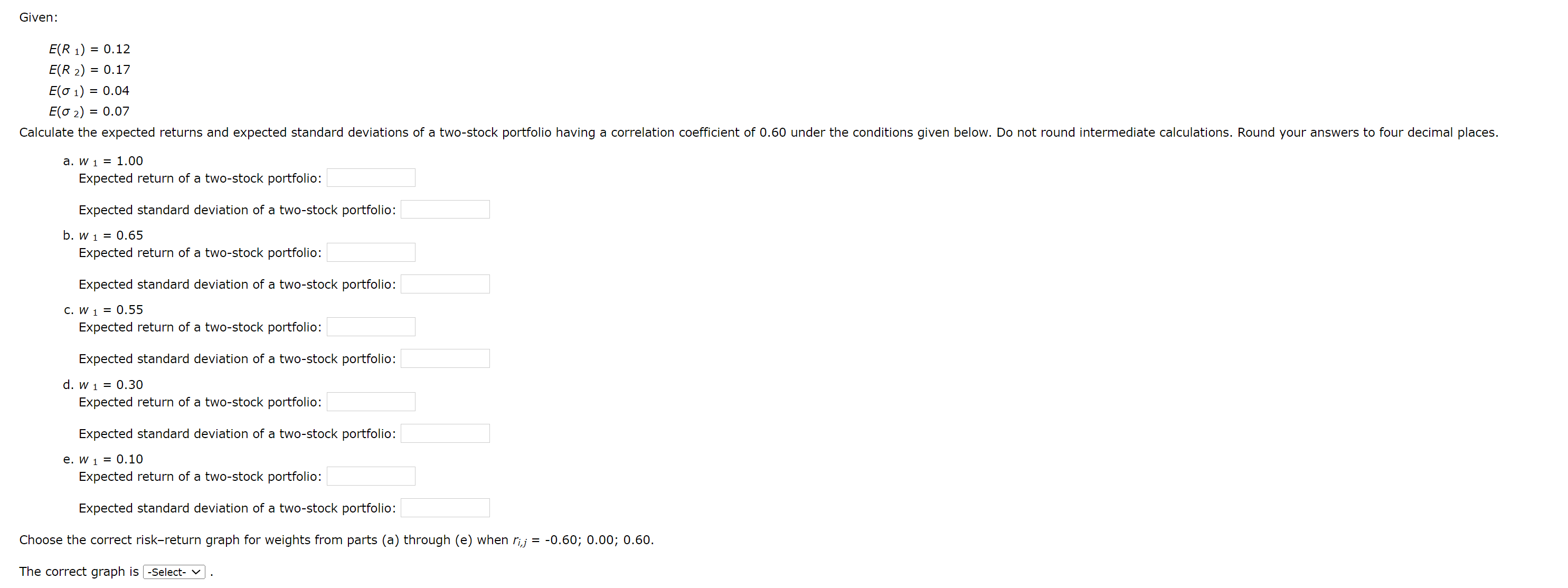

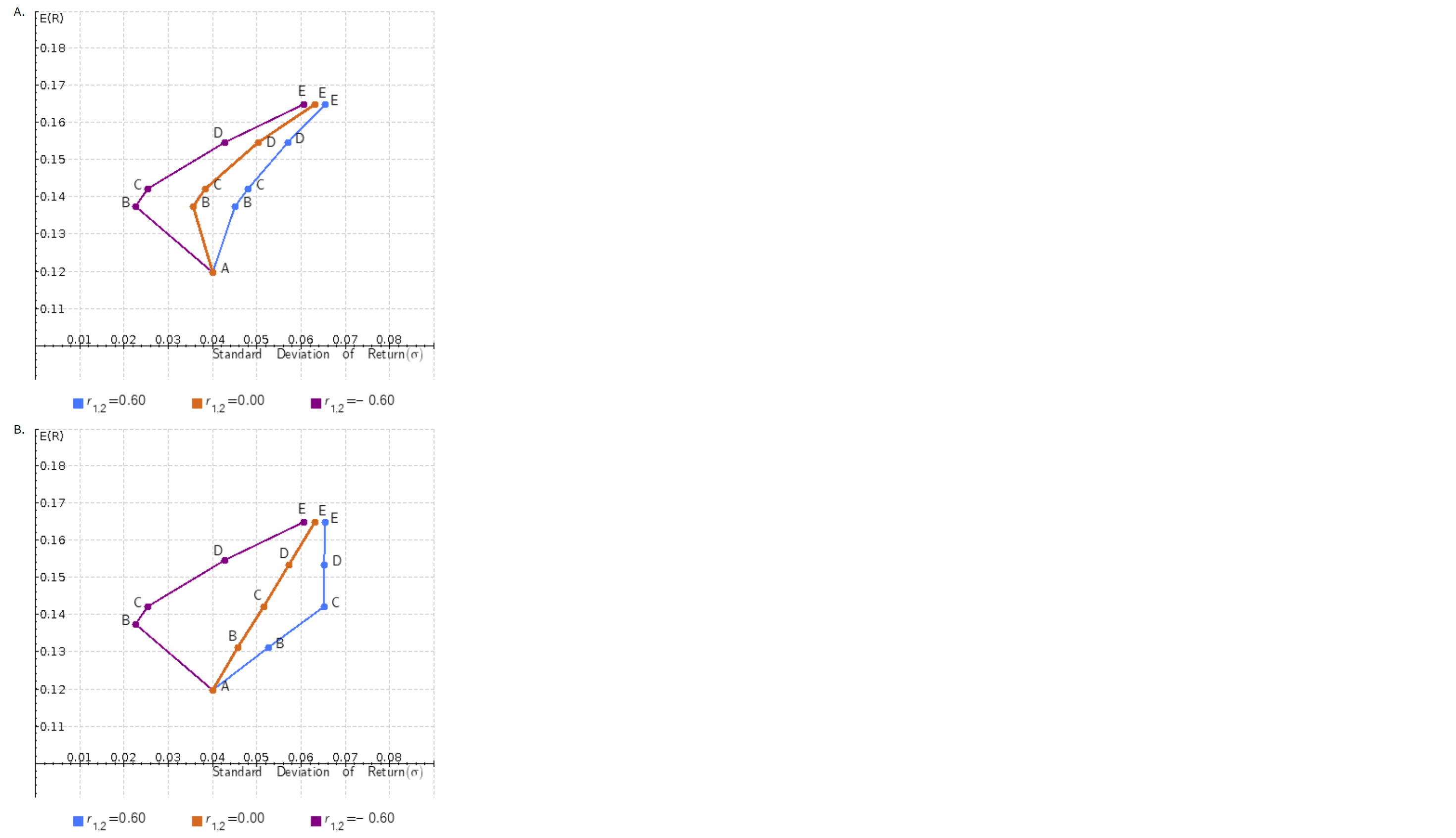

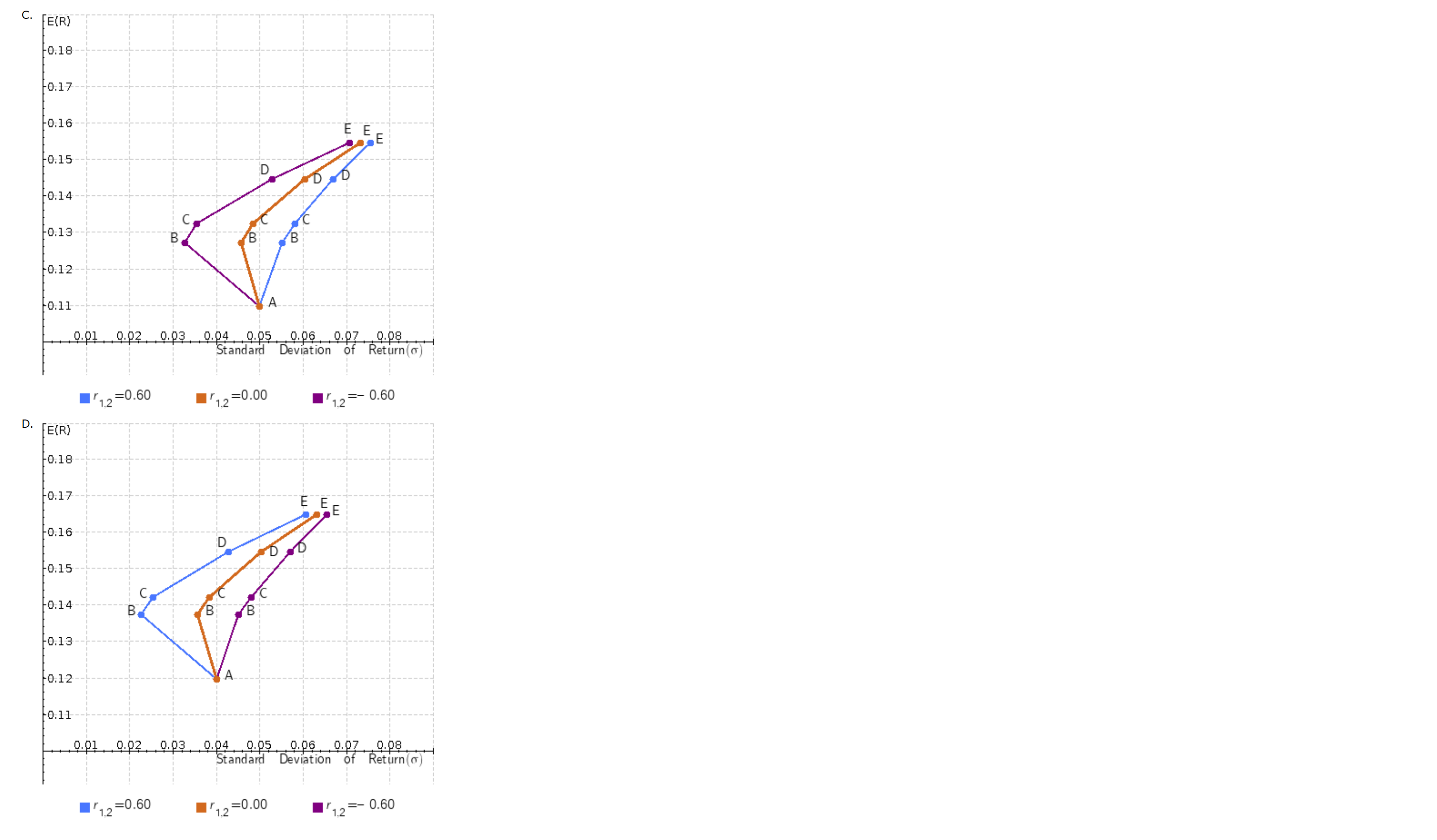

Question: A. B. C. D. E(R1)=0.12E(R2)=0.17E(1)=0.04E(2)=0.07 a. w1=1.00 Expected return of a two-stock portfolio: Expected standard deviation of a two-stock portfolio: b. w1=0.65 Expected return of

A. B. C. D. E(R1)=0.12E(R2)=0.17E(1)=0.04E(2)=0.07 a. w1=1.00 Expected return of a two-stock portfolio: Expected standard deviation of a two-stock portfolio: b. w1=0.65 Expected return of a two-stock portfolio: Expected standard deviation of a two-stock portfolio: c. w1=0.55 Expected return of a two-stock portfolio: Expected standard deviation of a two-stock portfolio: d. w1=0.30 Expected return of a two-stock portfolio: Expected standard deviation of a two-stock portfolio: e. w1=0.10 Expected return of a two-stock portfolio: Expected standard deviation of a two-stock portfolio: Choose the correct risk-return graph for weights from parts (a) through (e) when ri,j=0.60;0.00;0.60. The correct graph is

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts