Question: a. For the exponential smoothing method, choose the first quarter of 3 years ago as the beginning forecast. Make two forecasts: one with a =

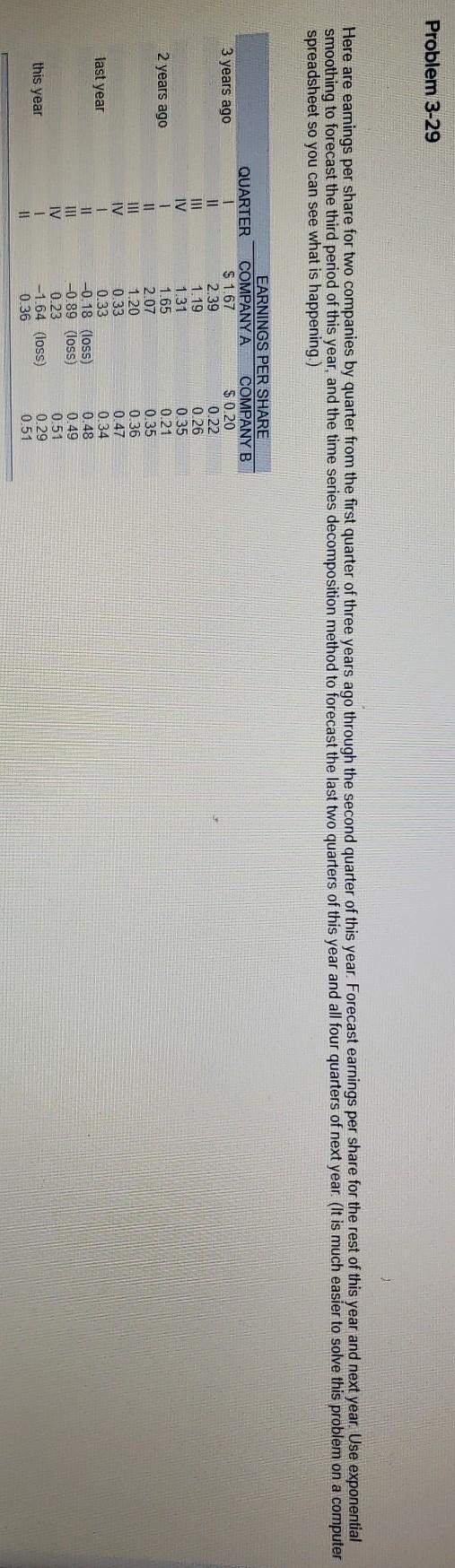

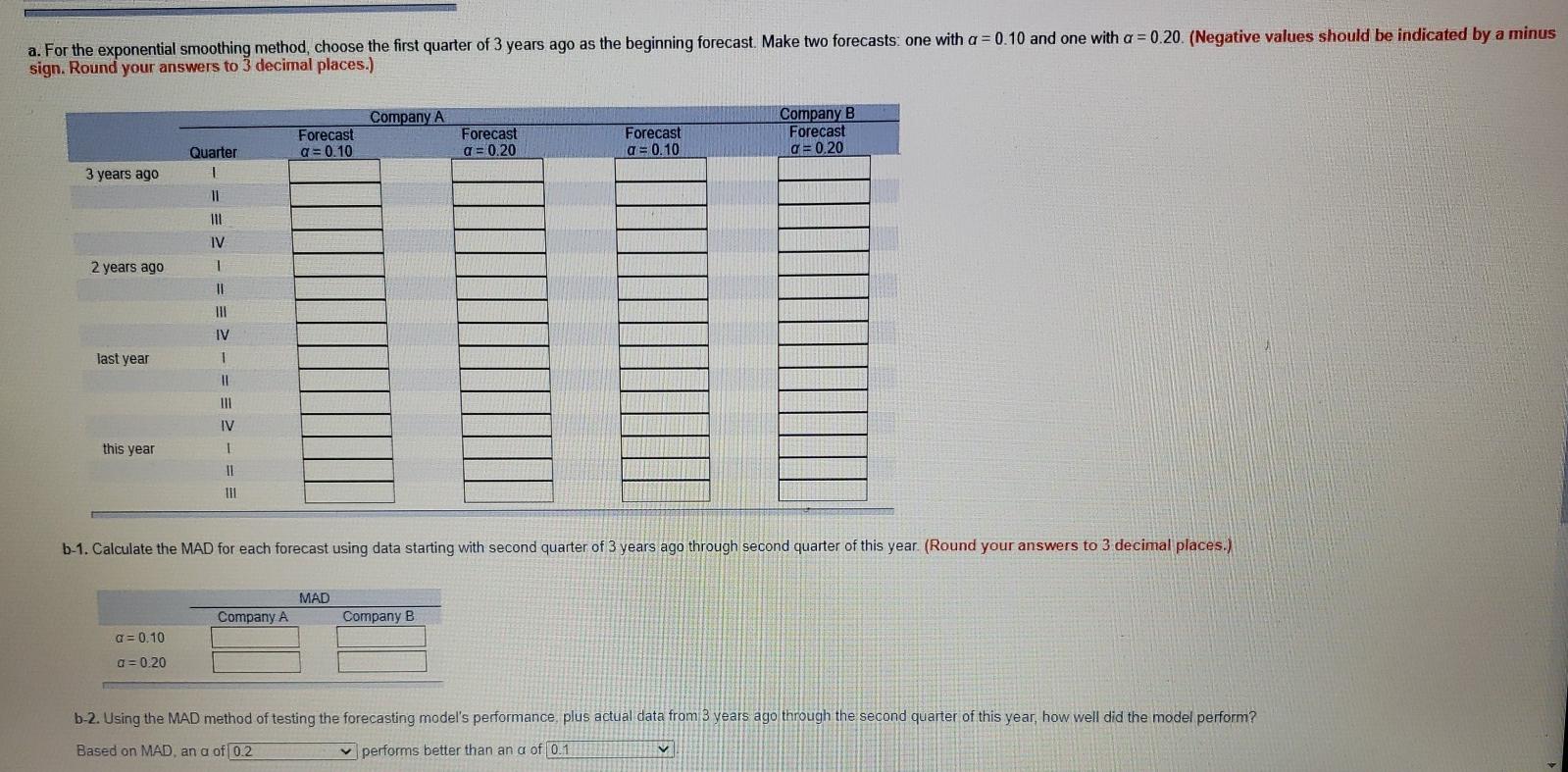

a. For the exponential smoothing method, choose the first quarter of 3 years ago as the beginning forecast. Make two forecasts: one with a = 0.10 and one with a = 0.20 (Negative values should be indicated by a minus sign. Round your answers to 3 decimal places.) Company A Forecast a = 0.10 Forecast a = 0.20 Forecast a = 0.10 Company B Forecast a=0.20 3 years ago Quarter 1 11 III IV 2 years ago 1 11 III IV last year 1 II IV this year 1 II 111 b-1. Calculate the MAD for each forecast using data starting with second quarter of 3 years ago through second quarter of this year. (Round your answers to 3 decimal places.) MAD Company A Company B a=0.10 a=0.20 b-2. Using the MAD method of testing the forecasting model's performance, plus actual data from 3 years ago through the second quarter of this year, how well did the model perform? Based on MAD, an a of 0.2 performs better than an a of 0.1 v c. Using the decomposition of a time series method of forecasting, forecast earnings per share for the last two quarters of this year and all four quarters of next year. (Negative values should be indicated by a minus Round your answers to 3 decimal places.) Company A Seasonal Factor Quarter Forecast Company B Seasonal Factor Forecast this year IV next year 1 11 III IV

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock