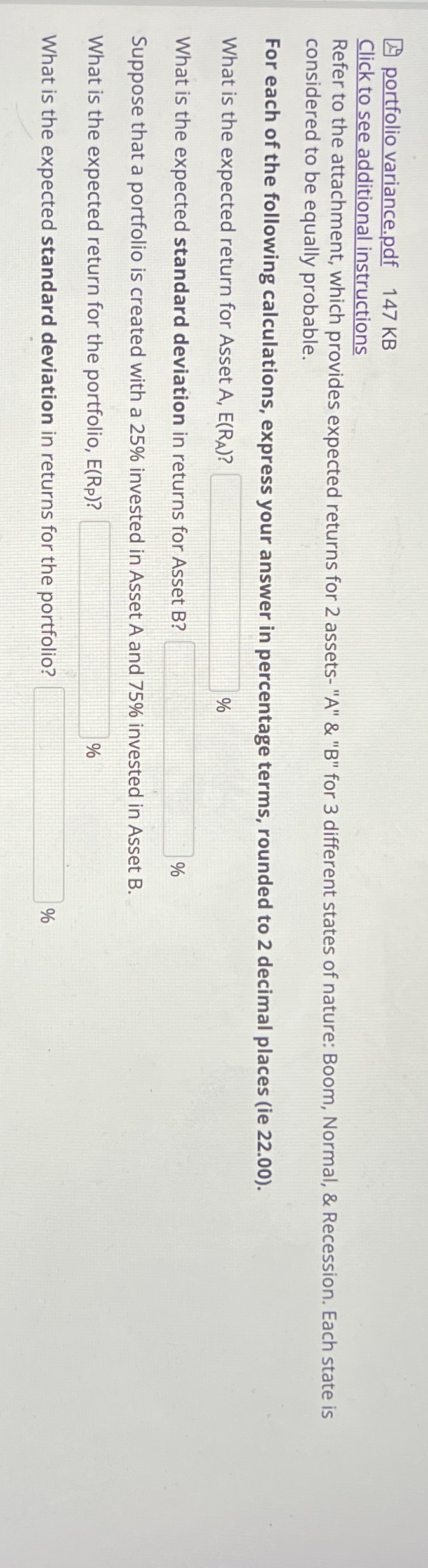

Question: A B Boom: 1 / 3 , 2 5 % , 1 % Normal: 1 / 3 , 5 % , 5 % Recessin: 1

A B

Boom:

Normal:

Recessin:

portfolio variance.pdf

Click to see additional instructions

Refer to the attachment, which provides expected returns for assetsA & B for different states of nature: Boom, Normal, & Recession. Each state is considered to be equally probable.

For each of the following calculations, express your answer in percentage terms, rounded to decimal places ie

What is the expected return for Asset

What is the expected standard deviation in returns for Asset B

Suppose that a portfolio is created with a invested in Asset A and invested in Asset B

What is the expected return for the portfolio,

What is the expected standard deviation in returns for the portfolio?

Refer to the attachment, which provides expected returns for assetsA & B for different states of nature: Boom, Normal, & Recession. Each state is considered to be equally probable.

For each of the following calculations, express your answer in percentage terms, rounded to decimal places ie

What is the expected return for Asset

What is the expected standard deviation in returns for Asset B

Suppose that a portfolio is created with a invested in Asset A and invested in Asset B

What is the expected return for the portfolio,

What is the expected standard deviation in returns for the portfolio?

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock