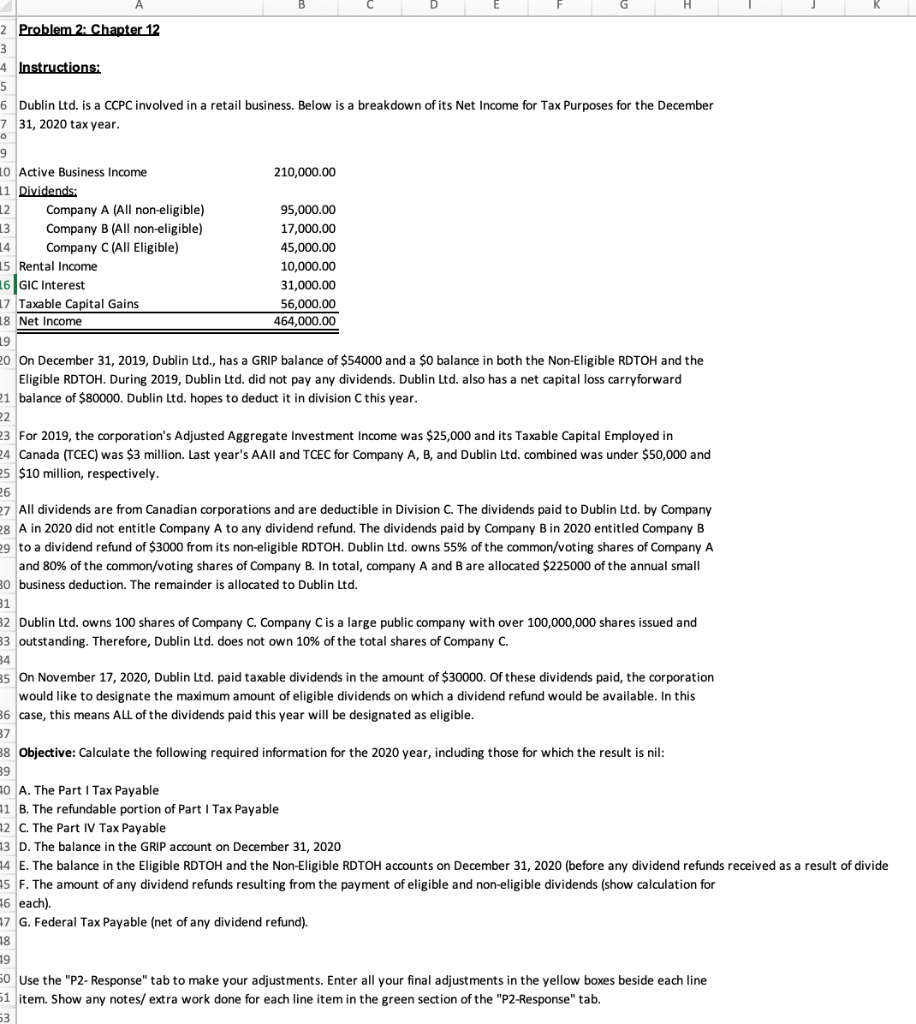

Question: A B 2 Problem 2: Chapter 12 3 4 Instructions: 5 6 Dublin Ltd. is a CCPC involved in a retail business. Below is a

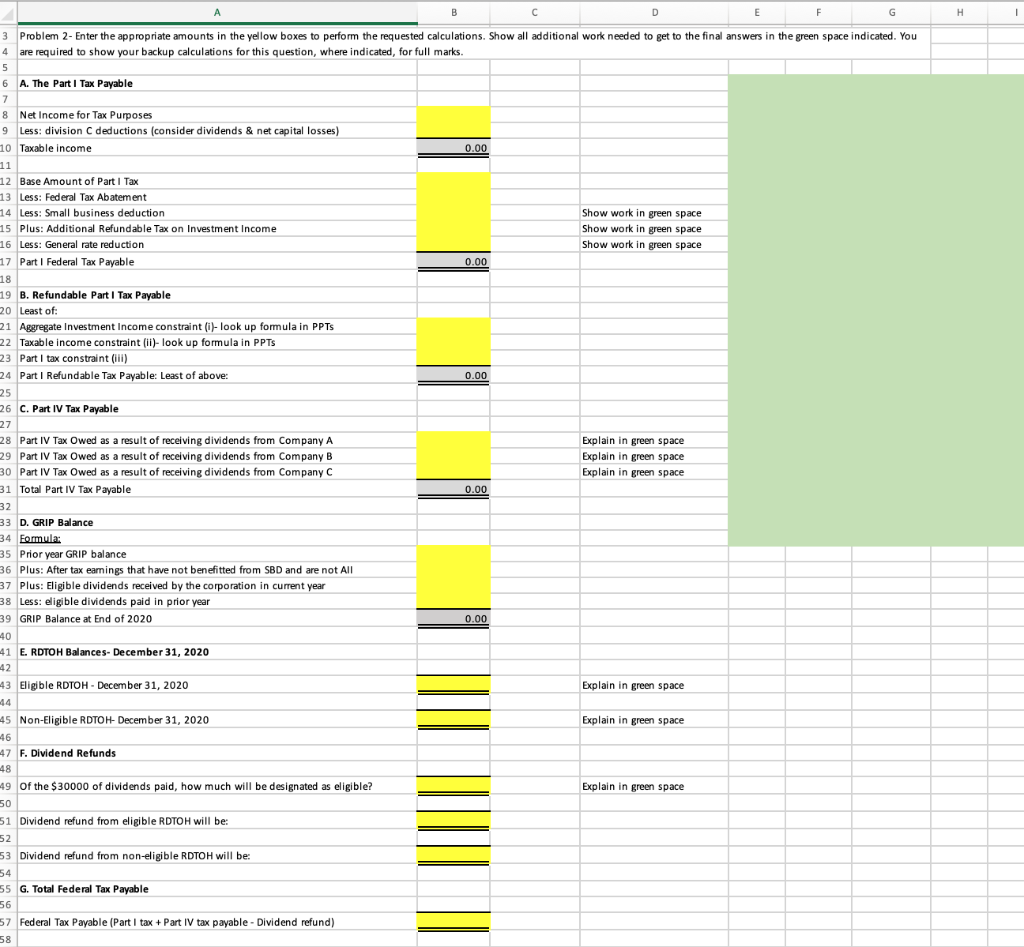

A B 2 Problem 2: Chapter 12 3 4 Instructions: 5 6 Dublin Ltd. is a CCPC involved in a retail business. Below is a breakdown of its Net Income for Tax Purposes for the December 7 31, 2020 tax year. 9 10 Active Business Income 210,000.00 11 Dividends: 12 Company A (All non-eligible) 95,000.00 13 Company B (All non-eligible) 17,000.00 14 Company C (All Eligible) 45,000.00 15 Rental Income 10,000.00 16 GIC Interest 17 Taxable Capital Gains 31,000.00 56,000.00 464,000.00 18 Net Income 19 20 On December 31, 2019, Dublin Ltd., has a GRIP balance of $54000 and a $0 balance in both the Non-Eligible RDTOH and the Eligible RDTOH. During 2019, Dublin Ltd. did not pay any dividends. Dublin Ltd. also has a net capital loss carryforward 21 balance of $80000. Dublin Ltd. hopes to deduct it in division C this year. 22 23 For 2019, the corporation's Adjusted Aggregate Investment Income was $25,000 and its Taxable Capital Employed in 24 Canada (TCEC) was $3 million. Last year's AAll and TCEC for Company A, B, and Dublin Ltd. combined was under $50,000 and 25 $10 million, respectively. 26 27 All dividends are from Canadian corporations and are deductible in Division C. The dividends paid to Dublin Ltd. by Company 28 A in 2020 did not entitle Company A to any dividend refund. The dividends paid by Company B in 2020 entitled Company B 29 to a dividend refund of $3000 from its non-eligible RDTOH. Dublin Ltd. owns 55% of the common/voting shares of Company A and 80% of the common/voting shares of Company B. In total, company A and B are allocated $225000 of the annual small 30 business deduction. The remainder is allocated to Dublin Ltd. 31 32 Dublin Ltd. owns 100 shares of Company C. Company C is a large public company with over 100,000,000 shares issued and 33 outstanding. Therefore, Dublin Ltd. does not own 10% of the total shares of Company C. 34 85 On November 17, 2020, Dublin Ltd. paid taxable dividends in the amount of $30000. Of these dividends paid, the corporation would like to designate the maximum amount of eligible dividends on which a dividend refund would be available. In this 36 case, this means ALL of the dividends paid this year will be designated as eligible. 37 88 Objective: Calculate the following required information for the 2020 year, including those for which the result is nil: 39 40 A. The Part I Tax Payable 41 B. The refundable portion of Part I Tax Payable 12 C. The Part IV Tax Payable 13 D. The balance in the GRIP account on December 31, 2020 14 E. The balance in the Eligible RDTOH and the Non-Eligible RDTOH accounts on December 31, 2020 (before any dividend refunds received as a result of divide 45 F. The amount of any dividend refunds resulting from the payment of eligible and non-eligible dividends (show calculation for 6 each). 47 G. Federal Tax Payable (net of any dividend refund). 18 19 50 Use the "P2-Response" tab to make your adjustments. Enter all your final adjustments in the yellow boxes beside each line 51 item. Show any notes/ extra work done for each line item in the green section of the "P2-Response" tab. 53 B E F 3 Problem 2- Enter the appropriate amounts in the yellow boxes to perform the requested calculations. Show all additional work needed to get to the final answers in the green space indicated. You 4 are required to show your backup calculations for this question, where indicated, for full marks. 5 6 A. The Part I Tax Payable 7 8 Net Income for Tax Purposes 9 Less: division C deductions (consider dividends & net capital losses) 0.00 10 Taxable income 11 12 Base Amount of Part I Tax 13 Less: Federal Tax Abatement 14 Less: Small business deduction 15 Plus: Additional Refundable Tax on Investment Income 16 Less: General rate reduction 17 Part I Federal Tax Payable 18 19 B. Refundable Part I Tax Payable 20 Least of: 21 Aggregate Investment Income constraint (i)-look up formula in PPTs 22 Taxable income constraint (ii)-look up formula in PPTs 23 Part I tax constraint (iii) 24 Part I Refundable Tax Payable: Least of above: 25 26 C. Part IV Tax Payable 27 Show work in green space Show work in green space Show work in green space 0.00 0.00 28 Part IV Tax Owed as a result of receiving dividends from Company A 29 Part IV Tax Owed as a result of receiving dividends from Company B 30 Part IV Tax Owed as a result of receiving dividends from Company C 31 Total Part IV Tax Payable 0.00 32 33 D. GRIP Balance 34 Formula: 35 Prior year GRIP balance 36 Plus: After tax eamings that have not benefitted from SBD and are not All 37 Plus: Eligible dividends received by the corporation in current year Explain in green space Explain in green space Explain in green space 38 Less: eligible dividends paid in prior year 39 GRIP Balance at End of 2020 40 41 E. RDTOH Balances- December 31, 2020 42 43 Eligible RDTOH December 31, 2020 44 45 Non-Eligible RDTOH- December 31, 2020 46 47 F. Dividend Refunds 48 49 Of the $30000 of dividends paid, how much will be designated as eligible? 50 51 Dividend refund from eligible RDTOH will be: 52 53 Dividend refund from non-eligible RDTOH will be: 54 55 G. Total Federal Tax Payable 56 57 Federal Tax Payable (Part I tax + Part IV tax payable - Dividend refund) 0.00 Explain in green space Explain in green space Explain in green space 58 H

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts