A Battle Emerging in Mobile Payments By 2014, there were 6.6 billion mobile phone subscriptions in the

Question:

A Battle Emerging in Mobile Payments

By 2014, there were 6.6 billion mobile phone subscriptions in the world, and of those, 2.3 billion had active mobile broadband subscriptions that would enable users to access the mobile web. Mobile payment systems offered the potential of enabling all of these users to perform financial transactions on their phones, similar to how they would perform those transactions using personal computers. However, in 2015, there was no dominant mobile payment system, and a battle among competing mobile payment mechanisms and standards was unfolding.

In the United States, several large players, including Apple, Samsung, and a joint venture called Softcard between Google, AT&T, T-Mobile, and Verizon Wireless, had developed systems based on near field communication (NFC) chips in smartphones. NFC chips enable communication between a mobile device and a point-of-sale system just by having the devices in close proximity. The systems being developed by Apple, Samsung, and Softcard transferred the customer’s information wirelessly, and then used merchant banks and credit card systems such as Visa or MasterCard to complete the transaction. These systems were thus very much like existing ways of using credit cards, but enabled completion of the purchase without contact.

Other competitors such as Square (with Square Wallet) and PayPal did not require a smartphone with an NFC chip, but instead used a downloadable application and the Web to transmit a customer’s information. Square had gained early fame by offering small, free, credit card readers that could be plugged into the audio jack of a smartphone. These readers enabled vendors that would normally only take cash (for example, street vendors and babysitters) to accept major credit cards. Square processed $30 billion in payments in 2013, making the company one of the fastest-growing tech start-ups in Silicon Valley. Square takes about 2.75 to 3% from each transaction it processes, but must split that with credit card companies and other financial institutions. In terms of installed base, however, PayPal had the clear advantage, with over 161 million active registered accounts. With PayPal, customers could complete purchases simply by entering their phone numbers and a pin number, or use a PayPalissued magnetic stripe cards linked to their PayPal accounts. Users could opt to link their PayPal accounts to their credit cards, or directly to their bank accounts. PayPal also owned a service, Venmo, that enabled peer-to-peer exchanges with a Facebooklike interface that was growing in popularity as a way to exchange money without carrying cash. Venmo charged a 3% fee if the transaction used a major credit card, but was free if the consumer used it with a major bank card and debit card.

As noted above, some of the systems being developed did not require involvement of the major credit card companies, which potentially meant that billions of dollars in transaction fees might be avoided, or captured by a new player. PayPal, and its peer-to-peer system Venmo, for instance, did not require credit cards. A group of large merchants that included Wal- Mart, Old Navy, Best Buy, 7-Eleven, and more had also developed their own payment system –“Current- C”—a downloadable application for a smartphone that enabled purchases to be deducted directly from the customer’s bank accounts. This would enable merchants to avoid the 2-4% charges that they paid on credit card transactions, amounting to billions of dollars in savings for the participating merchants.

For consumers, the key dimensions that influenced adoption were convenience (would the customer have to type in a code at the point of purchase? was it easily accessible on a device the individual already owned?), risk of fraud (was the individual’s identity and financial information at risk?)n and ubiquity (could the system be used everywhere? did it enable peer-to-peer transactions?). For merchants, fraud was also a big concern, especially in situations where the transaction was not guaranteed by a third party, and cost (what were the fixed costs and transaction fees of using the system?) Apple Pay had a significant convenience advantage in that a customer could pay via their fingerprint. Current-C, by contrast, had a serious convenience disadvantage because consumers would have to open the application on their phone and get a QR code to be scanned at the checkout aisle. Both Apple Pay and Current- C also experienced fraud problems, with multiple reports of hacked accounts emerging by early 2015.

In the United States, almost half of all consumers had used their smartphones to make a payment at a merchant location by early 2015. Mobile payments accounted for $52 billion in transactions in 2014 and were expected to be $67 billion in 2015.

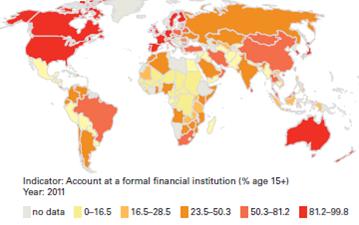

In other parts of the world, intriguing alternatives for mobile banking were gaining traction even faster. In India and Africa, for example, there are enormous populations of “unbanked” or “underbanked” people (individuals who do not have bank accounts or make limited use of banking services). In these regions, the proportion of people with mobile phones vastly exceeds the proportion of those with credit cards. In Africa, for example, less than 3% of the population was estimated to have a credit card, whereas 69% of the population was estimated to have mobile phones. Notably, the maximum fixed-line phone penetration ever achieved in Africa was 1.6%—reached in 2009–demonstrating the power of mobile technology to “leapfrog” landbased technology in the developing world. The opportunity, then, of giving such people access to fast and inexpensive funds transfer is enormous.

The leading system in India is the Inter-bank Mobile Payment Service developed by National Payments Corporation of India (NPCI). NPCI leveraged its ATM network (connecting more than 65 large banks in India) to create a person-to-person mobile banking system that works on mobile phones. The system uses a unique identifier for each individual who links directly to a bank account. In parts of Africa, where the proportion of people who are unbanked is even larger, a system called M-Pesa (“M” for mobile and “pesa,” which is Kiswahili for money) enables any individual with a passport or national ID card to deposit money into his or her phone account and transfer money to other users using short message service (SMS). By 2015, the M-Pesa system had roughly 12.2 million active users. The system enabled the percent of Kenyans with access to banking to rise from 41% in 2009 to 67% in 2014.

By early 2015, it was clear that mobile payments represented a game-changing opportunity that could accelerate e-commerce, smartphone adoption, and the global reach of financial services. However, lack of compatibility between many of the mobile payment systems, and uncertainty over what type of mobile payment system will become dominant, still pose significant obstacles to consumer and merchant adoption.

What are the advantages and disadvantages of using mobile banking systems for individuals and businesses?

Expert Answer:

1 Advantages of mobile Payment systems in a developed economy is the potential saving on cost and ti... View the full answer

Income Tax Fundamentals 2013

ISBN: 9781285586618

31st Edition

Authors: Gerald E. Whittenburg, Martha Altus Buller, Steven L Gill