unanimous in their favorable opinion of Jones. One of them said: "Nelson has been one of our best performing wholesalers. He really knows how to build relationships and close a sale. He has also been great with his expense management. The guy does not spend a dime unless he absolutely has to. We look forward to building a bigger relationship with him in the future." In addition to the electrical distribution business, which was Jones's only source of income, Jones held jointly with his wife an equity in their home. The house had cost $199,000 to build in 1999 and was mortgaged for $117,000. He also held a $250,000 life insurance policy, payable to his wife. Otherwise, they had no sizeable personal investments. Southern Bank & Trust gave particular attention to the debt position and current ratio of the business. It noted the ready market for the company's products at all times and the fact that sales prospects were favorable. The bank's investigator reported: "Sales are expected to reach $2.7 million by the end of 2007." On the other hand, it was recognized that a general economic downtum might slow down the rate of increase in sales. Projections beyond 2007 were difficult to make, but the pronpects appeared good for continued growih in the volume of Jores Electrical Distribution's business over the foreseeable future The bank alno noted the rapid increase in Jones Electrical's accounts payable and line of credit in Lihe necnt past Jone Electrical'a.main.suoliers had termms of 30 davs net and.ovided .2% OFocu Mailings Review View Grammarly Tell me ces 讯、而、。 AaBbCeDdE AalbCeDdE AaBbCcD AalbCcDdE A Normal No Spacing Heading 1 Haading 2 prospects appeared good for continued growth in the volume of Jones Electrical Distribution's buniness over the foreseeable future. The bank also noted the rapid increase in Jones Electrical's accounts payable and line of credit in the recent past Jones Electrical's main suppliers had terms of 30 days net and provided a 2% discount for payments made within 10 day of invoice date. These terms notwithstanding, the manufacturen did not object if payments laged somewhat behind thr due date. During the past six months, Jones had taken very few purchase discounts because of the shortage of funds arising from the additional investments in working capital associated with the company's increased sales volume. Balance sheets at December 31, 2004-2006, and March 31, 2007, are presented in Exhibit 2. The tentative discussions between Rachel Montrose and Nelson Jones had been about a revevjng. ecured line of credit not to exceed $350,000. The specific details of the loan had not been wked out. but Montrose had explained the agreement would involve the standard covenants applying to such a loan. She cited as illustrative provisions the requirement that restrictions on additional borrowing would be imposed, that additional investments in fixed assets could be made only with prior approval of the bank, and that limitations would be placed on withdrawals of funds from the business by Jones. She also indicated that while the line of credit would have a limit of 5350,000, Jones's utilization of the line at any point in time would be limited to an amount equal to 75% of Accounts Receivable and S of Inventory percentage points above the prime rate (the rate paid by the bank's most creditvworthy customers). Montrose indicated that the initial rate to be paid would be about 7.5% under conditions in effect in early 2007. Jones also understood that he would be required to sever his relationship with Metropolitan Bank if he entered into a loan agreement with Southern Bank & Trust. Interest would be set on a floating-rate basis at 15% The Future of Jones Electrical Distribution As he contemplated his next meeting with Montrose, Jos's thoughts were dominated by the immediate need for more bank credit. However, he knww that the increasingly tense relationships with his suppliers and the seemingty unending need for more financing meant that he needed to be more deliberate about his future growth plans. To get started. he grabbed a blank piece of paper from his oftice printer and sketched out the options before him. He started with the pace of sales growth followed by his taking the 2% discoantsor not-which led into the financing implications of each altermative. See Exhibit 3 for the diagram of thhe altermatives as Jones saw them Jones promised himself that he would not only close the new bank deal but he would then determine the right long-term growth path for the company he worked so hard to grow over the past seven years Exhibit 1 Operating Statements for Years Ending December 31, 2004-2006, and for First Quarter 2007 (thousands of dollars) 2004 2005 2006 First Quarter 2007 $ 608 £499 Net sales Cost of goods sold $1,624 $1.304 $1,916 $1.535 $2.242 S1818 Gross profit on sales 320 381 S424 S.109 Operating expense Interest expense Net income before taxes $ 347 S31 $94 $ 272 $ 27 S21 $ 307 $30 S44 Provision for income taxes Net income S14 *In the first quarter of 2006, sales were $514.000 and net income was $4,000. Operating expenses include a nomal level of cash salary for Mr. Jones in I periods Mallings Review Tell me 24 T AaBbCeDdE AaBbCeDdE AaBbCcDr AabbCcDdE v田。 Normal No Spacing Heading 1 Heading 2 Exhibit 2 Balance Sheet at December 31, 2004-2006, and March 31, 2007 (thousands of dollars) First Quarter 2007 2004 2005 2006 Cash Accounts receivable Inventory Total current assets $45 $ 187 5.243 $.475 S 53 $231 $.228 5.562 $23 S 264 S.329 5.666 S 32 S 290 S432 5.755 Property & equlpment S 187 係74) S.113 S 252 (S 134) $ 118 $ 202 Accumulated depreciation Total PP&E. net $252 G.142) $110 $103 Total assets 5.588 S.784 S865 Accounts payable Line of credik payable Accrued expenses Long-term debt, current portion Current liabilities $36 $149 $13 5 42 $ 214 $ 14 S24 5.294 $ 120 $249 $ 14 524 $203 5250 S 12 524 5.222 Long-term debt Total liabilities S.182 S 125 5.134 S.541 S.452 5.612 Net worth .213 5.243 5.245 Total liabilities and net worth 5.588 S865 介介 Focus MocBook Pio wwbu Accounts payable Line of credit payable Accrued expenses Long-term debt, current portion S 294 Current liabilities Long-term debt Total liabilities $ 158 S.452 Net worth Total liabilities and net worth $ 213 S 665 Eahbit Dagunof epns avalble te Neln Jomes and nelated financing equiremmts Diee Firunce Long Tem Deb Teke Trade Decourts Very Lane Need fer Firncing Rase New Eiquity Bank Det Finance Long Tem Debt Forgo Tade Discount Lage Need er Financing Raise New Equity Diet Finance Moderae Ned kar Finaing Rase New Equty Fago Trade Dicounb Ne Nenl for Addioal Financing SSS.

Expert Answer:

Answer rating: 100% (QA)

1 How well is Jones Electrical Distribution performing What must Jones do well to succeed Performing electrical distribution Jones has a systemic revenue increase and net profit increase A net profit ... View the full answer

Related Book For

Posted Date:

Students also viewed these general management questions

-

What can Sheila do to reduce the reverse culture shock of expatriates and their families?

-

What can a small business do to reduce the risk associated with innovation efforts?

-

To reduce the size of the deficit (and reduce the growth of the net public debt), a politician suggests that "we should tax the rich." The politician makes a simple arithmetic calculation in which he...

-

A small ice block of mass m starts from rest from the top of an inverted bowl in the shape of a hemisphere, as shown in the figure. The hemisphere is fixed to the ground, and the block slides without...

-

At a particular college, students have several options for purchasing textbooks. The options and the proportion of students choosing each option are shown in the table at the bottom of this page. If...

-

Which of the following statements concerning the reporting of general long-term liabilities is true? a. General long-term liabilities are reported both in the governmental funds and the...

-

Why a temporary restraining order or preliminary injunction may be necessary?

-

Refer to Problem 7.3. The head of the Mariposa County Accounting Department wants to establish a standard regarding the length of time that employees can expect to wait to receive reimbursement for...

-

1a The variation of inflation rate between the U.S. and other countries have been a few percentage in general.However, the annual exchange rates between the US dollars and other foreign currencies...

-

Allstar Inc. is considering a lockbox system that would reduce its float by three days. An expected 500 collections per day will be made to the lockbox with an average payment size of $1,000. The...

-

Create an ER Diagram for a Sports team (You may choose your favorite sport). 1. Identify atleast 5 entity in the ER Diagram 2. Identify atleast one weak entity. 3. Identify atleast 3 attributes for...

-

Highland\'s Company uses the weighted - average method in its process costing system. It processes wood pulp for various manufacturers of paper products. Data relating to tons of pulp processed...

-

Mr Leong spent large sums of money in creating false records and bribing accomplices in order to conceal the fraud from auditors. He insisted that the auditor should sign a "confidentiality"...

-

Explain the impact of IPC on system security. What potential vulnerabilities are introduced by IPC mechanisms like pipes and sockets, and how can they be mitigated?

-

In Year 1 , Lee Incorporated billed its customers $ 5 7 , 7 0 0 for services performed. The company collected $ 4 1 , 4 0 0 of the amount billed. Lee incurred $ 3 7 , 6 0 0 of other operating...

-

Directions: (1) Define key concepts that could be used to reduce uncertainty in social situations. (2) Describe the ''How it's Done'' scene from Hitch. (3) Define how each character used the...

-

Yellow Shoe Company, a distributor, purchases all its shoe inventory from Styles Limited. Selected account balances are included in the following table: Dec. 31, Year 1Dec. 31, Year...

-

The activities listed in lines 2125 serve primarily as examples of A) Underappreciated dangers B) Intolerable risks C) Medical priorities D) Policy failures

-

Are some individuals more prone to react well (or poorly) to stressful situations? What types of personalities are more likely to handle stress well?

-

What about the argument that CEO pay is no more out of line than the compensation of movie stars or star athletes?

-

Do Nixon and Whitman have legitimate discrimination claims?

-

What is the ratio between the viscosities of air and water at \(10^{\circ} \mathrm{C}\) ? What is the ratio between their kinematic viscosities at this temperature and standard barometric pressure?

-

If the 10-ft-long box is floating on the oil-water system, calculate how much the box and its contents must weigh. -8 ft- 2 ft 1 ft P3.71 Oil (SG= 0.80) Water

-

Which of the following controls is most likely to help ensure that all credit revenue transactions of an entity are recorded? a. The billing department supervisor sends a copy of each approved sales...

Study smarter with the SolutionInn App