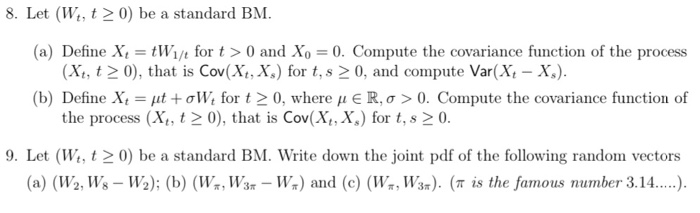

Question: 8. Let (W, t > 0) be a standard BM. (a) Define X = tW1/for t0 and Xo = 0. Compute the covariance function of

8. Let (W, t > 0) be a standard BM. (a) Define X = tW1/for t0 and Xo = 0. Compute the covariance function of the process (Xt, t > 0), that is Cov(X+, X:) for t,s > 0, and compute Var(X+ - X). (b) Define X, = ut + OW, for t > 0, where u ERO > 0. Compute the covariance function of the process (X, t > 0), that is Cov(X4, X,) for t, s > 0. 9. Let (W, t > 0) be a standard BM. Write down the joint pdf of the following random vectors (a) (W2, W3 - W2); (b) (W-,W3+ - W.) and (c) (W., W36). (is the famous number 3.14....... 8. Let (W, t > 0) be a standard BM. (a) Define X = tW1/for t0 and Xo = 0. Compute the covariance function of the process (Xt, t > 0), that is Cov(X+, X:) for t,s > 0, and compute Var(X+ - X). (b) Define X, = ut + OW, for t > 0, where u ERO > 0. Compute the covariance function of the process (X, t > 0), that is Cov(X4, X,) for t, s > 0. 9. Let (W, t > 0) be a standard BM. Write down the joint pdf of the following random vectors (a) (W2, W3 - W2); (b) (W-,W3+ - W.) and (c) (W., W36). (is the famous number 3.14

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts