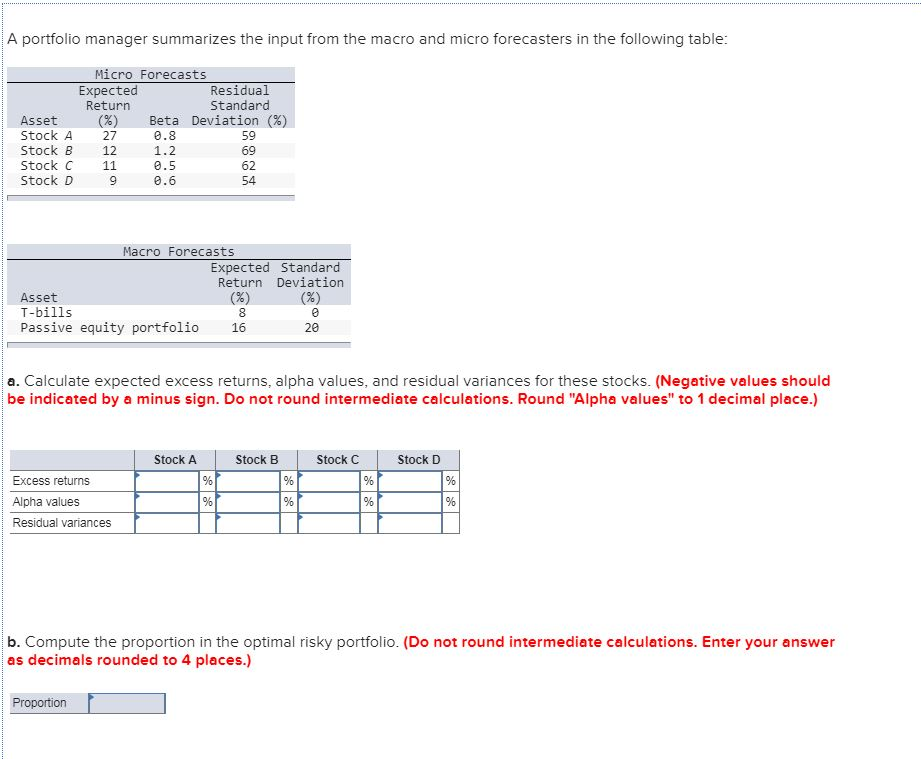

Question: A portfolio manager summarizes the input from the macro and micro forecasters in the following table Micro Forecasts Residual Standard Deviation(%) Asset Stock A Stock

A portfolio manager summarizes the input from the macro and micro forecasters in the following table Micro Forecasts Residual Standard Deviation(%) Asset Stock A Stock B Stock C Stock D Expected Return (%) 27 12 11 Beta 0.8 1.2 59 69 62 54 Macro Forecasts Expected Standard Return Deviation Asset T-bills Passive equity portfolio 16 a. Calculate expected excess returns, alpha values, and residual variances for these stocks. (Negative values should be indicated by a minus sign. Do not round intermediate calculations. Round "Alpha values" to 1 decimal place.) Stock A Stock B Stock C Stock D Excess returns Alpha values Residual variances b. Compute the proportion in the optimal risky portfolio. (Do not round intermediate calculations. Enter your answer as decimals rounded to 4 places.) Proportion A portfolio manager summarizes the input from the macro and micro forecasters in the following table Micro Forecasts Residual Standard Deviation(%) Asset Stock A Stock B Stock C Stock D Expected Return (%) 27 12 11 Beta 0.8 1.2 59 69 62 54 Macro Forecasts Expected Standard Return Deviation Asset T-bills Passive equity portfolio 16 a. Calculate expected excess returns, alpha values, and residual variances for these stocks. (Negative values should be indicated by a minus sign. Do not round intermediate calculations. Round "Alpha values" to 1 decimal place.) Stock A Stock B Stock C Stock D Excess returns Alpha values Residual variances b. Compute the proportion in the optimal risky portfolio. (Do not round intermediate calculations. Enter your answer as decimals rounded to 4 places.) Proportion

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts