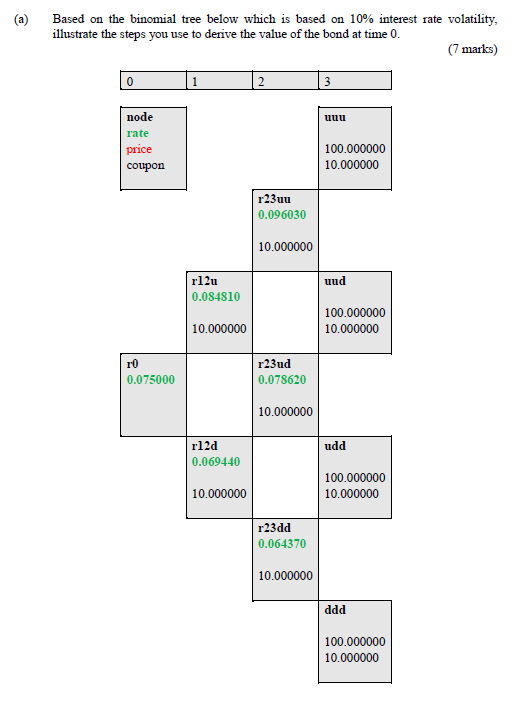

Question: (a) Based on the binomial tree below which is based on 10% interest rate volatility illustrate the steps you use to derive the value of

(a) Based on the binomial tree below which is based on 10% interest rate volatility illustrate the steps you use to derive the value of the bond at time 0 (7 marks) node rate price coupon 100.000000 10.000000 r23uu 0.096030 10.000000 uud 0.084810 100.000000 10.000000 10.000000 r0 0.075000 r23ud 0.078620 10.000000 rl2d 0.069440 udd 100.000000 10.000000 10.000000 r23dd 0.064370 10.000000 100.000000 10.000000 (a) Based on the binomial tree below which is based on 10% interest rate volatility illustrate the steps you use to derive the value of the bond at time 0 (7 marks) node rate price coupon 100.000000 10.000000 r23uu 0.096030 10.000000 uud 0.084810 100.000000 10.000000 10.000000 r0 0.075000 r23ud 0.078620 10.000000 rl2d 0.069440 udd 100.000000 10.000000 10.000000 r23dd 0.064370 10.000000 100.000000 10.000000

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts