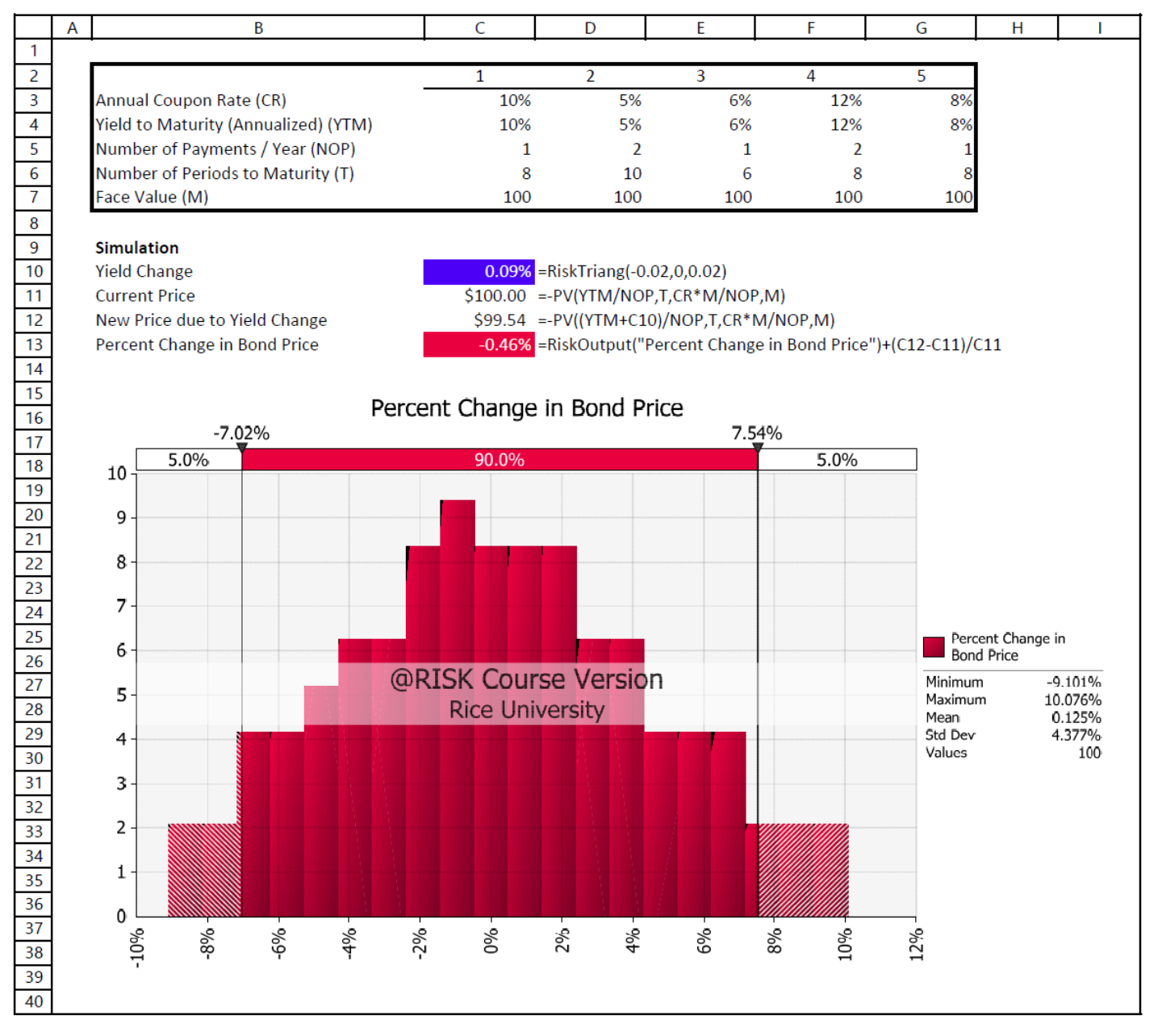

Question: A B C D E F G H 1 2 3 4 5 - W N Annual Coupon Rate (CR) 10% 5% 6% 12% 3%

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts