Question: 69 Security Market Line: Risk Premium Changes Conceptual Overview: Explore how risk premium changes affect the security market line. The Security Market Line defines the

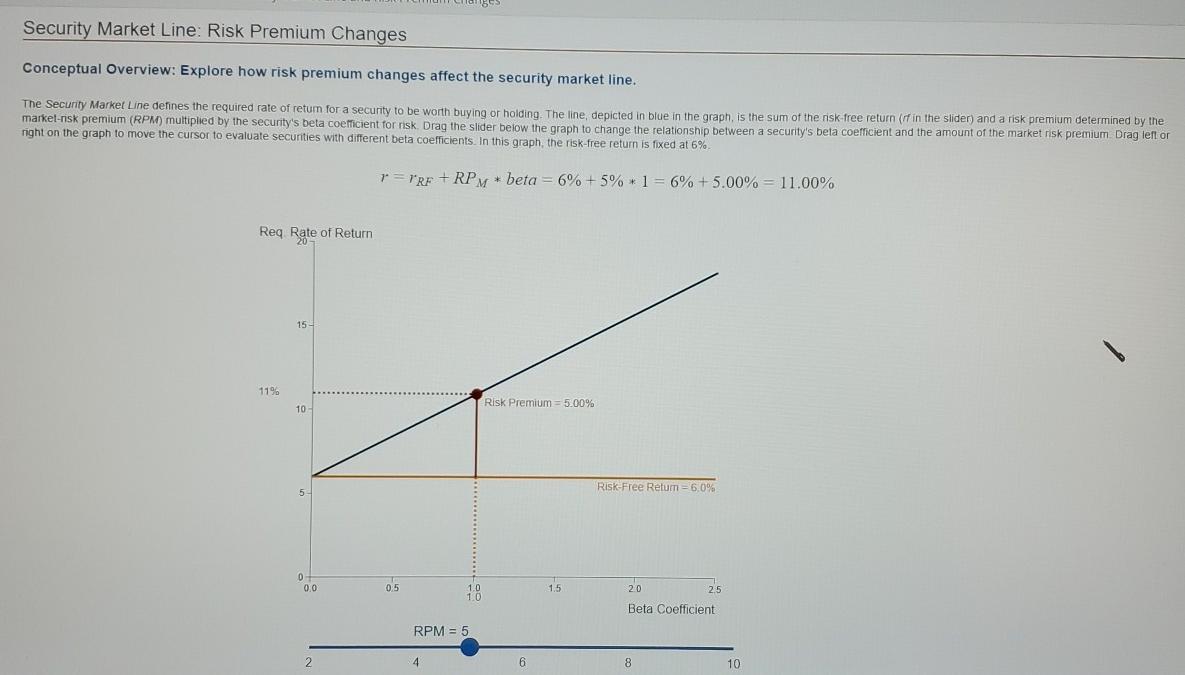

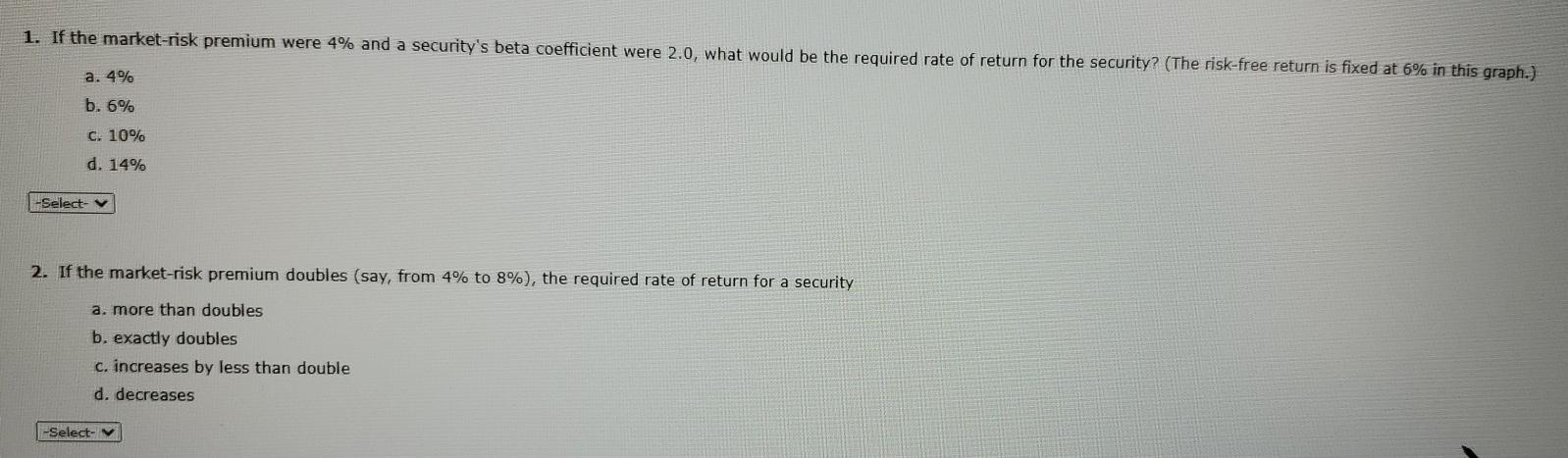

69 Security Market Line: Risk Premium Changes Conceptual Overview: Explore how risk premium changes affect the security market line. The Security Market Line defines the required rate of retum for a security to be worth buying or holding. The line, depicted in blue in the graph is the sum of the risk-free return (rf in the slider) and a risk premium determined by the market-risk premium (RPM) multiplied by the security's beta coefficient for risk. Drag the slider below the graph to change the relationship between a security's beta coefficient and the amount of the market risk premium Drag left or right on the graph to move the cursor to evaluate securities with different beta coefficients. In this graph, the risk-free return is fixed at 6% r=rre + RPM * beta = 6% +5%+ 1 = 6% +5.00% = 11.00% Req Rate of Return 15 11% 10 Risk Premium = 5.00% Risk Free Retum = 6.0% 0 0.0 0.5 1.5 18 20 25 Beta Coefficient RPM = 5 2 4 6 8 10 1. If the market-risk premium were 4% and a security's beta coefficient were 2.0, what would be the required rate of return for the security? (The risk-free return is fixed at 6% in this graph.) a. 4% b. 6% C. 10% d. 14% -Select- 2. If the market-risk premium doubles (say, from 4% to 8%), the required rate of return for a security a. more than doubles b. exactly doubles c. increases by less than double d. decreases -Select

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts