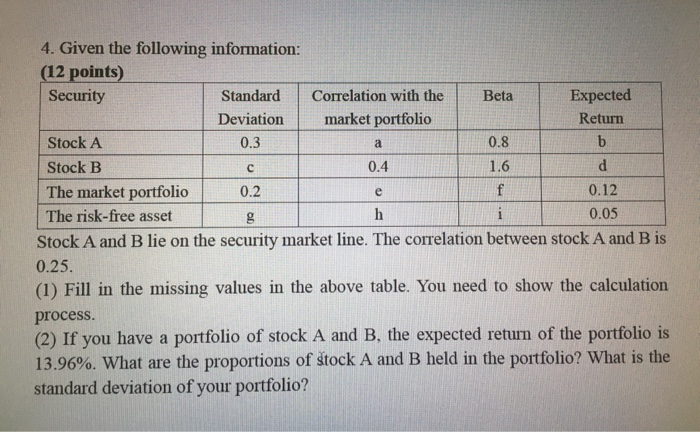

Question: a 4. Given the following information: (12 points) Security Standard Correlation with the Beta Expected Deviation market portfolio Return Stock A 0.3 0.8 b Stock

a 4. Given the following information: (12 points) Security Standard Correlation with the Beta Expected Deviation market portfolio Return Stock A 0.3 0.8 b Stock B 0.4 1.6 d The market portfolio 0.2 f 0.12 The risk-free asset g h i 0.05 Stock A and B lie on the security market line. The correlation between stock A and B is 0.25. (1) Fill in the missing values in the above table. You need to show the calculation process. (2) If you have a portfolio of stock A and B, the expected return of the portfolio is 13.96%. What are the proportions of stock A and B held in the portfolio? What is the standard deviation of your portfolio

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock