Question: A hedge fund has created a portfolio using just two stocks. It has shorted $45,000,000 worth of Oracle stock and has purchased $75,000,000 of Intel

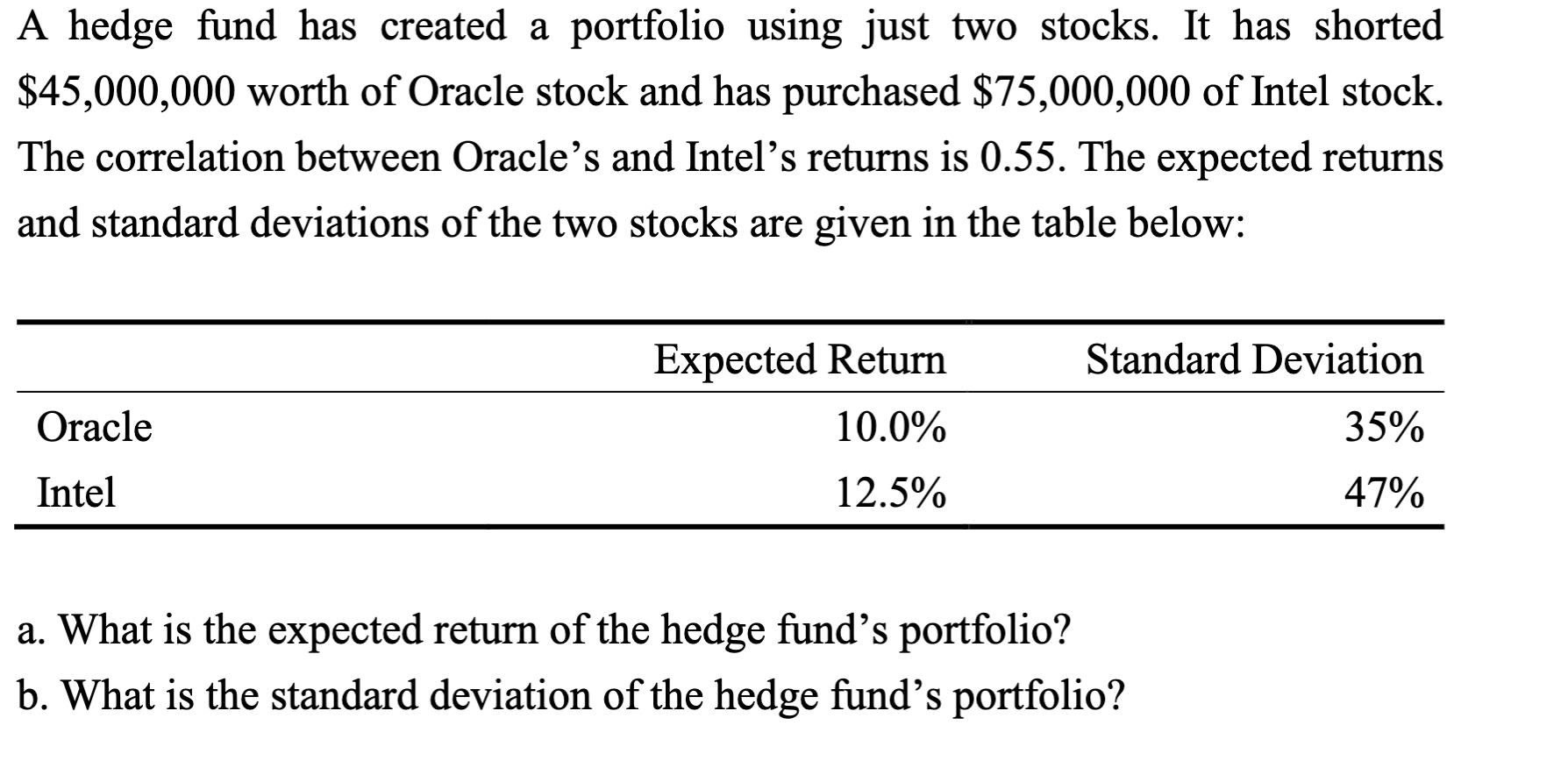

A hedge fund has created a portfolio using just two stocks. It has shorted $45,000,000 worth of Oracle stock and has purchased $75,000,000 of Intel stock. The correlation between Oracle's and Intel's returns is 0.55. The expected returns and standard deviations of the two stocks are given in the table below: Expected Return Standard Deviation 10.0% 35% Oracle Intel 12.5% 47% a. What is the expected return of the hedge fund's portfolio? b. What is the standard deviation of the hedge fund's portfolio

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock