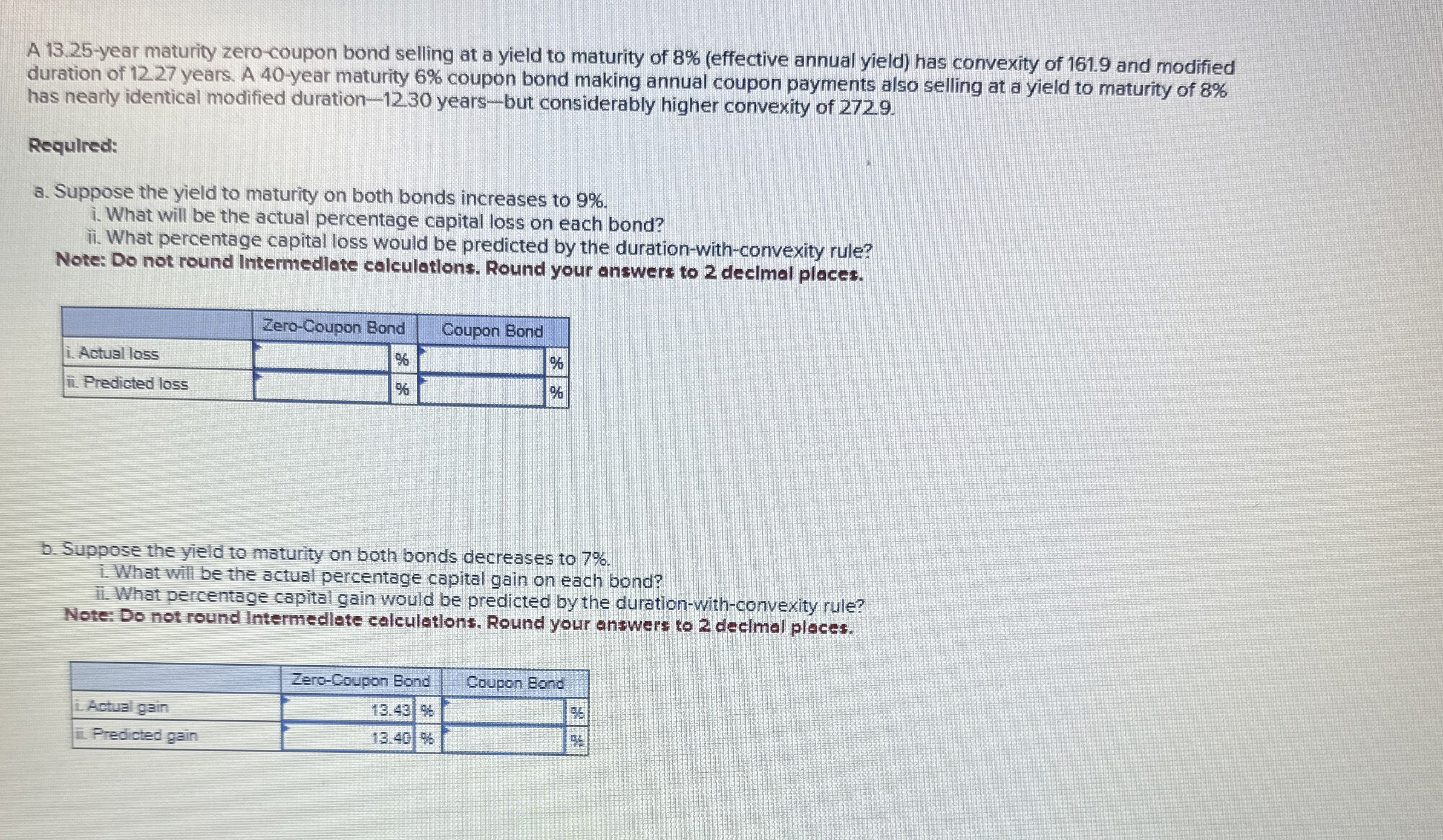

Question: A 1 3 . 2 5 - year maturity zero - coupon bond selling at a yield to maturity of 8 % ( effective annual

A year maturity zerocoupon bond selling at a yield to maturity of effective annual yield has convexity of and modified duration of years. A year maturity coupon bond making annual coupon payments also selling at a yield to maturity of has nearly identical modified duration yearsbut considerably higher convexity of

Required:

a Suppose the yield to maturity on both bonds increases to

i What will be the actual percentage capital loss on each bond?

ii What percentage capital loss would be predicted by the durationwithconvexity rule?

Note: Do not round Intermedlate calculatlons. Round your answers to decimal places.

tableZeroCoupon Bond,Coupon Bond,i Actual loss,,ii Predicted loss,,

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock