A Ltd is a Singapore-incorporated company and its functional and presentation currency is Singapore Dollar ($). It

Question:

A Ltd is a Singapore-incorporated company and its functional and presentation currency is Singapore Dollar ($). It adopts Singapore Financial Reporting Standards and presents yearly financial statements with 31 December year-end.

B Bhd is a Malaysia-incorporated company and its functional and presentation currency is Ringgit Malaysia (RM). It adopts Malaysia Financial Reporting Standards and presents yearly financial statements with 31 December year-end.

On 1 January 20x8, A Ltd paid $175,000 to acquire a 100% controlling interest in B Bhd, when the fair value of B Bhd's identifiable net assets was represented by share capital of RM100,000 and retained profit of RM100,000, except for its freehold land, which was carried at cost of RM500,000 but had a market value of RM600,000.

On 1 October 20x8, A Ltd extended an interest-free loan of RM100,000 to B Bhd, for which repayment was not scheduled for. This loan has been properly accounted for as "part of a reporting entity's net investment in a foreign operation" in the respective financial statements of A Ltd and B Bhd.

Profit on sale of land in Malaysia is subject to real property gains tax at a rate of 10%. Except for the Malaysian real property gains tax, ignore deferred tax effects arising from consolidation as they are expected to be immaterial.

The exchange rates were RM1.00 = $0.50 on 1 January 20x8, RM1.00 = $0.38 on 1 October 20x8, and RM1.00 = $0.30 on 31 December 20x8. The average exchange rate for the year 20x8 was RM1.00 = $0.40. The exchange rates when B Bhd was incorporated with the issuance of 100,000 ordinary shares at RM1.00 each in 20x1 and when B Bhd bought the land in 20x2 were RM1.00 = $0.80 and RM1.00 = $0.70 respectively.

All the relevant Singapore Financial Reporting Standards that were issued by the Accounting Standards Council as at 1 January 2021 are assumed to have been effective on 1 January 20x8. There are no significant differences between the Malaysian Financial Reporting Standards and the Singapore Financial Reporting Standards.

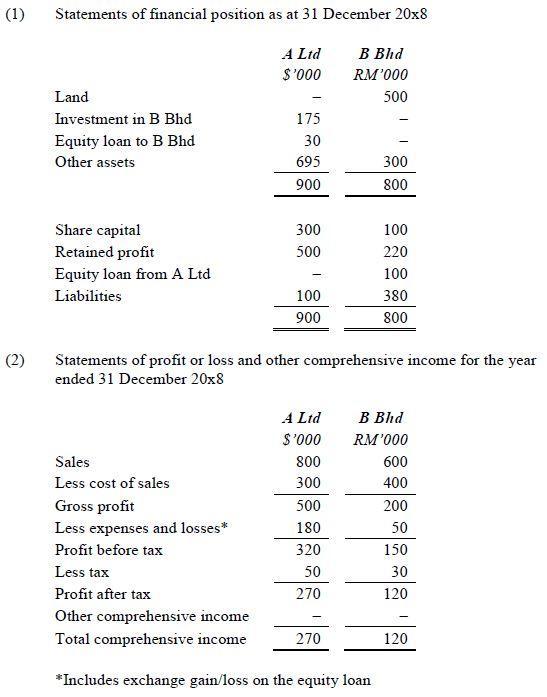

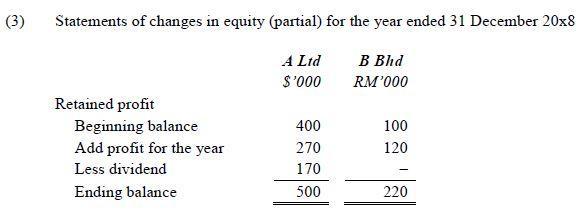

The 20x8 financial statements of A Ltd and B Bhd are as follows:

Required:

Translate B Bhd’s statement of financial position and statement of profit and loss and other comprehensive income into Singapore Dollars ($) for the purposes of the 20x8 consolidation of A Ltd group. Show the calculation for translation gain/loss.

Expert Answer:

On first October 20x8 A Ltd gave B Bhd a loan that was intrest free of RM 100000 The exchange rate a... View the full answer