Question: A pension fund manager is considering three mutual fur second is a long-term government and corporate bon money market fund that yields a sure rate

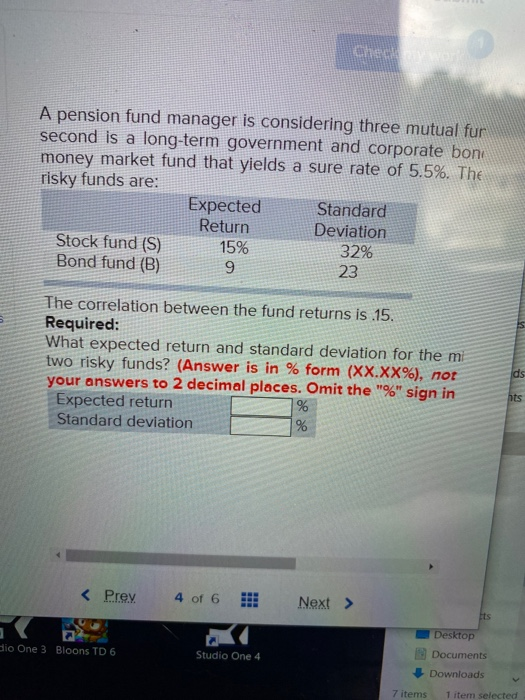

A pension fund manager is considering three mutual fur second is a long-term government and corporate bon money market fund that yields a sure rate of 5.5%. The risky funds are: Expected Standard Return Deviation Stock fund (S) 15% 32% Bond fund (B) 9 23 The correlation between the fund returns is .15. Required: What expected return and standard deviation for the mi two risky funds? (Answer is in % form (XX.XX%), not your answers to 2 decimal places. Omit the "%" sign in Expected return 1% Standard deviation % ds nts Ets Bio One 3 Bloons TD 6 Desktop Documents Studio One 4 Downloads 7 items 1 item selected

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock