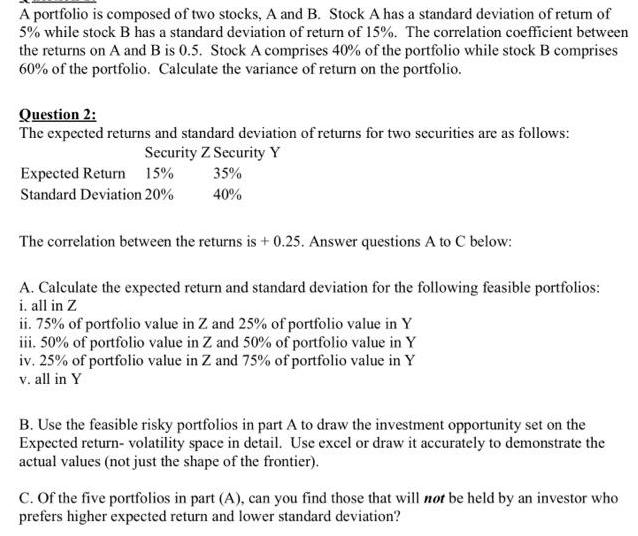

A portfolio is composed of two stocks, A and B. Stock A has a standard deviation...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

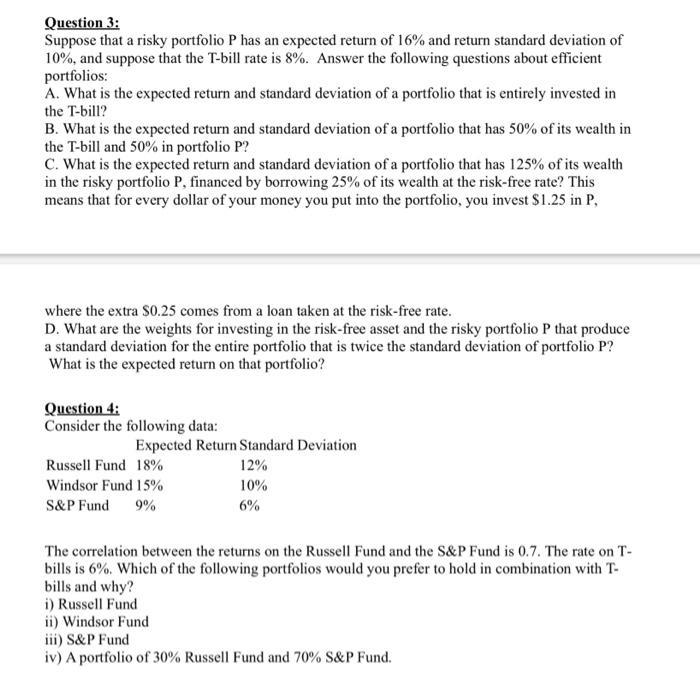

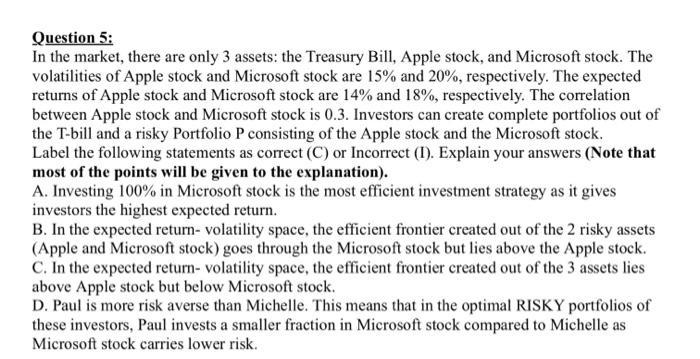

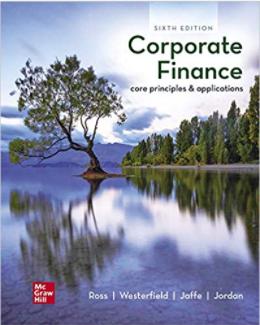

A portfolio is composed of two stocks, A and B. Stock A has a standard deviation of return of 5% while stock B has a standard deviation of return of 15%. The correlation coefficient between the returns on A and B is 0.5. Stock A comprises 40% of the portfolio while stock B comprises 60% of the portfolio. Calculate the variance of return on the portfolio. Question 2: The expected returns and standard deviation of returns for two securities are as follows: Security Z Security Y Expected Return 15% 35% Standard Deviation 20% 40% The correlation between the returns is + 0.25. Answer questions A to C below: A. Calculate the expected return and standard deviation for the following feasible portfolios: i. all in Z ii. 75% of portfolio value in Z and 25% of portfolio value in Y iii. 50% of portfolio value in Z and 50% of portfolio value in Y iv. 25% of portfolio value in Z and 75% of portfolio value in Y v. all in Y B. Use the feasible risky portfolios in part A to draw the investment opportunity set on the Expected return-volatility space in detail. Use excel or draw it accurately to demonstrate the actual values (not just the shape of the frontier). C. Of the five portfolios in part (A), can you find those that will not be held by an investor who prefers higher expected return and lower standard deviation? Question 3: Suppose that a risky portfolio P has an expected return of 16% and return standard deviation of 10%, and suppose that the T-bill rate is 8%. Answer the following questions about efficient portfolios: A. What is the expected return and standard deviation of a portfolio that is entirely invested in the T-bill? B. What is the expected return and standard deviation of a portfolio that has 50% of its wealth in the T-bill and 50% in portfolio P? C. What is the expected return and standard deviation of a portfolio that has 125% of its wealth in the risky portfolio P, financed by borrowing 25% of its wealth at the risk-free rate? This means that for every dollar of your money you put into the portfolio, you invest $1.25 in P, where the extra $0.25 comes from a loan taken at the risk-free rate. D. What are the weights for investing in the risk-free asset and the risky portfolio P that produce a standard deviation for the entire portfolio that is twice the standard deviation of portfolio P? What is the expected return on that portfolio? Question 4: Consider the following data: Expected Return Standard Deviation Russell Fund 18% 12% Windsor Fund 15% S&P Fund 10% 9% 6% The correlation between the returns on the Russell Fund and the S&P Fund is 0.7. The rate on T- bills is 6%. Which of the following portfolios would you prefer to hold in combination with T- bills and why? i) Russell Fund ii) Windsor Fund iii) S&P Fund iv) A portfolio of 30% Russell Fund and 70% S&P Fund. Question 5: In the market, there are only 3 assets: the Treasury Bill, Apple stock, and Microsoft stock. The volatilities of Apple stock and Microsoft stock are 15% and 20%, respectively. The expected returns of Apple stock and Microsoft stock are 14% and 18%, respectively. The correlation between Apple stock and Microsoft stock is 0.3. Investors can create complete portfolios out of the T-bill and a risky Portfolio P consisting of the Apple stock and the Microsoft stock. Label the following statements as correct (C) or Incorrect (I). Explain your answers (Note that most of the points will be given to the explanation). A. Investing 100% in Microsoft stock is the most efficient investment strategy as it gives investors the highest expected return. B. In the expected return- volatility space, the efficient frontier created out of the 2 risky assets (Apple and Microsoft stock) goes through the Microsoft stock but lies above the Apple stock. C. In the expected return- volatility space, the efficient frontier created out of the 3 assets lies above Apple stock but below Microsoft stock. D. Paul is more risk averse than Michelle. This means that in the optimal RISKY portfolios of these investors, Paul invests a smaller fraction in Microsoft stock compared to Michelle as Microsoft stock carries lower risk. A portfolio is composed of two stocks, A and B. Stock A has a standard deviation of return of 5% while stock B has a standard deviation of return of 15%. The correlation coefficient between the returns on A and B is 0.5. Stock A comprises 40% of the portfolio while stock B comprises 60% of the portfolio. Calculate the variance of return on the portfolio. Question 2: The expected returns and standard deviation of returns for two securities are as follows: Security Z Security Y Expected Return 15% 35% Standard Deviation 20% 40% The correlation between the returns is + 0.25. Answer questions A to C below: A. Calculate the expected return and standard deviation for the following feasible portfolios: i. all in Z ii. 75% of portfolio value in Z and 25% of portfolio value in Y iii. 50% of portfolio value in Z and 50% of portfolio value in Y iv. 25% of portfolio value in Z and 75% of portfolio value in Y v. all in Y B. Use the feasible risky portfolios in part A to draw the investment opportunity set on the Expected return-volatility space in detail. Use excel or draw it accurately to demonstrate the actual values (not just the shape of the frontier). C. Of the five portfolios in part (A), can you find those that will not be held by an investor who prefers higher expected return and lower standard deviation? Question 3: Suppose that a risky portfolio P has an expected return of 16% and return standard deviation of 10%, and suppose that the T-bill rate is 8%. Answer the following questions about efficient portfolios: A. What is the expected return and standard deviation of a portfolio that is entirely invested in the T-bill? B. What is the expected return and standard deviation of a portfolio that has 50% of its wealth in the T-bill and 50% in portfolio P? C. What is the expected return and standard deviation of a portfolio that has 125% of its wealth in the risky portfolio P, financed by borrowing 25% of its wealth at the risk-free rate? This means that for every dollar of your money you put into the portfolio, you invest $1.25 in P, where the extra $0.25 comes from a loan taken at the risk-free rate. D. What are the weights for investing in the risk-free asset and the risky portfolio P that produce a standard deviation for the entire portfolio that is twice the standard deviation of portfolio P? What is the expected return on that portfolio? Question 4: Consider the following data: Expected Return Standard Deviation Russell Fund 18% 12% Windsor Fund 15% S&P Fund 10% 9% 6% The correlation between the returns on the Russell Fund and the S&P Fund is 0.7. The rate on T- bills is 6%. Which of the following portfolios would you prefer to hold in combination with T- bills and why? i) Russell Fund ii) Windsor Fund iii) S&P Fund iv) A portfolio of 30% Russell Fund and 70% S&P Fund. Question 5: In the market, there are only 3 assets: the Treasury Bill, Apple stock, and Microsoft stock. The volatilities of Apple stock and Microsoft stock are 15% and 20%, respectively. The expected returns of Apple stock and Microsoft stock are 14% and 18%, respectively. The correlation between Apple stock and Microsoft stock is 0.3. Investors can create complete portfolios out of the T-bill and a risky Portfolio P consisting of the Apple stock and the Microsoft stock. Label the following statements as correct (C) or Incorrect (I). Explain your answers (Note that most of the points will be given to the explanation). A. Investing 100% in Microsoft stock is the most efficient investment strategy as it gives investors the highest expected return. B. In the expected return- volatility space, the efficient frontier created out of the 2 risky assets (Apple and Microsoft stock) goes through the Microsoft stock but lies above the Apple stock. C. In the expected return- volatility space, the efficient frontier created out of the 3 assets lies above Apple stock but below Microsoft stock. D. Paul is more risk averse than Michelle. This means that in the optimal RISKY portfolios of these investors, Paul invests a smaller fraction in Microsoft stock compared to Michelle as Microsoft stock carries lower risk.

Expert Answer:

Related Book For

Corporate Finance Core Principles And Applications

ISBN: 9781260571127

6th Edition

Authors: Stephen Ross, Randolph Westerfield, Jeffrey Jaffe, Bradford Jordan

Posted Date:

Students also viewed these finance questions

-

PLEASE ANSWER IN A DETAILED MANNER, WITH EACH ANSWER PROPERLY RESPONDED TO EACH QUESTION. NOT IN A SLOPPY MANNER. I WOULD LIKE TO KNOW WHICH ANSWER GOES WITH EACH QUESTION. THANK YOU. Image...

-

An Established firm had $100 of stock issues as of the beginning of the year. It Sold $50 worth of additional shares near the beginning of this year. The firm reported net income of $10. What is the...

-

Farley, Inc., is a manufacturer that produces customized computer components for several wellknown computer-assembly companies. Farleys latest contract with CompWest.com calls for Farley to deliver...

-

In an effort to reduce their total costs, many companies are now replacing paychecks with payroll cards, which are stored-value cards onto which the companies can download employees' wages and...

-

Find the limit. 1- tan x lim xT/4 sin x - cos x

-

A project has been selected for implementation. The net cash flow (NCF) profile associated with the project is shown below. MARR is 10 percent/year. a. What is the internal rate of return of this...

-

The unadjusted trial balance that you prepared for PS Music at the end of Chapter 2 should appear as shown below. The data needed to determine adjustments are as follows: a. During July, PS Music...

-

Let C be the closed convex set shown below u x2 21 Note that C is the intersection of three halfspaces and can be precisely described by the inequalities C = {x R x-1, x20, x1 + x2 0}. (a) Describe...

-

In the region defined by -h/2

-

Assume the credit terms offered to your firm by your suppliers are 4/15, net 60. Calculate the cost of the trade credit if your firm does not take the discount and pays on day 60.

-

The following information pertains to Alpha Corporation whose functional currency is the dollar. Required Assume that Alpha Corporation designates the forward contract as a fair value hedge of the...

-

Happy Valley Homecare Suppliers, Inc. (HVHS), had $10.9 million in sales in 2015. Its cost of goods sold was $4.36 million, and its average inventory balance was $1.77 million. a. Calculate the...

-

Your company had $14 million in sales last year. Its cost of goods sold was $9.8 million and its average inventory balance was $1,300,000. What was its average days of inventory?

-

Your firm purchases goods from its supplier on terms of 1.7/15, net 35. a. What is the effective annual cost to your firm if it chooses not to take the discount and makes its payment on day 35? b....

-

Nancy looks at 2 projects with different life spans. A has a NPV of 400k and with a 6 year life and B has a NPV of 500k and a 4 yr life. Using the EAA approach, which one is the better investment if...

-

Refer to the situation described inBE 18-13, but assume a 2-for-1 stock split instead of the 5% stock dividend. Prepare the journal entry to record the stock split if it is to be effected in the form...

-

Consider the following cash flows on two mutually exclusive projects: The cash flows of Project A are expressed in real terms while those of Project B are expressed in nominal terms. The appropriate...

-

You will earn the YTM on a bond if you hold the bond until maturity and if interest rates dont change. If you actually sell the bond before it matures, your realized return is known as the holding...

-

Tool Manufacturing has an expected EBIT of $51,600 in perpetuity and a tax rate of 24 percent. The firm has $90,000 in outstanding debt at an interest rate of 6.5 percent, and its unlevered cost of...

-

How might planning in a not-for-profit organization such as the World Wildlife Fund differ from planning in a for-profit organization such as Airbnb?

-

Provide examples of the sources of data a residential solar panel company might gather when engaging in environmental scanning. Exhibit 8-6 may be helpful when answering this question.

-

What advantages and disadvantages does Johnson Controls OpenBlue platform have over companies looking to develop solutions on their own?

Study smarter with the SolutionInn App