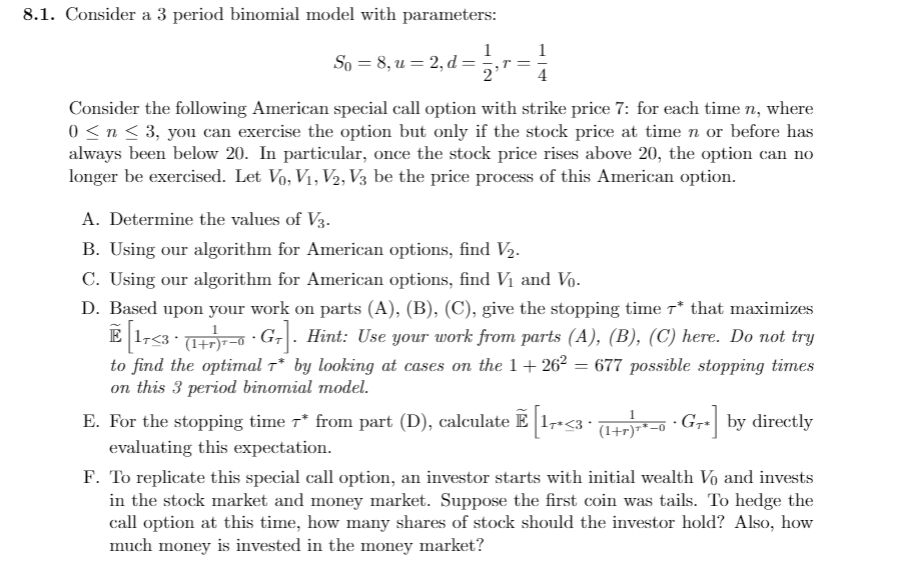

Question: 8.1. Consider a 3 period binomial model with parameters: 1 So = 8,u=2,d= 1 Consider the following American special call option with strike price 7:

8.1. Consider a 3 period binomial model with parameters: 1 So = 8,u=2,d= 1 Consider the following American special call option with strike price 7: for each time n, where 0

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts