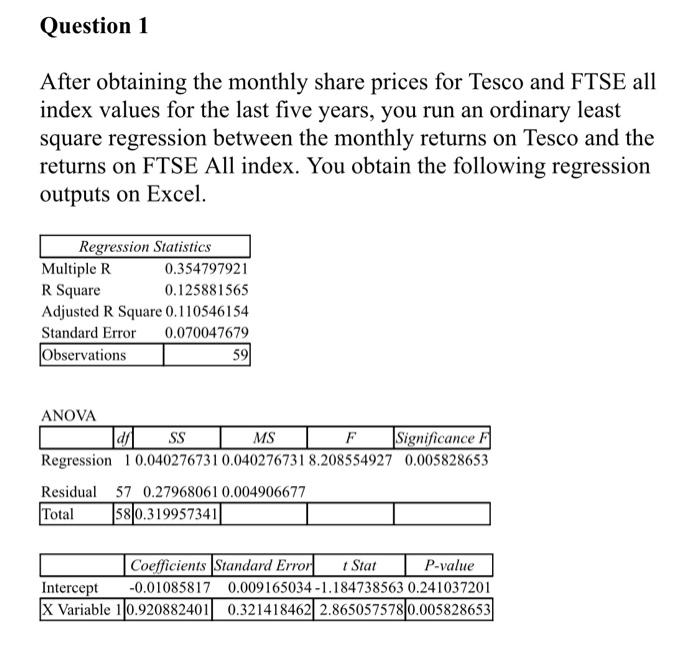

Question: (a) ( i ) What is the estimated beta value for Tesco from the above regression outputs? Question 1 After obtaining the monthly share prices

Question 1 After obtaining the monthly share prices for Tesco and FTSE all index values for the last five years, you run an ordinary least square regression between the monthly returns on Tesco and the returns on FTSE All index. You obtain the following regression outputs on Excel. Regression Statistics Multiple R 0.354797921 R Square 0.125881565 Adjusted R Square 0.110546154 Standard Error 0.070047679 Observations 590 ANOVA dll SS MS F Significance F Regression 10.040276731 0.040276731 8.208554927 0.005828653 Residual 57 0.27968061 0.004906677 Total 580.3199573411 Coefficients Standard Error 1 Stat P-value Intercept -0.01085817 0.009165034 -1.184738563 0.241037201 X Variable 10.920882401 0.321418462 2.865057578|0.005828653

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts