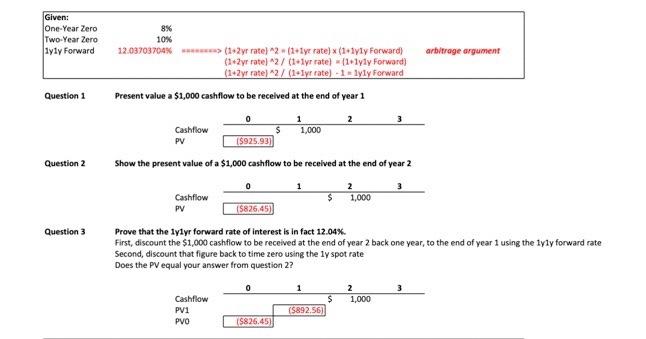

Question: 8% Given: One-Year Zero Two-Year Zero ayly Forward arbitrage argument Question 1 0 10% 12.03703704%> (12yr rate) 2 (1+ly rate) x (1+lyly Forward) (12yr ratel

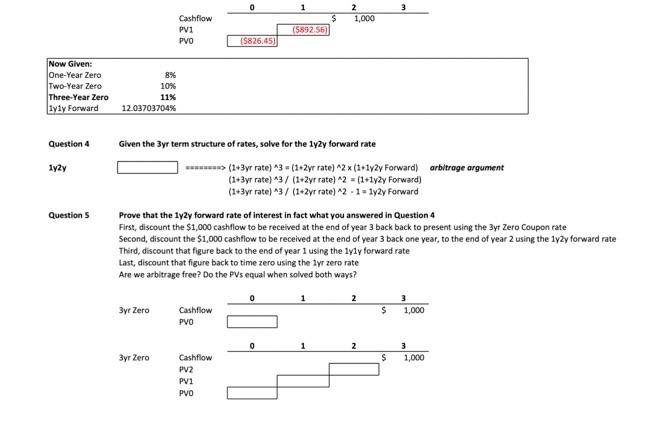

8% Given: One-Year Zero Two-Year Zero ayly Forward arbitrage argument Question 1 0 10% 12.03703704%> (12yr rate) 2 (1+ly rate) x (1+lyly Forward) (12yr ratel 2/ (lyr rate) 11.lyly Forward) (12yr rate)2 / (1+Iyt rate) - 1 e lyly Forward Present value a $1,000 cashflow to be received at the end of year 1 2 Cashflow $ 1,000 PV ($925.93) Show the present value of a $1,000 cashflow to be received at the end of year 2 2 Cashflow $ 1,000 PV (5826,45) Question 2 0 1 Question 3 Prove that the lylyr forward rate of interest is in fact 12.04%. First, discount the $1,000 cashfiow to be received at the end of year 2 back one year, to the end of year 1 using the lyly forward rate Second, discount that figure back to time zero using the ly spot rate Does the PV equal your answer from question 2? 0 Cashflow 1 $ (5892.56) 2 1,000 PV1 PVO ($826.45) 1 3 2 1,000 $ Cashflow PV1 PVO (5892.56) (5826.65) Now Glven: One-Year Zero Two-Year Zero Three-Year Zero iyiy Forward 8% 10% 11% 12.03703704% Question 4 1927 Given the 3yr term structure of rates, selve for the 1y2y forward rate -> (1+3yr rate) 3 = (1-2yr rate) "2 x (1+12y Forward) arbitrage argument (1+3yr rate) *3 / (1+2yr rate)^2 = (1+12y Forward) (1+3yr rate)^3 / (1+2yr rate)^2 - 1=192y Forward Questions Prove that the lyzy forward rate of interest in fact what you answered in Question 4 First, discount the $1,000 cashflow to be received at the end of year 3 back back to present using the Byr Zero Coupon rate Second, discount the $1,000 cashflow to be received at the end of year 3 back one year, to the end of year 2 using the ly2y forward rate Third, discount that figure back to the end of year 1 using the lyly forward rate Last, discount that figure back to time zero using the lyr zero rate Are we arbitrage free? Do the PVs equal when solved both ways? o 1 2 3yr Zero 3 1,000 $ Cashflow PVO 0 2 3yr Zero 3 1,000 $ Cashflow PV2 PV1 PVO

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts