Question: A Heading 1 Heading 3 I Normal Editing Dictate Sensitivity Edito v I AL Paragraph 15 Styles 12 Voice Sensitivity Editor Exhibit Table 1 A

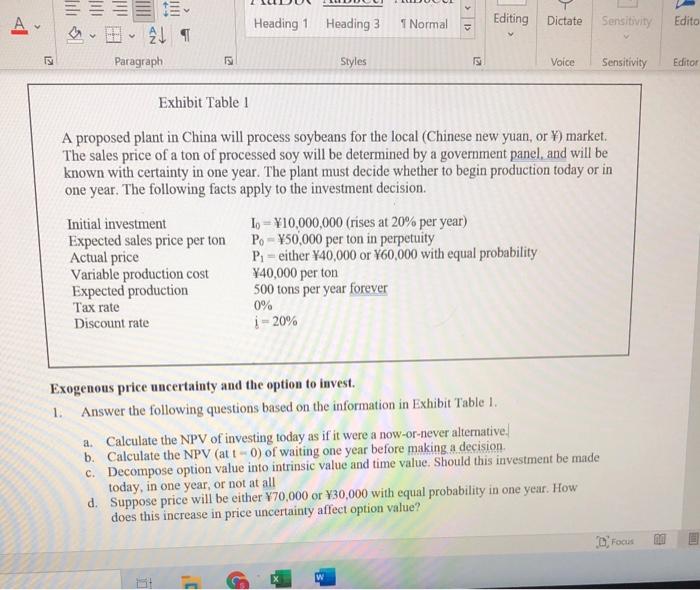

A Heading 1 Heading 3 I Normal Editing Dictate Sensitivity Edito v I AL Paragraph 15 Styles 12 Voice Sensitivity Editor Exhibit Table 1 A proposed plant in China will process soybeans for the local (Chinese new yuan, or Y) market. The sales price of a ton of processed soy will be determined by a government panel, and will be known with certainty in one year. The plant must decide whether to begin production today or in one year. The following facts apply to the investment decision. Initial investment Io =10,000,000 (rises at 20% per year) Expected sales price per ton Po - 50,000 per ton in perpetuity Actual price P. - either Y40,000 or V60,000 with equal probability Variable production cost Y40,000 per ton Expected production 500 tons per year forever Tax rate Discount rate i -20% 0% Exogenous price uncertainty and the option to invest. 1. Answer the following questions based on the information in Exhibit Table 1. a. Calculate the NPV of investing today as if it were a now-or-never alternative. b. Calculate the NPV (att -0) of waiting one year before making a decision c. Decompose option value into intrinsic value and time value. Should this investment be made today, in one year, or not at all d. Suppose price will be either 470,000 or $30,000 with equal probability in one year. How does this increase in price uncertainty affect option value? D) Focus 1

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts