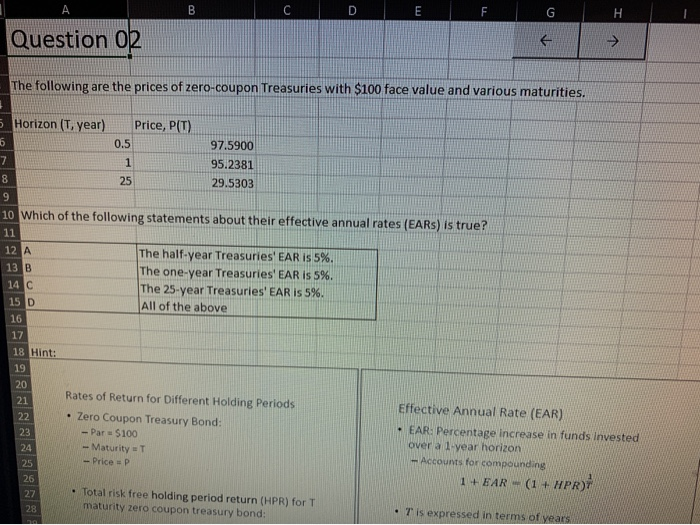

Question: A B D F G . Question 02 > The following are the prices of zero-coupon Treasuries with $100 face value and various maturities. 5

A B D F G . Question 02 > The following are the prices of zero-coupon Treasuries with $100 face value and various maturities. 5 Horizon (T, year) Price, P(T) 6 0.5 97.5900 7 1 95.2381 8 25 29.5303 9 10 Which of the following statements about their effective annual rates (EARs) is true? 11 12 A The half-year Treasuries' EAR is 5%. 13 B The one-year Treasuries' EAR is 5%. 14 C The 25-year Treasurles' EAR is 5%. 15 D All of the above 16 17 18 Hint: 19 20 21 Rates of Return for Different Holding Periods Effective Annual Rate (EAR) 22 Zero Coupon Treasury Bond: EAR: Percentage increase in funds invested 23 - Par $100 - Maturity = T over a 1-year horizon 25 - Price =P - Accounts for compounding 26 1 + EAR - (1 + #PR) 27 Total risk free holding period return (HPR) for T 28 maturity zero coupon treasury bond: T is expressed in terms of years 2A

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts