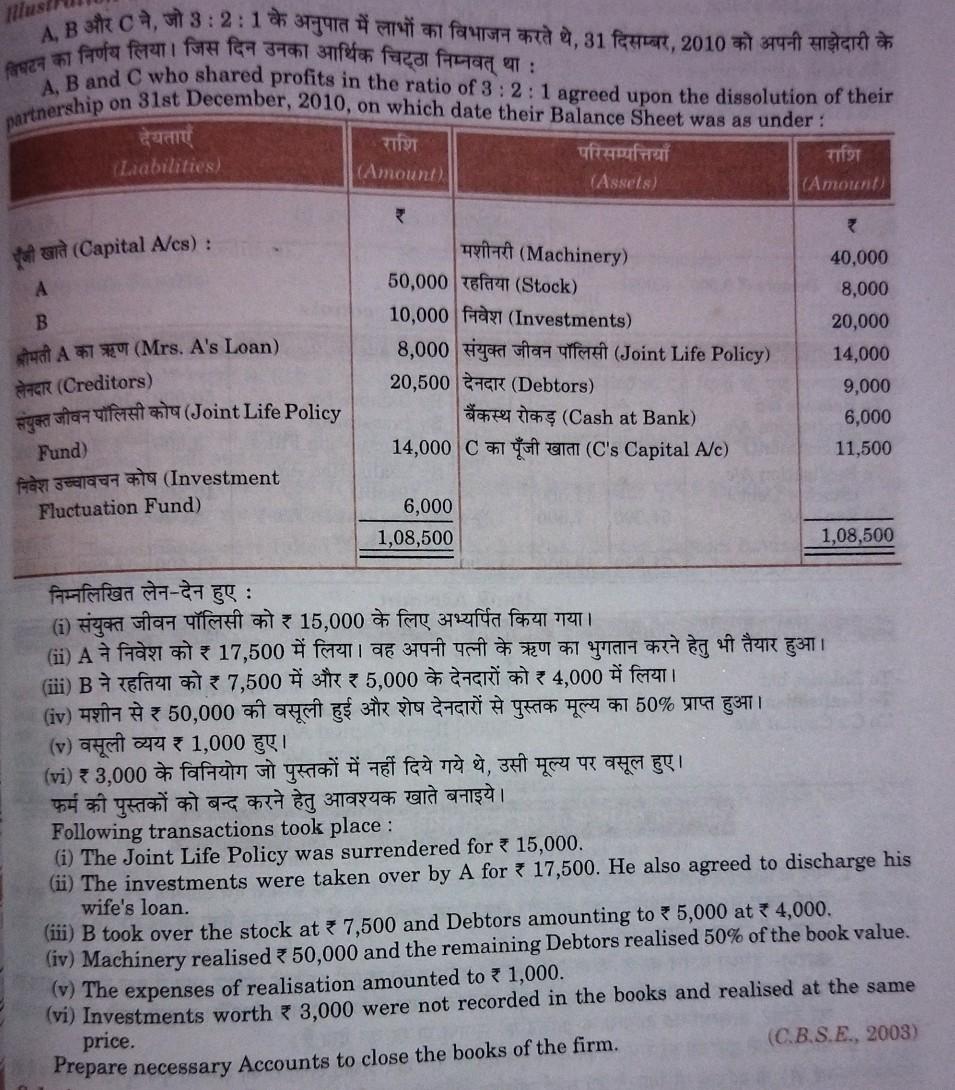

Question: A, B C , 3:2:1 , 31 , 2010 : A, B and C who shared profits in the ratio of 3: 2:1 agreed upon

A, B C , 3:2:1 , 31 , 2010 : A, B and C who shared profits in the ratio of 3: 2:1 agreed upon the dissolution of their on 31st December, 2010, on which date their Balance Sheet was as under: TLiabilities) (Amount) (Assets) (Amount partnership (Capital Acs) : A B (Machinery) 40,000 50,000 (Stock) 8,000 10,000 (Investments) 20,000 A (Mrs. A's Loan) 8,000 (Joint Life Policy) 14,000 (Creditors) 20,500 (Debtors) 9,000 (Joint Life Policy (Cash at Bank) 6,000 Fund) 14,000 C (C's Capital Ac) 11,500 (Investment Fluctuation Fund) 6,000 1,08,500 1,08,500 - : (1) 15,000 (ii) A 17,500 Cii) B 7,500 5,000 4,000 (iv) 50,000 50% (v) 1,000 (vi) 3,000 , Following transactions took place : (i) The Joint Life Policy was surrendered for 15,000. (ii) The investments were taken over by A for 17,500. He also agreed to discharge his wife's loan. (iii) B took over the stock at 7,500 and Debtors amounting to 5,000 at 4,000. (iv) Machinery realised 50,000 and the remaining Debtors realised 50% of the book value. (v) The expenses of realisation amounted to 1,000. (vi) Investments worth 3,000 were not recorded in the books and realised at the same price. (C.B.S.E., 2003) Prepare necessary Accounts to close the books of the firm

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts