Question: 8-C. Assemble the following from previous continuous problems: (1) the governmental funds Balance Sheet and Statement of Revenues, Expenditures, and Changes in Fund Balances from

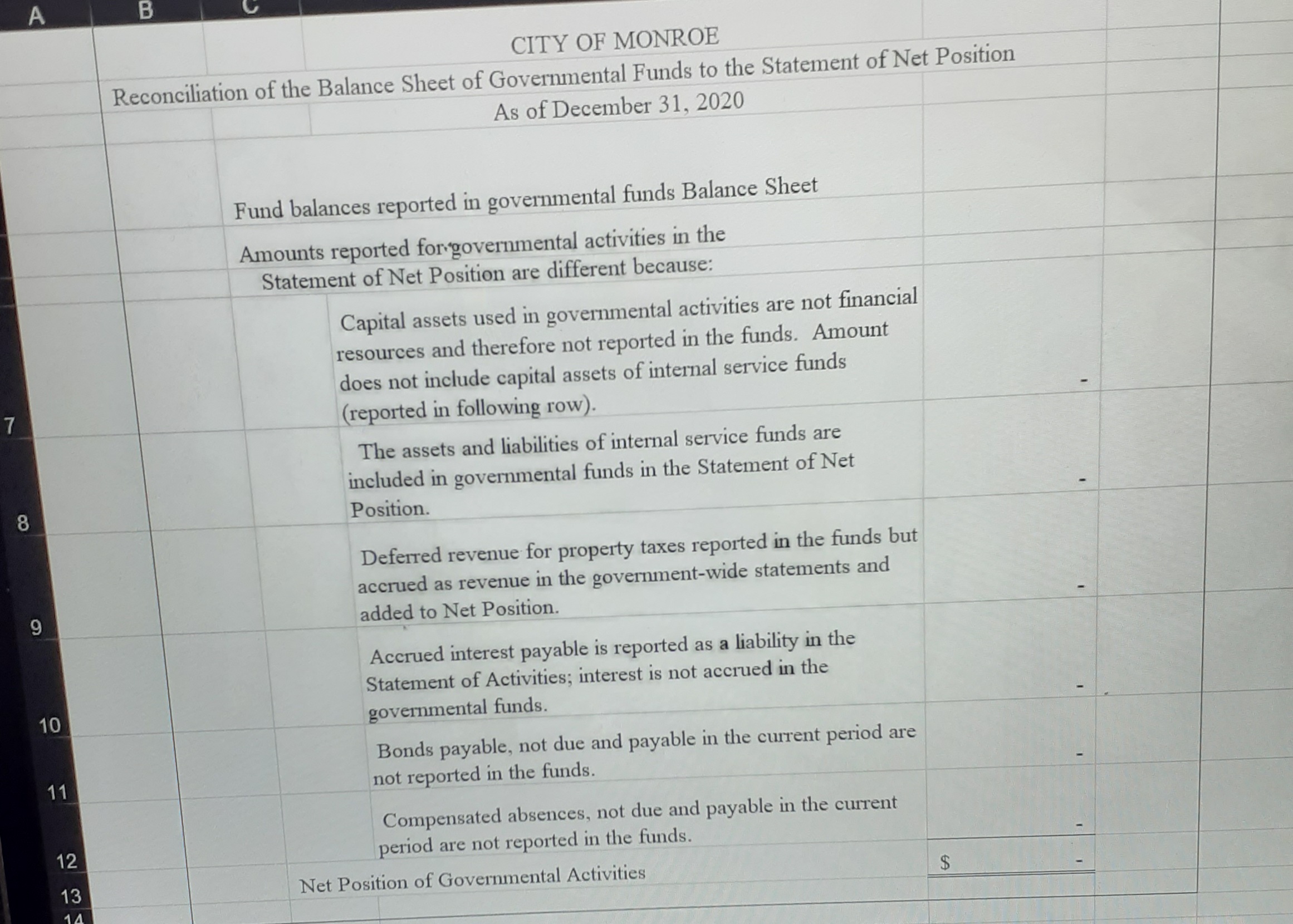

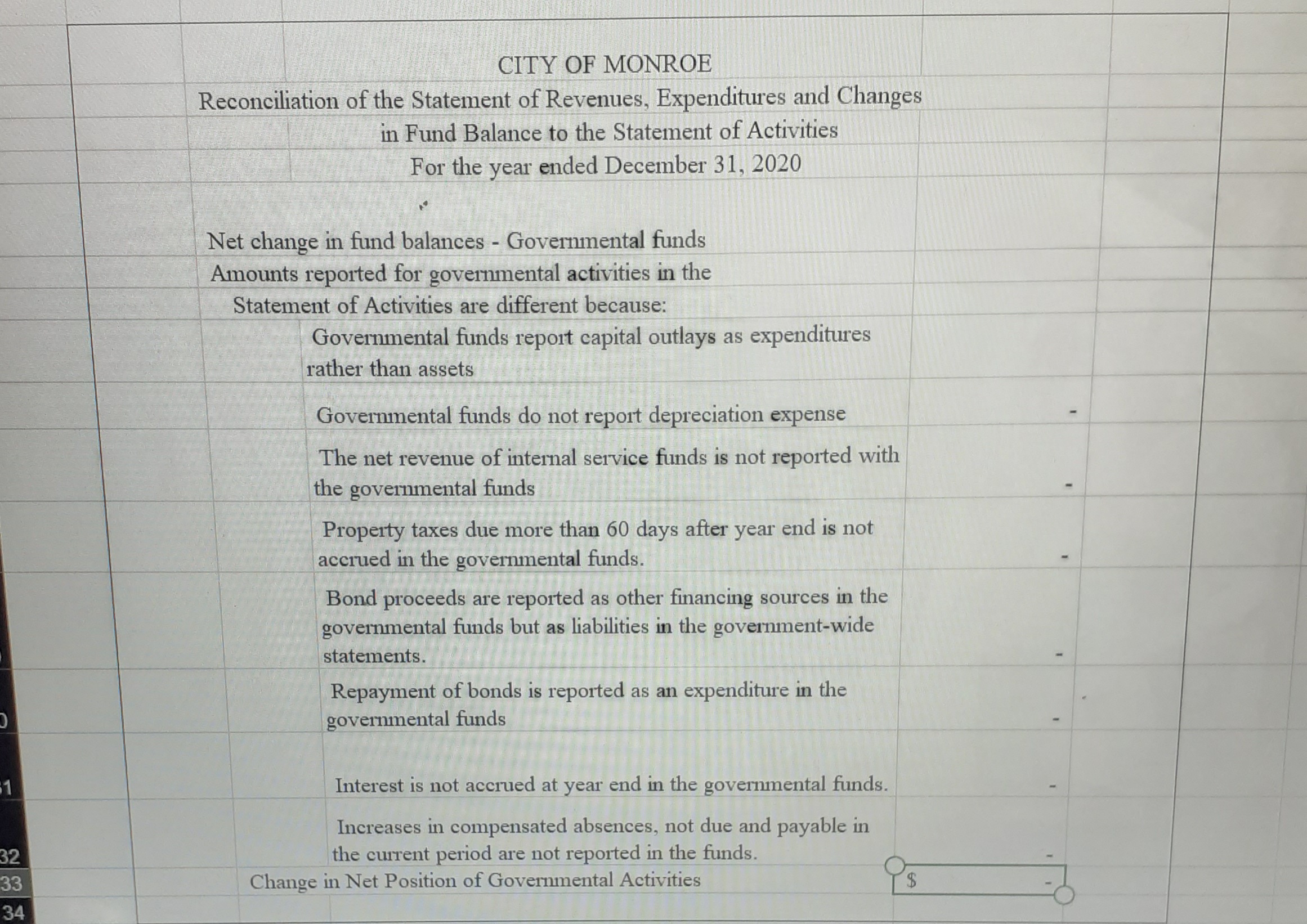

8-C. Assemble the following from previous continuous problems: (1) the governmental funds Balance Sheet and Statement of Revenues, Expenditures, and Changes in Fund Balances from Section 5-C; (3) the proprietary funds Statement of Net Position and Statement of Revenues, Expenses, and Changes in Fund Net Position from Section 6-C. (Please right click on the attached document and select open in new window. Then, download the template and enter the required values in the appropriate fields. Save your completed template to your computer and then upload it here by clicking "Browse." Next, click "Save.") Required: " 1. Start a worksheet for adjustments, using the trial balance format illustrated in the text (i.e. list accounts with debit balances first, then accounts with credit balances). Enter the balances from the governmental funds financial statements prepared for Section 5-C. When doing this, follow the following guidelines: . Net Position: Use a single account for net position (which will include the beginning balance of all fund balance accounts). . Intergovernmental Revenues: When setting up the worksheet, set up separate lines for the intergovernmental revenues as follows: State Grant for Highway and Street Maintenance $1, 067, 500 Operational Grant-General Government 332, 000 Capital Grant-Public Safety 1, 335,000 Total $2, 734, 500 . Capital Assets: It is not necessary to set up separate lines for different classes of capital (fixed) assets or accumulated depreciation (simply use one row for Capital Assets and another for Accumulated Depreciation). . Confirm that the total debits and credits equal. 2. Prepare worksheet entries and post to the worksheet for the following items. Identify each adjustment by the letter used in the problem:2. Prepare worksheet entries and post to the worksheet for the following items. Identify each adjustment by the letter used in the problem: a. Record the January 1, 2020 balances of general fixed asset and related accumulated depreciation accounts. The City of Monroe had the following balances (excluding Internal Service Funds): Cost Accumulated Depreciation Totals $67 , 900, 000 $32, 000, 000 b. Eliminate the capital expenditures shown in the governmental funds Statement of Revenues, Expenditures, and Changes in Fund Balances. c. Depreciation Expense (governmental activities) for the year totaled $5,130,000. d. Eliminate the other financing sources from the sale of bonds by recording a liability for bonds payable and the related premium. e. As of January 1, 2020, the City of Monroe had $12,000,000 in general obligation bonds outstanding. f. Eliminate the expenditures for bond principal. g. Accrue interest in the amount of $328,000. (Two bond issues were outstanding; interest payments for both were last made on July 1, 2020. The computation is as follows: ($11,200,000 x 0.03 x 6/12) + ($4,000,000 x 0.08 x 6/12) = $328,000). h. Adjust for the interest accrued in the prior year government-wide statements, but recorded as an expenditure in the 2020 fund basis statements, ($12,000,000 x 0.03 x 6/12) = $180,000. i. Amortize bond premium in the amount of $10,000. j. Make adjustments for additional revenue accrual. The only adjustment is for property taxes to eliminate the current year deferral of property taxes. k. Adjust for the $21,000 of property taxes that was deferred in 2019 and recognized as revenue in the 2020 fund-basis statements. 1. Assume the City adopted a policy in 2020 of allowing employees to accumulate compensated absences. Make an adjustment accruing the expense of $42,000 Charge compensated absences expense. m Dring in the halancer of the internal corviro fund halance choot accounts Anain Ice a cinnlo account for all canital accote and a corAnd account for allj. Make adjustments for additional revenue accrual. The only adjustment is for property taxes to eliminate the current year deferral of property taxes. k. Adjust for the $21,000 of property taxes that was deferred in 2019 and recognized as revenue in the 2020 fund-basis statements. 1. Assume the City adopted a policy in 2020 of allowing employees to accumulate compensated absences. Make an adjustment accruing the expense of $42,000 Charge compensated absences expense. m. Bring in the balances of the internal service fund balance sheet accounts. Again, use a single account for all capital assets and a second account for all accumulated depreciation balances (use a separate column of the worksheet to enter Internal Service Fund entries). n. No revenues from internal service funds were with external parties. Assume $3,200 of the $11,200 "Due from Other Funds" in the internal service accounts represents a receivable from the General Fund and the remaining $8,000 is due from the enterprise fund. Eliminate the $3,200 interfund receivables. o. Reduce governmental fund expenses by the net operating profit of internal service funds. As the amount is small, reduce general government expenses for the entire amount. p. Eliminate transfers that are between departments reported within governmental activities. 3. Prepare a Statement of Activities for the City of Monroe for the Year Ended December 31, 2020. For purposes of this statement, assume: . $332,000 in the General Fund is a state grant specifically to support general government programs. . $1,067,500 in the Street and Highway Fund is an operating grant specifically for highway and street maintenance expenses. . $1,335,000 in the City Jail Construction Fund is a capital grant that applies to public safety. Use the balances computed from the worksheet completed in part 2 for the governmental activities portion of the statement. Use the solution to P6-C (Enterprise fund) to prepare the business activities portion (net any short-term interfund payables/receivables). 4. Prepare a Statement of Net Position for the City of Monroe as of December 31, 2020. Group all capital assets, net of depreciation. Include a breakdown in the Net Position section for (a) Capital Assets, net of related debt, (b) Restricted, and (c) Unrestricted. For purposes of classifying net position for the governmental activities, assume:Use the balances computed from the worksheet completed in part 2 for the governmental activities portion of the statement. Use the solution to P6-C (Enterprise fund) to prepare the business activities portion (net any short-term interfund payables/receivables). 4. Prepare a Statement of Net Position for the City of Monroe as of December 31, 2020. Group all capital assets, net of depreciation. Include a breakdown in the Net Position section for (a) Capital Assets, net of related debt, (b) Restricted, and (c) Unrestricted. For purposes of classifying net position for the governmental activities, assume: . For the governmental activities net position invested in capital assets, net of related debt, the related debt includes the bonds payable, the premium on bonds payable, and the advance from the water utility fund. . The special revenue fund resources are restricted by the granting agency for street and highway maintenance. Assume $204,500 are the only restricted resources in the governmental activities. 5. Prepare the reconciliation necessary to convert from the fund balance reported in the governmental funds Balance Sheet to the Net Position in the government- wide Statement of Net Position. 6. Prepare the reconciliation necessary to convert from the change in fund balances in the governmental funds Statement of Revenues, Expenditures, and Changes in Fund Balances to the change in net position in the government-wide Statement of Activities.Enter all amounts as positive numbers. The worksheet is formatted to add debits to assets & expenses and add credits to revenues, liabilities & equity Gov'tal Govern- mental Balances Ref Fund Account Titles Debits Credits Funds for Gov't- Balances Adjustments & Eliminations Adjusted Internal Service Funds wide Stmts Debits Credits Debits Credits A type debit accounts in this column DEBITS: type credit accounts in this column Cash 541,400 541.400 541.400 Cash with Fiscal Agent 760,000 760.000 760,000 Investments 263,000 263,000 263,000 Taxes Receivable, net 457,500 457.500 457,500 Interest Receivable, net 16,850 16.850 16,850 Inventories Due from State Govt. 557,500 557.500 557,500 Due from Other Funds Capital Assets ....... both rows Expenditures (expenses) Current General Govt. 1,649,000 1.649,000 1,649,000 Public Safety 3,066,900 3.066,900 3.066,900 Highway and Streets 2,481,900 2.481.900 2,481,900 Sanitation 591,400 591,400 591,400 Health 724,100 724,100 724.100 Welfare 374,300 374.300 374.300 Culture and Recreation 917,300 917.300 917,300 Compensated Absences Exp Other Expenditures (expenses) - Debt Service Principal 800,000 800.000 800.000 - Interest (expenditure/expense) 614,000 514.000 514.000 both rows - Capital Outlay 5,821, 100 5.821,100 5,821,100 - Depreciation Other Fin. Uses - Transfers Out 1,868,700 1868.700 1.868,700 32 21.404.950 Total Debits 21,404,950 33 CREDITS: 34 263.800 263,800 35 Accounts Payable 263,800G H K - Interest (expenditure/expense) M N O P 514,000 R S both rows 514.000 514,000 Capital Outlay 5,821,100 Depreciation 5.821.100 5,821,100 Other Fin. Uses - Transfers Out 1,868,700 1,868,700 1,868,700 Total Debits 21,404,950 CREDITS: 21,404,950 Accounts Payable 263,800 Due to Other Funds 263.800 263,800 40,200 Accrued Interest Payable 40,200 40,200 Bonds Payalbe both rows ........ Premium on Bonds Compensated Absence Payable Advance from Water Utility Fund Deferred Inflows: Property Taxes 17,500 17.500 17,500 Accumulated Depreciation both rows Revenues Property Taxes 6,846,000 6.846,000 6,846,000 Sales Taxes 2,938,000 2.938,000 2,938,000 Interest 18,000 18.000 18,000 Licenses & Permits 800,000 800.000 800,000 Miscellaneous 350,000 350.000 350,000 State Grant for Highway Street Exper 1,067,500 1.067.500 1,067,500 Capital Grant- Gen Gov't 332,000 332.000 332,000 Capital Grant- Public Safety 1,335,000 1.335.000 1,335,000 Other Financing Sources Proceeds of Bonds 4,000,000 4.000.000 4,000,000 Premium on Bonds 200,000 200.000 200,000 Transfers In 1,868,700 1.868.700 1,868,700 Net Position at beginning of year three rows -.... 1,328,250 1.328.250 1,328,250 21,404.950 Total Credits 21,404,950 column totals: debits = credits ??A B C D E H K Program Revenues Net (Expense) Revenue and Change in Net Position Operational Capital Business Charges for Grants and Grants and Governmental Type Expenses Services Contributions Contributions Activities Activities Total Functions/Programs Governmental Activities: General Government $ Public Safety Highways and Streets Sanitation Health Welfare Culture and Recreation Depreciaiton Interest 4 Compensated Absneces 15 Total Governmental Activities 16 Business Type Activities 17 Water and Sewer 18 Total Government $ $ $ $ $ - $ 19 20 General Revenues 21 Taxes: 22 Property Taxes 23 Sales Taxes 24 Interest 25 licenses and Permits 26 Miscellaneous Total General Revenues 28 Change in Net Position 29 Net Position, Beginning 30 Net Position, Ending $ $ $ 31 32 33G H Governmental Business-Type Activities Activities Assets Total Cash Cash with Fiscal Agents $ Investments Accounts Receivable (Net) Taxes Receivable (Net) Interest Receivable Internal Balances Current Net the amounts: due from and (due to) other funds 0 Due from Other Governments Inventories Internal Balances Long-Term 13 Restricted Assets 14 Capital Assets, Net of Accumulated Depreciation 15 Total Assets $ $ $ 16 17 Liabilities 18 Accounts Payable 19 Payroll Taxes Payable 20 Accrued Interest Payable 21 Revenue Bonds Payable 22 General Obligation Bonds Payable 23 Premium on Bonds Sold 24 Compensated Absences Payable 25 Total Liabilities 26 27 Net Position 28 Net Investment in Capital Assets 29 Restricted 30 Unrestricted 31 Total Net Position $ $ $ 32 33 34A B CITY OF MONROE Reconciliation of the Balance Sheet of Governmental Funds to the Statement of Net Position As of December 31, 2020 Fund balances reported in governmental funds Balance Sheet Amounts reported for governmental activities in the Statement of Net Position are different because: Capital assets used in governmental activities are not financial resources and therefore not reported in the funds. Amount does not include capital assets of internal service funds (reported in following row). The assets and liabilities of internal service funds are included in governmental funds in the Statement of Net 8 Position. Deferred revenue for property taxes reported in the funds but accrued as revenue in the government-wide statements and 9 added to Net Position. Accrued interest payable is reported as a liability in the Statement of Activities; interest is not accrued in the 10 governmental funds. Bonds payable, not due and payable in the current period are 11 not reported in the funds. Compensated absences, not due and payable in the current 12 period are not reported in the funds. 13 Net Position of Governmental Activities $CITY OF MONROE Reconciliation of the Statement of Revenues, Expenditures and Changes in Fund Balance to the Statement of Activities For the year ended December 31, 2020 Net change in fund balances - Governmental funds Amounts reported for governmental activities in the Statement of Activities are different because: Governmental funds report capital outlays as expenditures rather than assets Governmental funds do not report depreciation expense The net revenue of internal service funds is not reported with the governmental funds Property taxes due more than 60 days after year end is not accrued in the governmental funds. Bond proceeds are reported as other financing sources in the governmental funds but as liabilities in the government-wide statements. Repayment of bonds is reported as an expenditure in the governmental funds Interest is not accrued at year end in the governmental funds. Increases in compensated absences, not due and payable in 32 the current period are not reported in the funds. 33 Change in Net Position of Governmental Activities 34

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock

Students Have Also Explored These Related Accounting Questions!