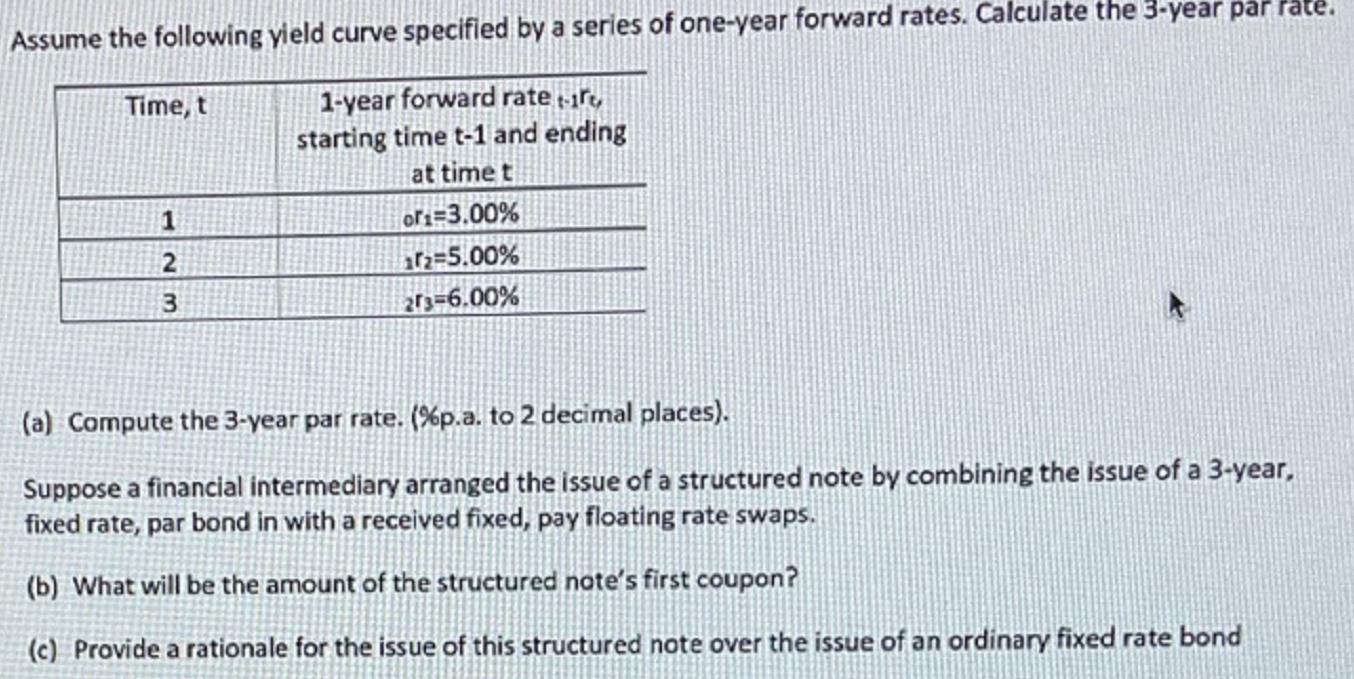

Question: (a) Compute the 3-year par rate. (%p.a. to 2 decimal places). Suppose a financial intermediary arranged the issue of a structured note by combining the

(a) Compute the 3-year par rate. (\%p.a. to 2 decimal places). Suppose a financial intermediary arranged the issue of a structured note by combining the issue of a 3-year, fixed rate, par bond in with a received fixed, pay floating rate swaps. (b) What will be the amount of the structured note's first coupon? (c) Provide a rationale for the issue of this structured note over the issue of an ordinary fixed rate bond (a) Compute the 3-year par rate. (\%p.a. to 2 decimal places). Suppose a financial intermediary arranged the issue of a structured note by combining the issue of a 3-year, fixed rate, par bond in with a received fixed, pay floating rate swaps. (b) What will be the amount of the structured note's first coupon? (c) Provide a rationale for the issue of this structured note over the issue of an ordinary fixed rate bond

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts