Question: 6-4 r12=0.30 B: r1.2=0.40 Chapter 06: Assignment - An Introduction to Portfolio Management A: r12=0.30 B: r12=0.40 D. A: r12=0.30 B. r12=0.40 r1,2=0.30 B: r12=0.40

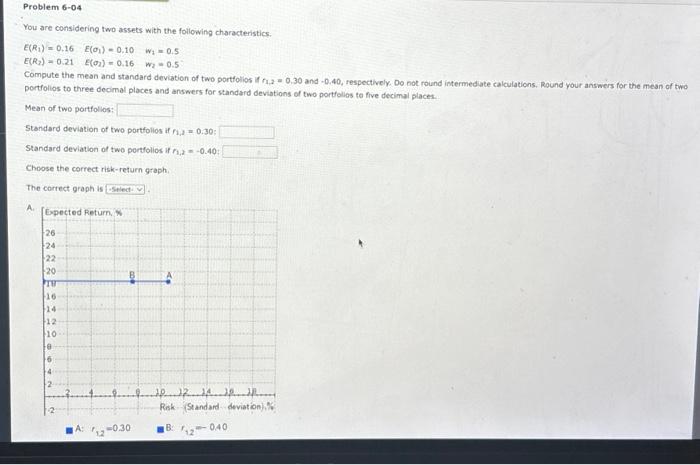

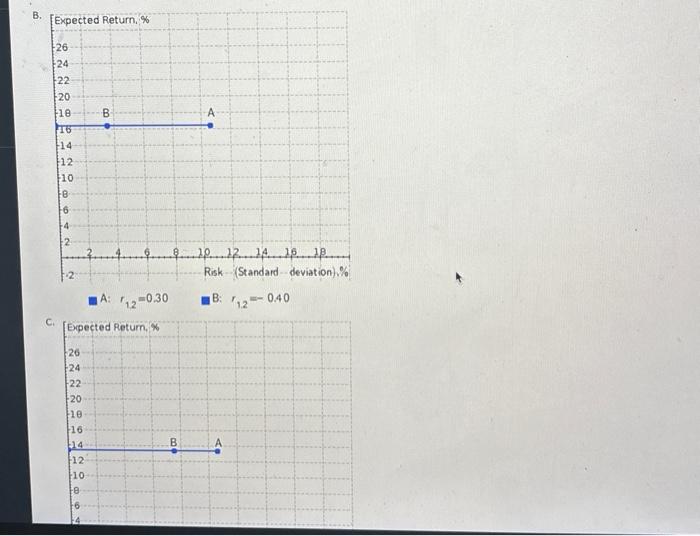

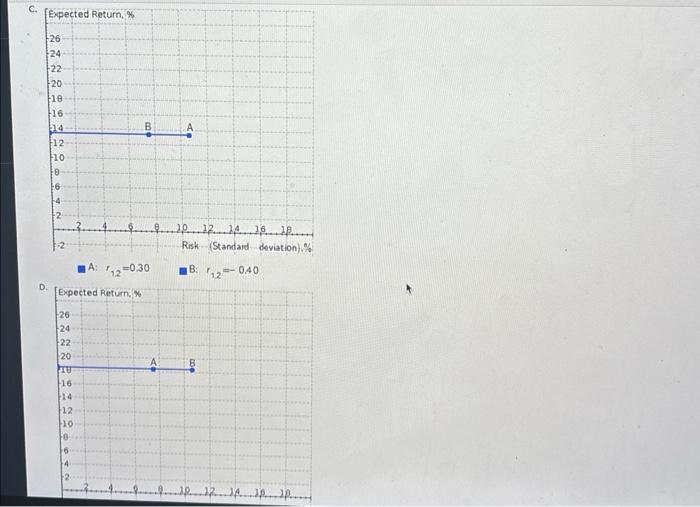

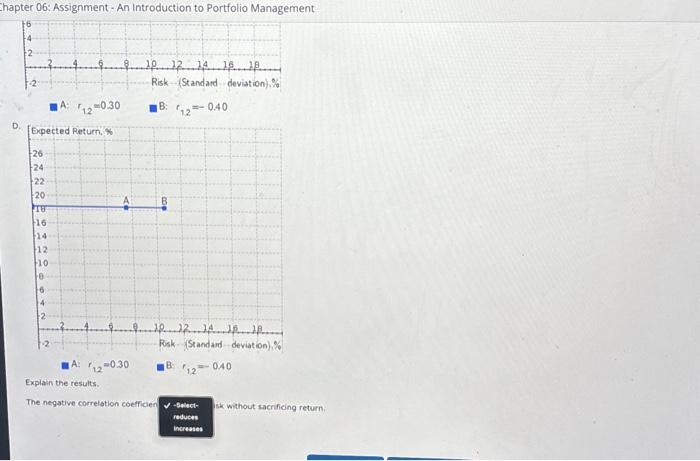

r12=0.30 B: r1.2=0.40 Chapter 06: Assignment - An Introduction to Portfolio Management A: r12=0.30 B: r12=0.40 D. A: r12=0.30 B. r12=0.40 r1,2=0.30 B: r12=0.40 You are considering two assets with the following characteristics. E(R1)=0.16E(R2)=0.21E(1)=0.10E(o2)=0.16w2=0.5w2=0.5 Compute the mean and standard deviation of two portfolios if r1,2=0,30 and -0.40 , respectively. Do not round intermedate calculations. Round your answers for the mean of two portfolios to three decimal places and answers for standard deviations of two portfolios to five decimal places. Mean of two portfolios: Standard deviation of two portfollos if f1,2=0.30; Standard deviation of two pertfolios if n2,2=0.40 : Choose the correct risk-return graph. The correct graph is A: r12=0.30 B: r12=0.40

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts