Question: (a) Implement the right endpoint rule as a function in R. Use it to compute L /2 22 dz for several discretizations h. Compare

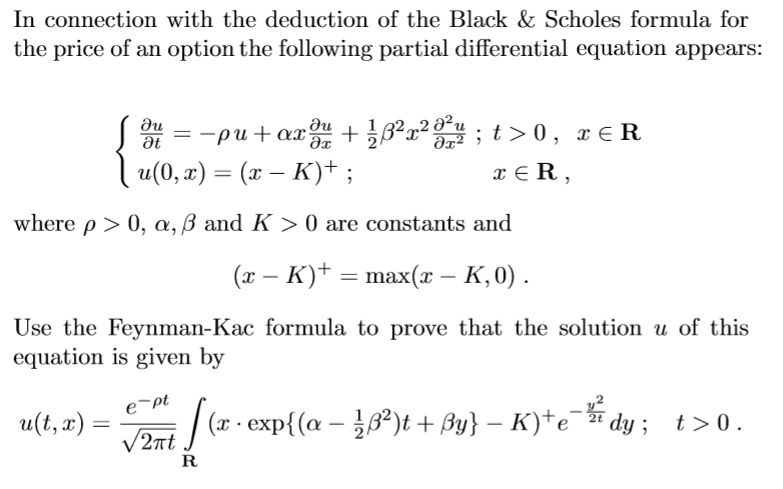

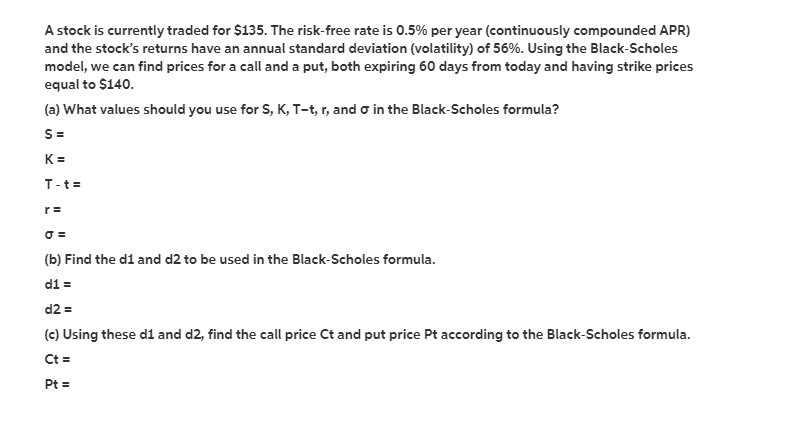

(a) Implement the right endpoint rule as a function in R. Use it to compute L /2 22 dz for several discretizations h. Compare your results to the exact answer and verify the order of convergence of the right endpoint method. (b) How might you use a numerical integrator to compute the integral L 212 dz? Implement a function that takes as input a and the number of subintervals n and numerically approximates the integral using a scheme of your choice. (c) The Black-Scholes formula for a European call option is: C()=Se(d+) - Ke*(-)(d) where (2)= 2T d+ log () + (r-q+) (Tt) oT-t dd-oT-1 = log () + (rq) (T-1) +(8-9-) Using your results from (b), write a function in R. that takes as input S, T, t, K, r, 8, and q and outputs the Black-Scholes call option price with all integrals computed numerically. (d) Use one of your finite difference schemes to approximate one of the Greeks using the function from (c) to compute the data points. Compare this to the exact answer, and comment on how the numerical integration affected your accuracy. In connection with the deduction of the Black & Scholes formula for the price of an option the following partial differential equation appears: u t =-pu+ax +x; t> 0, x R Ju | u(0, x) = (x K) + ; - 20u 12 x R, where p > 0, a, and K > 0 are constants and - (x K)+ = max(x K,0). - Use the Feynman-Kac formula to prove that the solution u of this equation is given by u(t, x) = e-pt (2t - 1 (x exp{(a } )t + y} K)+edy ; R t>0. A stock is currently traded for $135. The risk-free rate is 0.5% per year (continuously compounded APR) and the stock's returns have an annual standard deviation (volatility) of 56%. Using the Black-Scholes model, we can find prices for a call and a put, both expiring 60 days from today and having strike prices equal to $140. (a) What values should you use for S, K, T-t, r, and in the Black-Scholes formula? S = K = T-t= r = = (b) Find the d1 and d2 to be used in the Black-Scholes formula. d1 = d2 = (c) Using these d1 and d2, find the call price Ct and put price Pt according to the Black-Scholes formula. Ct = Pt=

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts