Question: a) Let the claim number random variable, namely N, be Poisson dis- tributed with parameter ? > 0. Also, let the individual losses, X, have

a) Let the claim number random variable, namely N, be Poisson dis- tributed with parameter ? > 0. Also, let the individual losses, X, have probability function fX(1) = 0.8 and fX(2) = 0.2. The claim sizes {Xi}i?1 are independent each other and independent of the random variable N.

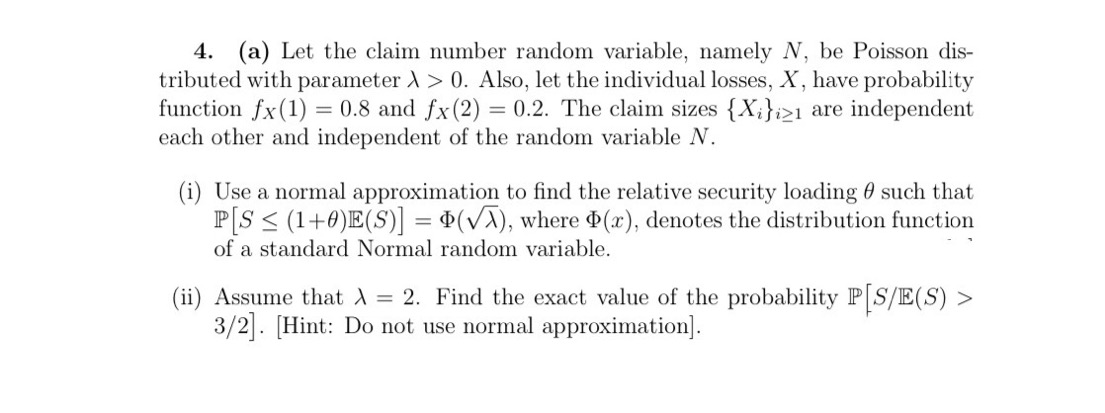

4. (a) Let the claim number random variable, namely N, be Poisson dis- tributed with parameter > > 0. Also, let the individual losses, X, have probability function fx(1) = 0.8 and fx(2) = 0.2. The claim sizes {Xi}> are independent each other and independent of the random variable N. (i) Use a normal approximation to find the relative security loading 0 such that PIS S (1+0)E(S)] = $(VA), where (x), denotes the distribution function of a standard Normal random variable. (ii) Assume that A = 2. Find the exact value of the probability P S/E(S) > 3/2 . [Hint: Do not use normal approximation]

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts