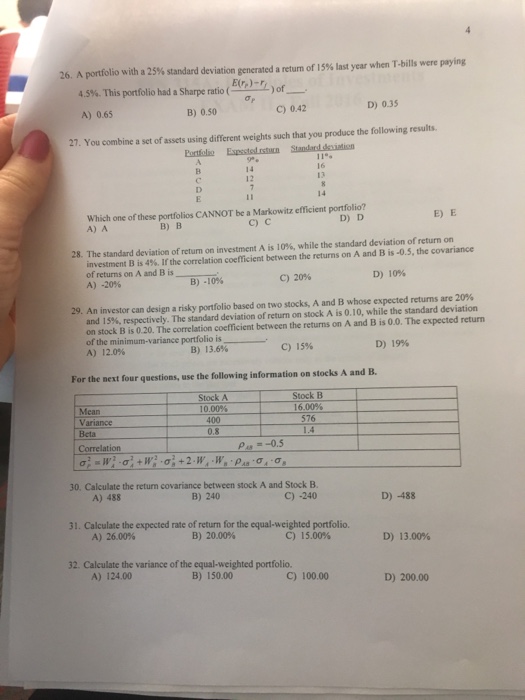

Question: A portfolio with a 25% standard deviation generated a return of 15% last year when T-bills were paying 4.5%. This portfolio had a Sharpe ratio

A portfolio with a 25% standard deviation generated a return of 15% last year when T-bills were paying 4.5%. This portfolio had a Sharpe ratio (E(r_p) - r_L/sigma_P) of __ 0 65 0.50 0.42 0.35 You combine a set of assets using different weight, such that you produce the following results. Portfolio Expected return Standard Deviation A 9 11 B 14 16 C 12 13 D 7 8 E 11 14 Which one of these portfolios cannot be a Markowitz efficient portfolio? A B C D E The standard deviation of return on investment A is 10%. while the standard deviation of return on investment B is 4% If the correlation coefficient between the returns on A and B is -0. 5, the covariance of returns on A and B is ___. -20% -10% 20% 10% An investor can design a risky portfolio based on two stocks, A and B whose expected returns are 20% and 15%. respectively The standard deviation of return on stock A is 0 10, while the standard deviation on stock B is 0 20 The correlation coefficient between the returns on A and B is 0.0. The expected return of the minimum-variance portfolio is 12.0% 13.6% 15% 19% For the sell four questions. are the following information on stocks A and B. Calculate the return covariance between stock A and Stock B. 488 240 -240 -488 Calculate the expected rate of return for the equal-weighted portfolio. 26.00% 20.00% 15.00% 13.00% Calculate the variance of the equal-weighted portfolio. 124.00 150.00 100.00 200.00

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts