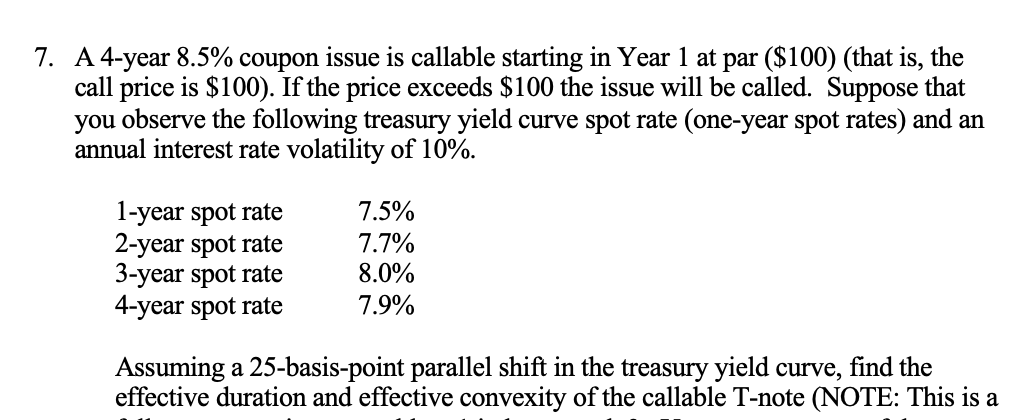

Question: 7 . A 4 - year ( 8 . 5 % ) coupon issue is callable starting in Year 1 at par

A year coupon issue is callable starting in Year at par $ that is the call price is $ If the price exceeds $ the issue will be called. Suppose that you observe the following treasury yield curve spot rate oneyear spot rates and an annual interest rate volatility of Assuming a basispoint parallel shift in the treasury yield curve, find the effective duration and effective convexity of the callable Tnote NOTE: This is a

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock