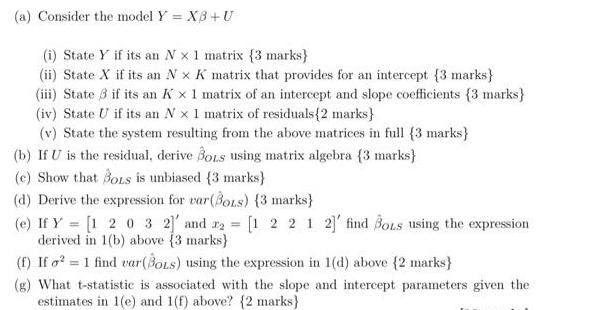

Question: (a) Consider the model Y = X3+U (i) State Y if its an Nx 1 matrix (3 marks) (ii) State X if its an

(a) Consider the model Y = X3+U (i) State Y if its an Nx 1 matrix (3 marks) (ii) State X if its an Nx K matrix that provides for an intercept {3 marks) (iii) State 3 if its an K x 1 matrix of an intercept and slope coefficients [3 marks} (iv) State U if its an N x 1 matrix of residuals (2 marks] (v) State the system resulting from the above matrices in full (3 marks) (b) If U is the residual, derive BoLs using matrix algebra (3 marks} (e) Show that BoLs is unbiased (3 marks) (d) Derive the expression for var(BOLS) (3 marks} (e) If Y = [1 2 0 3 2] and r2 = [1 2 2 1 2]' find BoLs using the expression derived in 1(b) above (3 marks) (f) If o = 1 find var (BOLS) using the expression in 1(d) above (2 marks] (g) What t-statistic is associated with the slope and intercept parameters given the estimates in 1(e) and 1(f) above? {2 marks)

Step by Step Solution

3.51 Rating (161 Votes )

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts