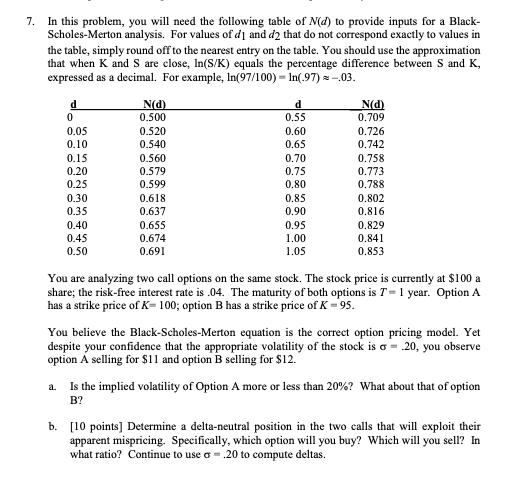

Question: 7. In this problem, you will need the following table of N(d) to provide inputs for a Black- Scholes-Merton analysis. For values of d]

7. In this problem, you will need the following table of N(d) to provide inputs for a Black- Scholes-Merton analysis. For values of d] and d2 that do not correspond exactly to values in the table, simply round off to the nearest entry on the table. You should use the approximation that when K and S are close, In(S/K) equals the percentage difference between S and K, expressed as a decimal. For example, In(97/100) - In(97) --.03. d 0 0.05 0.10 0.15 0.20 0.25 0.30 0.35 0.40 0.45 0.50 N(d) 0.500 0.520 0.540 0.560 0.579 0.599 0.618 0.637 0.655 0.674 0.691 d 0.55 0.60 0.65 0.70 0.75 0.80 0.85 0.90 0.95 1.00 1.05 N(d) 0.709 0.726 0.742 0.758 0.773 0.788 0.802 0.816 0.829 0.841 0.853 You are analyzing two call options on the same stock. The stock price is currently at $100 a share; the risk-free interest rate is .04. The maturity of both options is T = 1 year. Option A has a strike price of K= 100; option B has a strike price of K = 95. You believe the Black-Scholes-Merton equation is the correct option pricing model. Yet despite your confidence that the appropriate volatility of the stock is o = 20, you observe option A selling for $11 and option B selling for $12. a. Is the implied volatility of Option A more or less than 20%? What about that of option B? b. [10 points] Determine a delta-neutral position in the two calls that will exploit their apparent mispricing. Specifically, which option will you buy? Which will you sell? In what ratio? Continue to use a.20 to compute deltas.

Step by Step Solution

3.51 Rating (158 Votes )

There are 3 Steps involved in it

a Implied volatility of ... View full answer

Get step-by-step solutions from verified subject matter experts