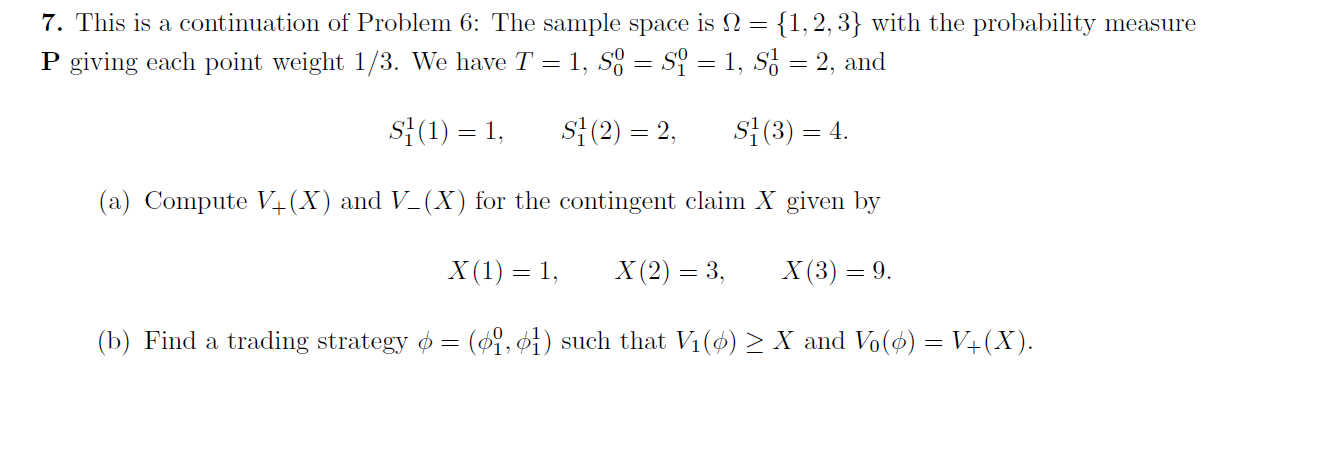

Question: 7. This is a continuation of Problem 6: The sample space is N = {1, 2, 3} with the probability measure P giving each point

7. This is a continuation of Problem 6: The sample space is N = {1, 2, 3} with the probability measure P giving each point weight 1/3. We have T = 1, so = Si = 1, S7 = 2, and S](1) = 1, S](2) = 2, S7(3) = 4. (a) Compute V+(X) and V_(X) for the contingent claim X given by X(1) = 1, X(2) = 3, X(3) = 9. (b) Find a trading strategy o = (07,01) such that Vi(0) > X and V.(0) = V+(X). 7. This is a continuation of Problem 6: The sample space is N = {1, 2, 3} with the probability measure P giving each point weight 1/3. We have T = 1, so = Si = 1, S7 = 2, and S](1) = 1, S](2) = 2, S7(3) = 4. (a) Compute V+(X) and V_(X) for the contingent claim X given by X(1) = 1, X(2) = 3, X(3) = 9. (b) Find a trading strategy o = (07,01) such that Vi(0) > X and V.(0) = V+(X)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts