Question: 7. A pension fund manager is considering three mutual funds for investment. The first one is a stock fund, the second is a bond fund

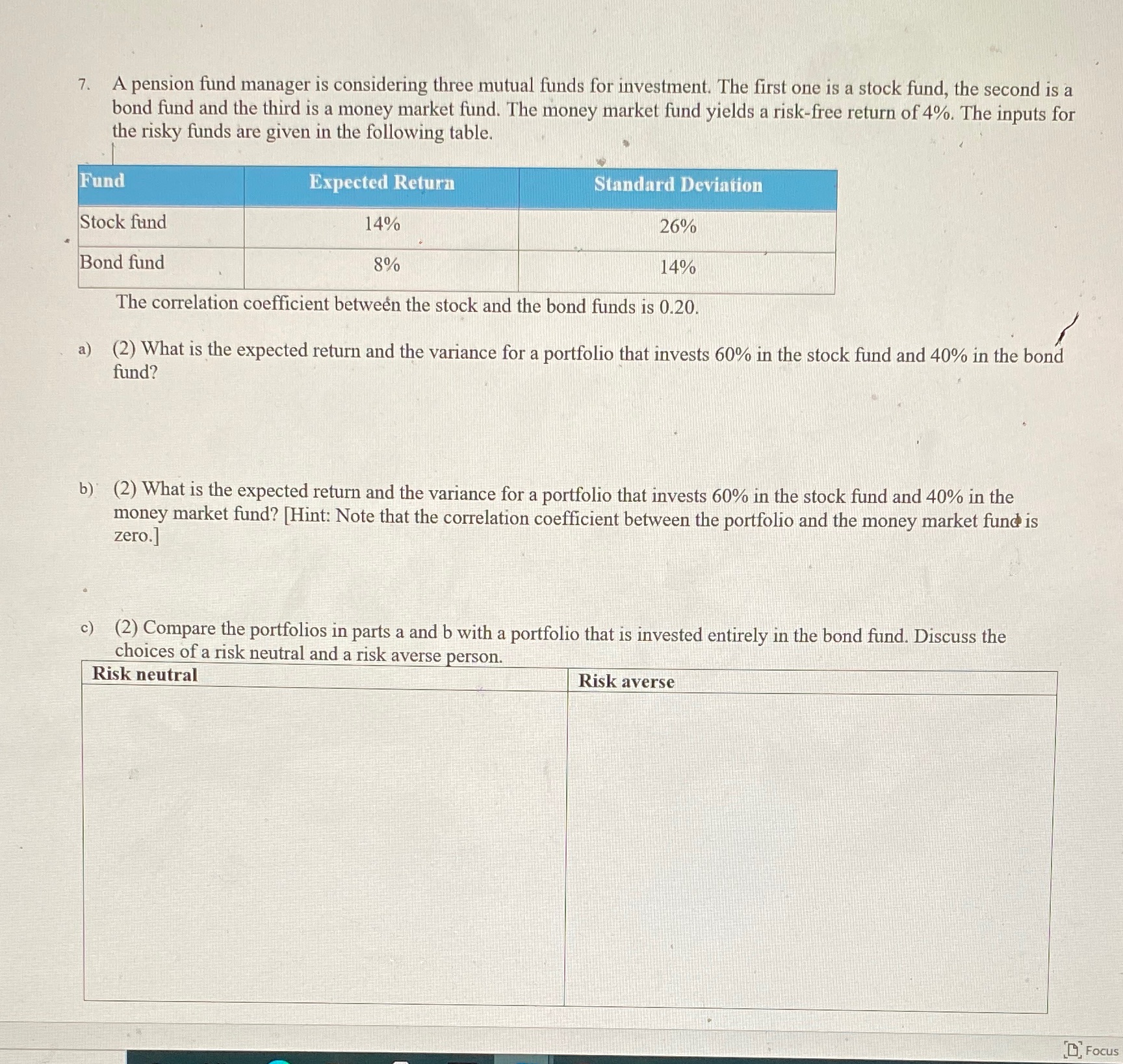

7. A pension fund manager is considering three mutual funds for investment. The first one is a stock fund, the second is a bond fund and the third is a money market fund. The money market fund yields a risk-free return of 4%. The inputs for the risky funds are given in the following table. Fund Expected Return Standard Deviation Stock fund 14% 26% Bond fund 8% 14% The correlation coefficient between the stock and the bond funds is 0.20. a) (2) What is the expected return and the variance for a portfolio that invests 60% in the stock fund and 40% in the bond fund? b) (2) What is the expected return and the variance for a portfolio that invests 60% in the stock fund and 40% in the money market fund? [Hint: Note that the correlation coefficient between the portfolio and the money market fund is zero. c) (2) Compare the portfolios in parts a and b with a portfolio that is invested entirely in the bond fund. Discuss the choices of a risk neutral and a risk averse person. Risk neutral Risk averse Focus

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts