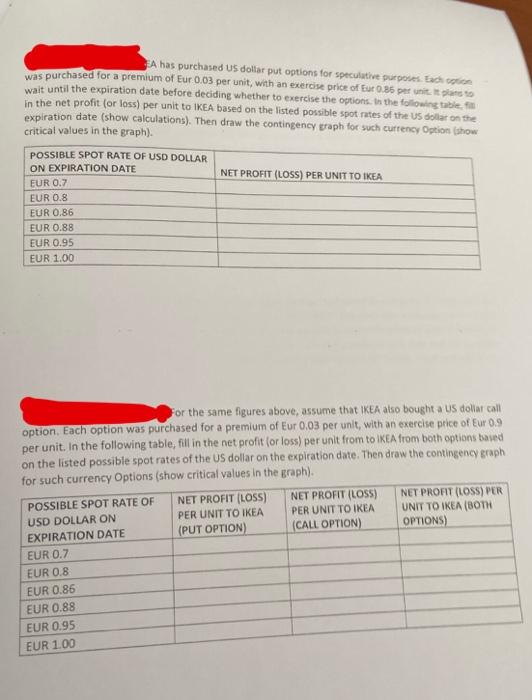

Question: A has purchased US dollar put options for speculative purposes. Each option was purchased for a premium of Eur 0.03 per unit, with an

A has purchased US dollar put options for speculative purposes. Each option was purchased for a premium of Eur 0.03 per unit, with an exercise price of Eur 0.86 per unit. It plans to wait until the expiration date before deciding whether to exercise the options. In the following table, fill in the net profit (or loss) per unit to IKEA based on the listed possible spot rates of the US dollar on the expiration date (show calculations). Then draw the contingency graph for such currency Option (show critical values in the graph). POSSIBLE SPOT RATE OF USD DOLLAR ON EXPIRATION DATE EUR 0.7 EUR 0.8 NET PROFIT (LOSS) PER UNIT TO IKEA EUR 0.86 EUR 0.88 EUR 0.95 EUR 1.00 For the same figures above, assume that IKEA also bought a US dollar call option. Each option was purchased for a premium of Eur 0.03 per unit, with an exercise price of Eur 0.9 per unit. In the following table, fill in the net profit (or loss) per unit from to IKEA from both options based on the listed possible spot rates of the US dollar on the expiration date. Then draw the contingency graph for such currency Options (show critical values in the graph). POSSIBLE SPOT RATE OF EXPIRATION DATE USD DOLLAR ON EUR 0.7 EUR 0.8 EUR 0.86 EUR 0.88 NET PROFIT (LOSS) PER UNIT TO IKEA (PUT OPTION) NET PROFIT (LOSS) PER UNIT TO IKEA (CALL OPTION) NET PROFIT (LOSS) PER UNIT TO IKEA (BOTH OPTIONS) EUR 0.95 EUR 1.00

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts