Question: A CDO invests in two $1000 zero-coupon bonds. The CDO has two tranches, the Senior tranche gets paid $1000 before the Junior Tranche gets

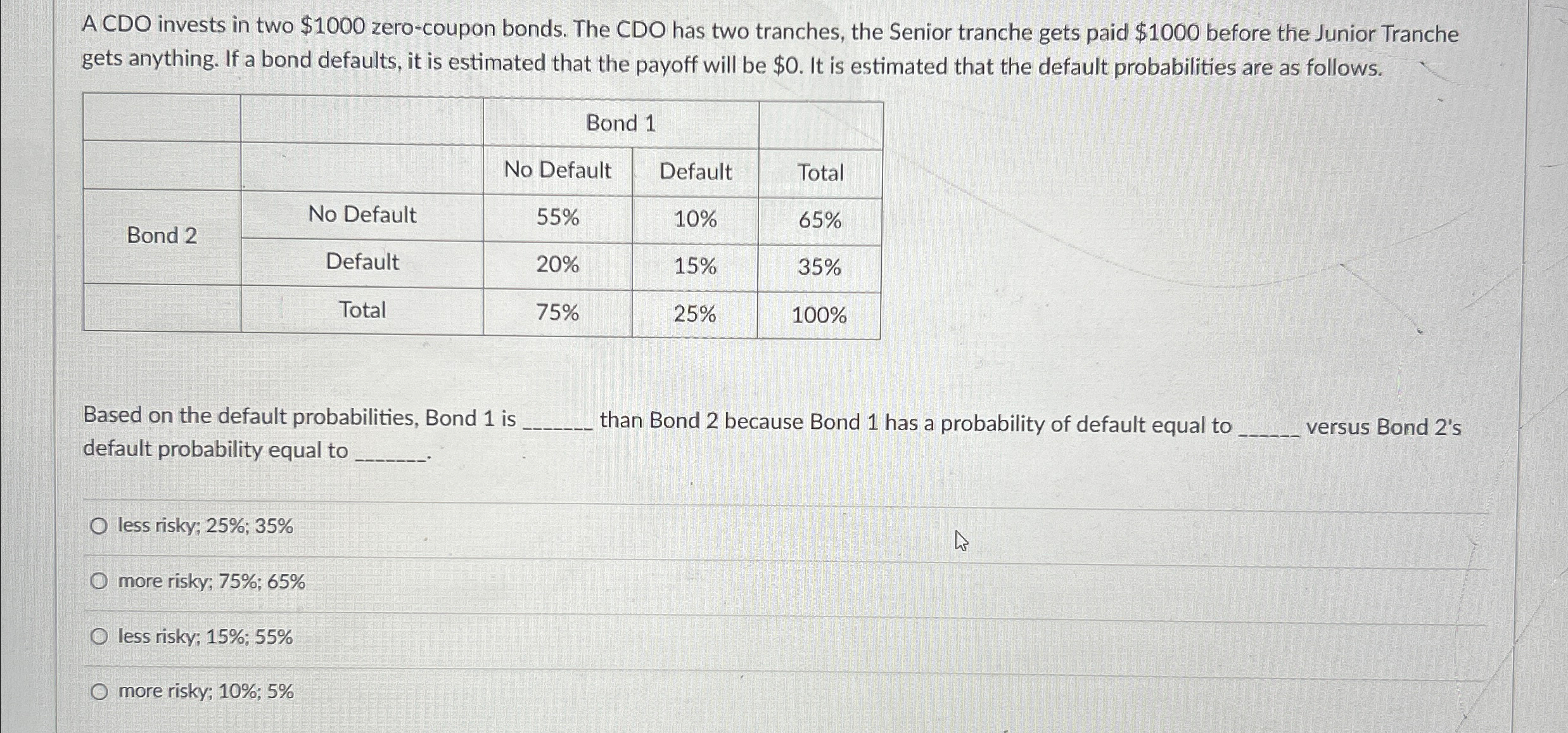

A CDO invests in two $1000 zero-coupon bonds. The CDO has two tranches, the Senior tranche gets paid $1000 before the Junior Tranche gets anything. If a bond defaults, it is estimated that the payoff will be $0. It is estimated that the default probabilities are as follows. Bond 1 No Default Default Total No Default 55% 10% 65% Bond 2 Default 20% 15% 35% Total 75% 25% 100% Based on the default probabilities, Bond 1 is default probability equal to O less risky; 25%; 35% O more risky; 75%; 65% Oless risky; 15%; 55% O more risky; 10%; 5% than Bond 2 because Bond 1 has a probability of default equal to versus Bond 2's B

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts