Question: (a) Prepare the entry to record the interest expense at October 1, 2014. Assume that accrued interest payable was credited when the bonds were issued.

| (a) | Prepare the entry to record the interest expense at October 1, 2014. Assume that accrued interest payable was credited when the bonds were issued. | |

| (b) | Prepare the entry to record the conversion on April 1, 2015. (Book value method is used.) Assume that the entry to record amortization of the bond discount and interest payment has been made. |

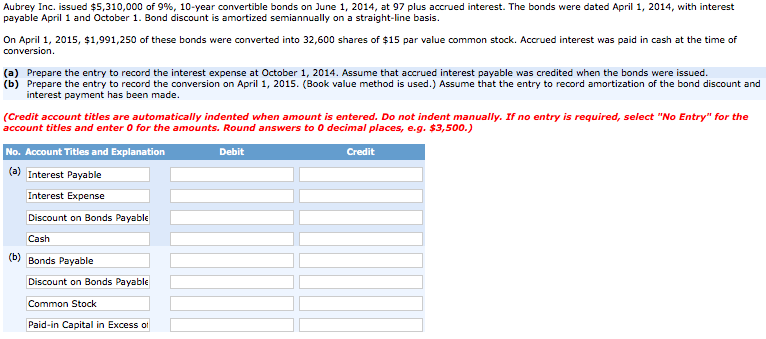

Aubrey Inc. issued $5,310,000 of 9%, 10-year convertible bonds on June 1, 2014, at 97 plus accrued interest. The bonds were dated April 1, 2014, with interest payable April 1 and October 1. Bond discount is amortized se annually on a straight-line basis. On April 1, 2015, $1,991,250 of these bonds were converted into 32,600 shares of $15 par value common stock. Accrued interest was paid in cash at the time of conversion (a) Prepare the entry to record the interest expense at October 1, 2014. Assume that accrued interest payable was credited when the bonds were issued. (b) Prepare the entry to record the conversion on April 1, 2015. (Book value method is used.) Assume that the entry to record amortization of the bond discount and interest payment has been made. (Credit account titles are automatically indented when amount is entered. Do not indent manually. If no entry is required, select "No Entry" for the account titles and enter 0 for the amounts. Round answers to 0 decimal places, e.g. $3,500) No. Account Titles and Explanation Credit (a) Interest payable Interest Expense Discount on Bonds Payable Cash (b) Bonds payable Discount on Bonds Payable common stock Paid-in capital in Excess o

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts