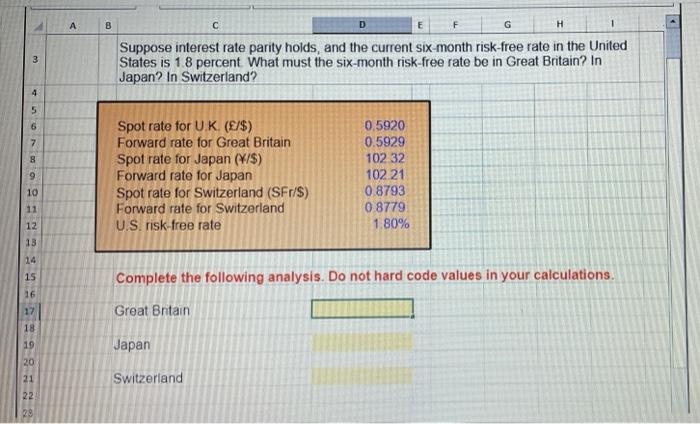

Question: A B D . E G H 1 3 3 Suppose interest rate parity holds, and the current six month risk-free rate in the United

A B D . E G H 1 3 3 Suppose interest rate parity holds, and the current six month risk-free rate in the United States is 18 percent What must the six-month risk-free rate be in Great Britain? In Japan? In Switzerland? 4 5 6 7 8 9 Spot rate for UK (/$) Forward rate for Great Britain Spot rate for Japan (/$) Forward rate for Japan Spot rate for Switzerland (SFr/S) Forward rate for Switzerland U.S. risk-free rate 0.5920 0.5929 102 32 102.21 08793 0.8779 1.80% 10 11 12 13 14 15 Complete the following analysis. Do not hard code values in your calculations. 16 Great Brtain 17 18 19 20 21 22 Japan Switzerland 29

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock