Question: a. If the returns of assets V and W are perfectly positively correlated (correlation coefficient = +1), all possible portfolio combinations will have: (Select

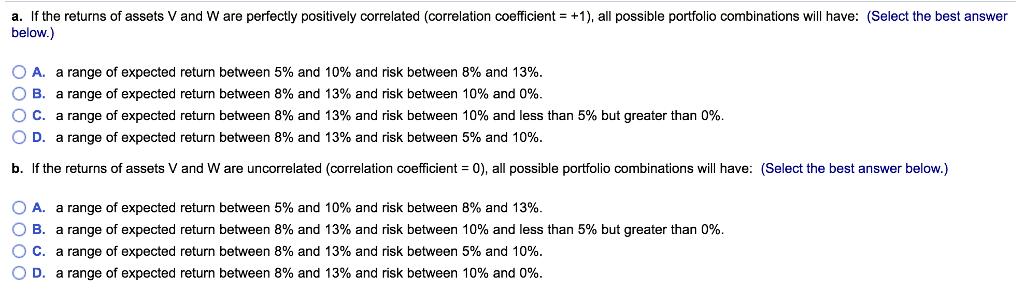

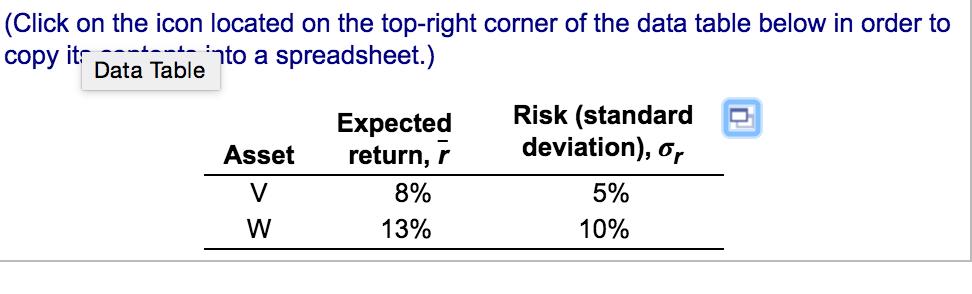

a. If the returns of assets V and W are perfectly positively correlated (correlation coefficient = +1), all possible portfolio combinations will have: (Select the best answer below.) O A. a range of expected return between 5% and 10% and risk between 8% and 13%. OB. a range of expected return between 8% and 13% and risk between 10% and 0%. O C. a range of expected return between 8% and 13% and risk between 10% and less than 5% but greater than 0%. O D. a range of expected return between 8% and 13% and risk between 5% and 10%. b. If the returns of assets V and W are uncorrelated (correlation coefficient = 0), all possible portfolio combinations will have: (Select the best answer below.) O A. a range of expected return between 5% and 10% and risk between 8% and 13%. OB. a range of expected return between 8% and 13% and risk between 10% and less than 5% but greater than 0%. O C. a range of expected return between 8% and 13% and risk between 5% and 10%. D. a range of expected return between 8% and 13% and risk between 10% and 0%. c. If the returns of assets V and W are perfectly negatively correlated (correlation coefficient = -1), all possible portfolio combinations will have: (Select the best answer below.) O A. a range of expected return between 5% and 10% and risk between 8% and 13%. O B. a range of expected return between 8% and 13% and risk between 10% and 0%. OC. a range of expected return between 8% and 13% and risk between 5% and 10%. O D. a range of expected return between 8% and 13% and risk between 10% and less than 5% but greater than 0%. (Click on the icon located on the top-right corner of the data table below in order to copy it into a spreadsheet.) Data Table Asset V W Expected return, r 8% 13% Risk (standard deviation), or 5% 10% T

Step by Step Solution

3.57 Rating (157 Votes )

There are 3 Steps involved in it

a If the returns of assets V and W are perfectly positively correlated ... View full answer

Get step-by-step solutions from verified subject matter experts