Question: 9. You have performance data for two portfolio managers and a common benchmark portfolio: Benchmark Manager A Weight Return Weight Return Manager B Weight

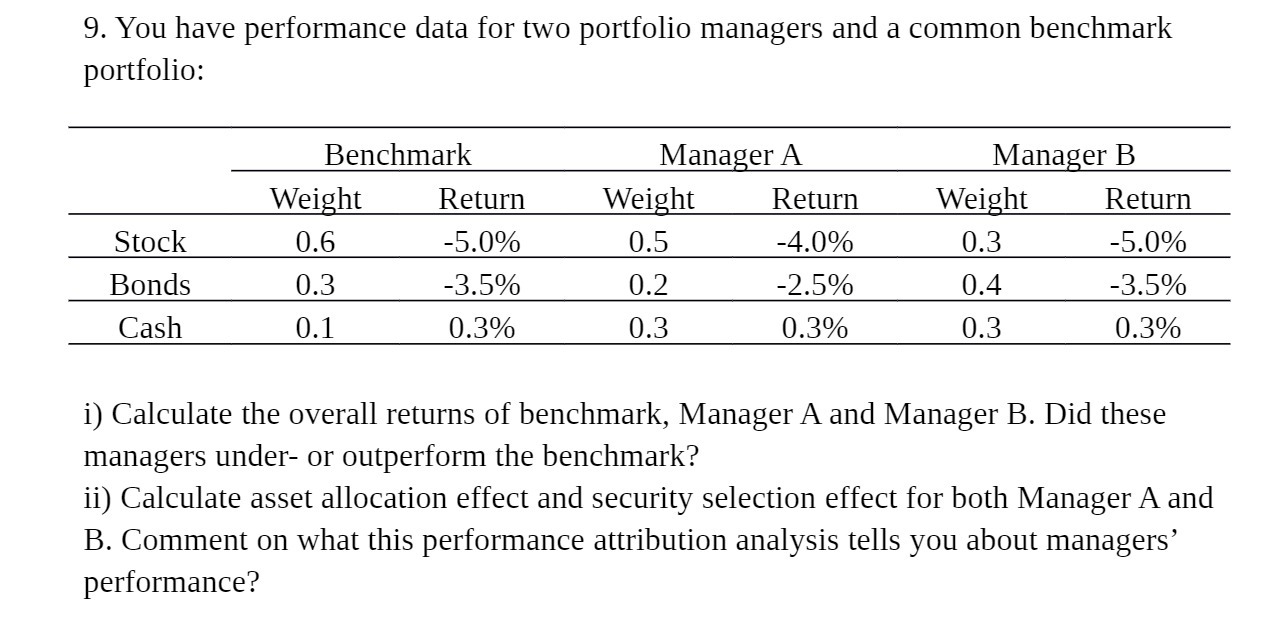

9. You have performance data for two portfolio managers and a common benchmark portfolio: Benchmark Manager A Weight Return Weight Return Manager B Weight Return Stock 0.6 -5.0% 0.5 -4.0% 0.3 -5.0% Bonds 0.3 -3.5% 0.2 -2.5% 0.4 -3.5% Cash 0.1 0.3% 0.3 0.3% 0.3 0.3% i) Calculate the overall returns of benchmark, Manager A and Manager B. Did these managers under- or outperform the benchmark? ii) Calculate asset allocation effect and security selection effect for both Manager A and B. Comment on what this performance attribution analysis tells you about managers' performance?

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts